Africa’s EdTech Funding Story: Record Market Potential, But Equity Investors Are Pulling Back

A $3.4 billion sector with a clear path to $19.7 billion by 2034 is attracting philanthropic and DFI capital — but traditional venture investors grew more cautious in 2025 even as the broader tech market rebounded.

Africa’s education technology sector is living in two contradictory realities at once. The market numbers tell a story of extraordinary long-term promise: a continent of 1.4 billion people, with the world’s youngest population, a persistent learning infrastructure gap, and a $3.4 billion EdTech market that analysts project will expand to $19.7 billion by 2034 — a compound annual growth rate of over 19%. Yet on the ground in 2025, equity investors are stepping back just as the opportunity peaks.

The Equity Retreat

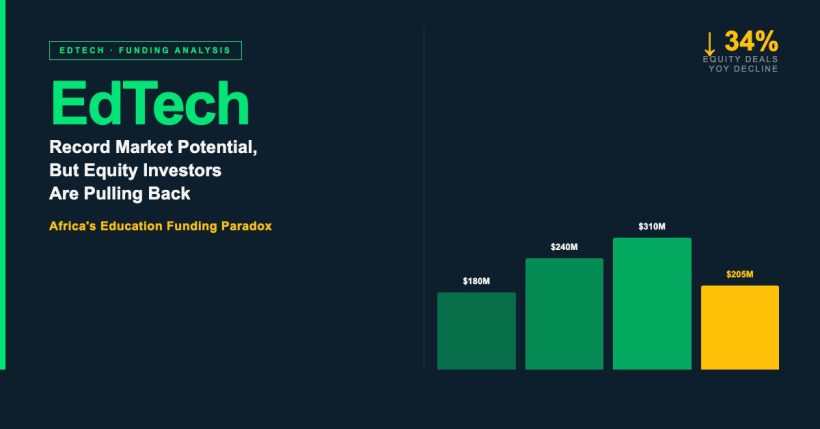

Partech Africa’s 2025 Africa Tech VC Report — the continent’s most closely watched funding tracker — recorded a sharp decline in EdTech equity investors of approximately 70% year-on-year, even as total African tech funding rebounded to a robust US$4.1 billion (up 25% from 2024). EdTech was one of the few sectors to buck the broader recovery trend in equity terms, as VC firms that once backed multiple education startups tightened their portfolios.

The reasons are familiar to anyone who followed the sector’s recent history. Edukoya, which had raised $3.5 million in Africa’s largest EdTech pre-seed round at the time, shut down in February 2025. Nigeria’s economic pressures — persistent naira depreciation and contracting household income — have made subscription-based learning models difficult to sustain at scale. Even uLesson, the flagship Nigerian edtech startup backed by TLcom Capital, cut subscription fees by half in 2024 to retain users. Decagon, once a beacon of tech-talent training, pivoted entirely away from education in March 2025, citing unsustainable unit economics.

“The low-hanging fruit of EdTech in Africa was always the premium segment — young professionals who could afford quality digital learning,” said Olumide Soyombo, co-founder of Voltron Capital, which has backed several Nigerian startups. “That segment is smaller than the PowerPoint slides suggested, and it’s price-sensitive in ways that make the SaaS revenue model hard.”

Where the Money Is Still Flowing

The retreat of traditional VCs has not meant a funding vacuum. Philanthropic capital, development finance institutions (DFIs), and blended-finance programmes have stepped in — and in some cases, written larger cheques than venture investors typically would.

The Mastercard Foundation EdTech Fellowship, administered through Co-creation Hub (CcHUB), backed 12 African EdTech companies with $100,000 equity-free grants each in 2025, channelling $1.2 million in non-dilutive capital to startups across Nigeria, Kenya, Rwanda, Ghana, and Ethiopia. The programme also provides technical assistance and investor connections, positioning it as a de facto accelerator for the sector.

Proparco, the French DFI, maintains an active EdTech portfolio in Africa ranging from €0.5 million to €5 million per investment, with Moringa School — a Kenyan coding bootcamp that has trained thousands of software developers — among its flagship bets. DOB Equity backs East African ventures including Zydii and Moringa School with a similar patient-capital approach.

Earlier-stage players remain active. Ingressive Capital (tickets of $50K–$500K) and Future Africa ($100K–$500K) continue writing pre-seed and seed cheques, particularly for Nigerian and Ghanaian founders, while TLcom Capital remains the continent’s most prominent institutional VC for education technology at the Series A stage ($1M–$3M range).

Which Countries Lead — and Which Sub-Sectors Attract Capital

Nigeria and Kenya account for the bulk of EdTech investment by volume and deal count, with South Africa and Egypt following. Rwanda and Ghana punch above their weight in terms of ecosystem density relative to population.

The sub-sector picture has shifted noticeably: skills and vocational training — coding schools, professional certification platforms, job-readiness programmes — now attract more capital than K-12 products, reflecting both investor pragmatism and a demographic reality. Africa’s 15–35 age cohort is the fastest-growing segment of the workforce, and employers are increasingly willing to co-fund training that produces job-ready candidates.

AltSchool Africa, a Nigerian startup offering mobile-friendly courses in software engineering and cybersecurity with documented employer partnerships, has raised $4 million and is among the stronger performers in this cohort. Gebeya, the Ethiopian skills platform that connects graduates directly with employer pipelines, has attracted international investor attention as it scales beyond East Africa.

The Adult-Learning Pivot

A structural shift is underway: Africa’s EdTech sector is moving from children toward adults. The K-12 market, while vast in user numbers, has proven the hardest to monetise — parents in most African markets cannot or will not pay subscription prices that make the unit economics work. The adult professional and vocational market, by contrast, has a clearer willingness-to-pay linked to income outcomes.

This pivot is not without risk. Africa has more than 600 million children of school age, and the K-12 gap is arguably the continent’s most critical education challenge. If commercial EdTech largely abandons the school market, the burden falls entirely on governments and aid organisations — an outcome that sits uneasily with the continent’s stated ambitions for universal quality education.

Looking to 2026

Analysts tracking the sector point to government procurement as the next frontier. National digital skills programmes — Nigeria’s 3 Million Technical Talent (3MTT) initiative, Kenya’s Digital Superhighway agenda, South Africa’s SETA-funded training frameworks — represent large, stable revenue streams for EdTech providers that can navigate public sector procurement cycles.

The 500-plus EdTech startups currently operating across Africa, of which fewer than 200 have raised any formal funding, are betting that 2026 will mark the moment when DFI patience, government demand, and demographic pressure converge into a market that finally delivers on the sector’s long-standing promise. The data suggests they have reason to hope — but the business model questions that broke Edukoya and Decagon have not gone away.

BETAR.africa covers education, technology, and business across Africa. Follow our Education vertical for ongoing coverage of EdTech investment and workforce development.