Zimbabwe’s 15% Digital Services Tax Is the Steepest on the Continent — Here’s What It Means for Business

By BETAR.africa Policy & Regulation Desk

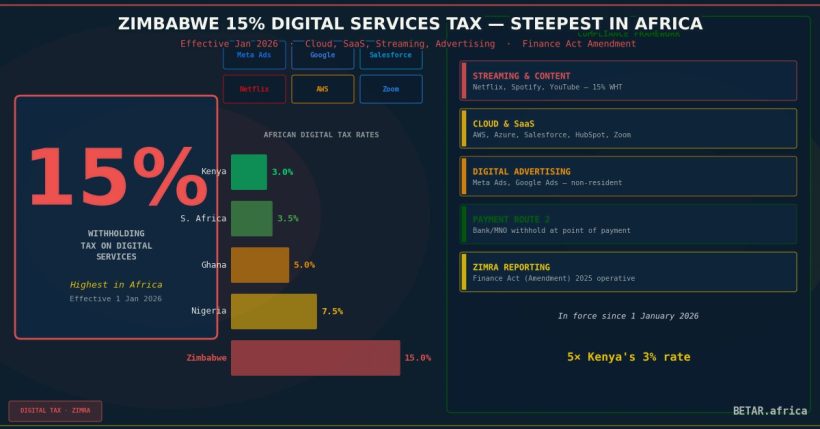

Since January 1, 2026, every business in Zimbabwe that pays for a foreign digital service — whether that’s a Netflix subscription, a Starlink connection, or a Salesforce licence — has been subject to a 15% withholding tax remitted to the Zimbabwe Revenue Authority (ZIMRA).

That rate is the steepest digital services tax currently in force anywhere in Africa. It is five times Kenya’s 3% Significant Economic Presence Tax and more than double the rates most other African countries have adopted or are considering. For companies operating in Zimbabwe, it is an immediate cost increase on virtually every cloud tool, SaaS platform, and digital subscription in their IT stack.

Understanding the mechanics, the compliance exposure, and the continental context is now a baseline requirement for any finance or operations team with Zimbabwe exposure.

What the Tax Covers

The Zimbabwe Finance Act (Amendment) 2025 introduced a withholding tax on payments made to non-resident persons for digital services. The tax applies to:

- Streaming and content subscriptions: Netflix, Spotify, YouTube Premium, Apple TV+, and equivalent platforms

- Satellite and fixed internet services: Starlink and other non-resident satellite internet providers

- Ride-hailing and delivery platforms: Bolt, inDrive, and similar platforms where the operator is non-resident

- Cloud computing and SaaS tools: AWS, Microsoft Azure, Google Cloud, Salesforce, HubSpot, Zoom, and equivalent enterprise software

- Digital advertising: Payments to non-resident digital advertising platforms (Meta Ads, Google Ads)

- Digital content and app stores: App store payments, in-app purchases routed to non-resident developers

The operative principle is straightforward: if payment is made from Zimbabwe to a non-resident for a digitally delivered service, the 15% withholding obligation is triggered.

The Collection Mechanism: Two Routes

ZIMRA has designed a dual-track enforcement approach:

Route 1 — Non-resident self-registration. Foreign digital service providers with sufficient economic presence in Zimbabwe (broadly, those generating revenue above ZIMRA’s registration threshold) are required to register as non-resident taxpayers and remit the 15% directly. Platform-side compliance.

Route 2 — Payment intermediary withholding. Where a non-resident provider has not self-registered, the obligation shifts to the local payment intermediary — typically a bank, mobile money operator, or corporate treasury. The local entity is required to withhold 15% at the point of payment and remit to ZIMRA.

In practice, Route 2 is the dominant mechanism for most businesses. Foreign SaaS vendors are unlikely to have registered with ZIMRA voluntarily on day one. That means the cost and compliance burden falls on local businesses making the payments.

Business Cost Exposure: A Practical Illustration

Consider a mid-sized Zimbabwean enterprise with a typical SaaS stack:

| Service | Monthly cost (USD) | 15% tax |

|---|---|---|

| Microsoft 365 (20 seats) | $300 | $45 |

| Salesforce CRM | $500 | $75 |

| AWS cloud infrastructure | $800 | $120 |

| Google Workspace (20 seats) | $240 | $36 |

| Zoom Business | $200 | $30 |

| Total | $2,040 | $306/month |

Annualised, that enterprise is paying approximately $3,672 in additional tax on its digital tools — before factoring in ride-hailing, advertising spend, or any consumer subscriptions on business accounts.

For larger enterprises with more extensive cloud infrastructure — data-heavy operations, fintechs, logistics companies — the exposure is materially higher. An enterprise spending $10,000/month on cloud services is paying an additional $18,000/year in digital services tax.

The Enforcement Gap

The critical compliance question is not the rate — it is how ZIMRA enforces collection from non-residents who do not self-register.

Most major global tech platforms have demonstrated willingness to comply with digital services taxes in markets where collection is operationally straightforward. The EU’s VAT OSS system and Kenya’s DST experience both show that large platforms will register when the regulatory framework is clear and the compliance pathway is simple.

Zimbabwe presents a harder case. The RTGS/ZiG currency environment, international banking restrictions, and the country’s history of inconsistent regulatory enforcement create friction for non-resident registration. ZIMRA has not yet published detailed guidance on:

- The registration process for non-resident digital service providers

- The minimum revenue threshold that triggers self-registration

- Audit and penalty frameworks for non-compliant intermediaries

Until this guidance is published, local businesses bear the full compliance risk. Payment intermediaries — banks processing international corporate card payments — are the de facto enforcement point, and their systems may not yet be configured to identify and withhold on digital service transactions automatically.

Practical advice for CFOs: Do not assume your bank is handling the withholding. Until ZIMRA publishes and enforces intermediary guidance, the safest posture is manual identification and tracking of all payments to non-resident digital service providers, with the 15% withheld and remitted directly.

The Continental Context: Africa’s Digital Tax Landscape

Zimbabwe’s 15% rate sits at the far end of Africa’s growing digital services tax spectrum. The landscape as of March 2026:

| Country | Tax | Rate | In force |

|---|---|---|---|

| Zimbabwe | Withholding tax on digital services | 15% | January 1, 2026 |

| Tanzania | Value Added Tax on digital services | 18% (VAT rate, not DST-specific) | 2022 |

| Kenya | Significant Economic Presence Tax | 3% | 2021 (amended 2023) |

| Nigeria | Significant Economic Presence Order | 6% WHT | 2022 |

| South Africa | VAT on electronic services | 15% (standard VAT) | 2014 |

| Ghana | VAT on electronic services | 12.5–15% (standard VAT) | 2021 |

Two clarifications on the table above: South Africa and Ghana impose standard VAT on electronic services rather than a standalone digital services tax — the compliance and collection mechanisms differ. Zimbabwe’s 15% is a withholding tax, applied at source by the local payer, which creates a structurally different compliance burden than supplier-collected VAT.

The broader trend is unmistakable. Revenue-constrained African governments are treating digital services as a legitimate and increasingly accessible tax base. Zimbabwe’s aggressive rate signals that this trend is entering a new phase: governments are no longer following international norms cautiously but are setting their own fiscal benchmarks.

What the Rate Signals for Other Markets

Tax policy often moves through regional demonstration effects. When Kenya introduced its 1.5% Digital Services Tax in 2021 (later restructured as the SEP framework), it validated the concept for the region. Nigeria followed. Uganda attempted to.

Zimbabwe’s 15% rate — whether it generates expected revenues or not — places a high-water mark in the public discourse. A government in Malawi, Zambia, or Ethiopia reviewing its own digital economy revenue options now has Zimbabwe as a reference point, not just Kenya’s 3%.

For regional businesses and multinationals, the takeaway is not that every country will rush to 15%. It is that the floor is rising. Planning for digital services tax exposure across African operating markets should now be a standard component of regional financial modelling — not a country-specific footnote.

What Businesses Should Do

Immediate (if operating in Zimbabwe):

1. Audit all payment flows to non-resident digital service providers. Identify every vendor, subscription, and platform payment.

2. Determine whether your bank or payment processor is currently withholding and remitting — do not assume compliance.

3. If your bank is not withholding, begin manual withholding and remittance to ZIMRA directly while awaiting formal intermediary guidance.

4. Brief your board or CFO on annualised cost exposure from the tax.

Near-term (Q2 2026):

– Monitor ZIMRA guidance on non-resident registration and intermediary obligations.

– Evaluate whether any affected non-resident vendors have registered with ZIMRA (which would shift the compliance obligation to them).

– Review corporate card and expense management policies to flag digital service payments for DST tracking.

Strategic (ongoing):

– Build digital services tax into African market cost modelling. At minimum, model scenarios for 5%, 10%, and 15% rates in all markets where you have material cloud/SaaS spend.

– Engage industry associations (CZI, ICT Association of Zimbabwe) on advocating for ZIMRA compliance guidance and reasonable enforcement timelines.

The Bottom Line

Zimbabwe’s 15% digital services withholding tax is real, in force, and generating compliance obligations that most businesses in the country are not yet fully managing. The enforcement mechanism is weighted toward local intermediaries and corporate payers, not non-resident platforms — meaning the compliance burden falls directly on Zimbabwean businesses.

More broadly, Zimbabwe’s rate illustrates a continental shift in fiscal philosophy: African governments increasingly view foreign digital platforms not as untaxable internet actors but as commercial operators extracting revenue from their markets, subject to the same fiscal obligations as any other business.

Companies with Zimbabwe exposure need to act now. Companies with broader sub-Saharan Africa exposure need to build digital tax contingency into their regional planning.

BETAR.africa tracks regulatory and tax developments across all 54 African nations. This analysis is based on publicly available provisions of the Zimbabwe Finance Act (Amendment) 2025 and published coverage from TechAfrica News and Developing Telecoms. ZIMRA has not yet published full implementation guidance as of March 2026.

Word count: ~1,350 words

Tags: [DIGITAL-TAX] Zimbabwe, ZIMRA, Digital Services Tax, Withholding Tax, SaaS Compliance, Africa Digital Economy