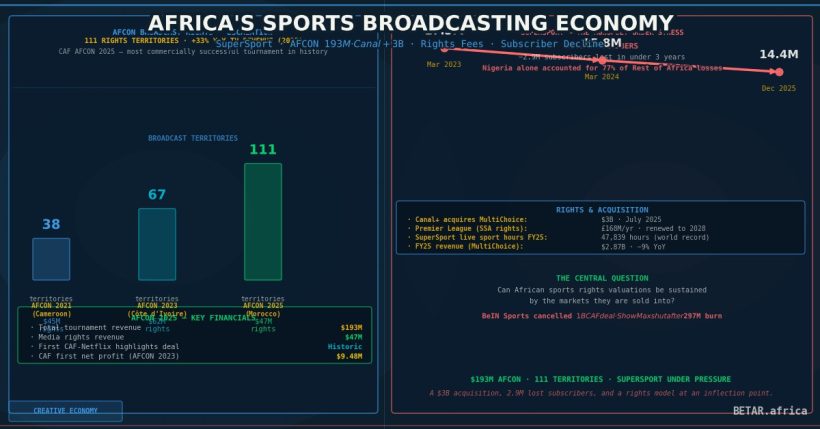

When the Africa Cup of Nations tournament kicked off in Morocco in January 2026, it did so with broadcast reach that would have seemed improbable five years earlier: 111 rights-holding territories, 20 European broadcast partnerships, a CAF-Netflix highlights deal — the first of its kind — and a projected total tournament revenue of $193 million, of which $47 million came from media rights alone. CAF described AFCON 2025 as the most commercially successful in its history.

The trajectory is striking. At AFCON Cameroon 2021, just 38 territories broadcast the tournament. By AFCON Côte d’Ivoire 2023, that had grown to 67 territories, with CAF recording a 33% year-on-year rise in TV revenue and its first net profit — $9.48 million — in several years. The Morocco tournament more than doubled broadcast reach again. For CAF President Dr. Patrice Motsepe, the pattern confirms a structural shift: “The exponential growth and global competitiveness of football in Africa has resulted in substantial interest from major African and international broadcasters in African Football.”

But behind that broadcast expansion lies a more complicated economic story — one involving cancelled billion-dollar deals, a satellite TV empire under stress, a streaming platform that burned through $297 million before shutting its doors, and a fundamental question about whether African sports rights valuations can be sustained by the markets they are sold into.

How SuperSport Built the Monopoly

For three decades, the answer to African sports broadcasting was straightforward: MultiChoice’s DStv satellite network and its sports arm, SuperSport. Operating across 50 Sub-Saharan African markets, SuperSport assembled what regulators have described as an unassailable position in live sports broadcasting. It holds Premier League rights across Sub-Saharan Africa — a deal that was worth approximately £168 million (~$222 million) per year in its 2017 cycle and has since been renewed through to 2028. It holds CAF competition rights across its territories. In FY2025, SuperSport aired 47,839 hours of live sport — a volume that exceeds any other broadcaster on the planet by programming hours.

The economics of that position depended on premium subscribers willing to pay for it. At its peak in March 2023, MultiChoice held 17.3 million DStv subscribers across the continent. By December 2025, that figure had fallen to 14.4 million — a loss of nearly 2.9 million subscribers in under three years. Nigeria alone accounted for 77% of the losses in the Rest of Africa segment, with MultiChoice Nigeria shedding 1.4 million subscribers between 2023 and 2025. MultiChoice’s FY2025 revenue fell 9% to $2.87 billion, with adjusted EBIT contracting 14%.

The company did not reach that point as an independent entity. Canal+, the French broadcasting group, completed its $3 billion acquisition of MultiChoice in July 2025. By February 2026, it had centralised SuperSport’s sports rights acquisition decisions from Johannesburg to Paris — a restructuring that stripped regional teams of purchase authority and led to the first-ever loss of rights to the Winter Olympics and World Darts Championships from the SuperSport schedule.

The Rights Fee Escalation — and Its Casualties

The CAF rights story illustrates what happens when broadcast rights outpace the revenue base available to monetise them.

In 2015, CAF signed a $1 billion, 12-year deal with French media group Lagardère, with SuperSport as a sub-contractor, handing near-total control of African football rights to a single intermediary. An Egyptian court found the arrangement violated competition law; CAF cancelled it in 2019, paying Lagardère $50 million in compensation after the agency had sought $90 million. CAF then signed with beIN Sports — a deal valued at approximately $415 million covering 40-plus countries. That relationship also ended in dispute: CAF terminated the contract in September 2023, accusing beIN of $80 million in outstanding unpaid obligations.

Since then, CAF has restructured its rights distribution across multiple sub-rights holders. IMG holds international distribution across 85-plus countries. New World TV (NWTV) secured Sub-Saharan African broadcast rights — backed by a EUR 245 million facility from Afreximbank, signed in October 2024, to fund acquisition of FIFA, UEFA, CAF, La Liga, and Ligue 1 rights for broadcast across the continent. The complexity of the current arrangement reflects both CAF’s hunger for higher valuations and the difficulty of finding a single entity with the balance sheet and distribution reach to cover Africa at scale.

For Premier League rights — the cornerstone of SuperSport’s programming — financial terms of the most recent renewals remain undisclosed. The 2017 benchmark of $222 million per year indicates the magnitude of the obligation. With MultiChoice carrying approximately $300 million in outstanding sports rights as of late 2024, the rights arms race has consequences that extend well beyond programming budgets.

The Streaming Miscalculation

MultiChoice’s attempt to future-proof its position through streaming produced the most visible financial failure in African media in recent memory. Showmax 2.0 launched on February 12, 2024, rebranded with mobile-first positioning and backed by Comcast/NBCUniversal’s Peacock technology. Its Premier League subscription tier — priced at R69 per month in South Africa (~$3.75) and ₦2,900 per month in Nigeria (~$3.35) — was designed to compete at African income levels.

“There are currently just over 450 million smartphones in the hands of individuals across Africa,” said Marc Jury, CEO of Showmax, at the platform’s launch, “and more than 250 million avid football lovers on the continent.” In FY2024, Showmax grew revenue 22% to R1.0 billion (~$54 million) and reached 3.1 million paying subscribers, with Rest-of-Africa subscriber growth running at 75% CAGR.

The economics beneath those numbers were unsustainable. By FY2025, Showmax posted a trading loss of R4.9 billion (~$297 million) — 88% worse than the prior year. The platform was losing approximately $2.50 for every $1 it earned. Canal+ CEO Maxime Saada described the underperformance as “obvious.” On March 5, 2026, Canal+ announced Showmax’s closure, with plans to replace it with a proprietary streaming platform.

The failure reflects a structural tension at the heart of African sports streaming economics: rights fees are priced for premium markets, while African ARPU is structurally constrained. A DStv Premium subscription in South Africa runs R979 per month (~$53); in Kenya, a Premium package is approximately KES 11,000 per month (~$85). Mobile-first streaming can reach those markets at a fraction of the price point, but the revenue per subscriber cannot cover rights costs that were negotiated on the assumption of a premium pay-TV subscriber base.

Mobile Crossover and What Comes Next

The audience is moving regardless of whether the business model is ready. A 2025 survey across six African countries found 41% of fans primarily consuming football content on mobile devices, against 40% on traditional satellite TV — a crossover that was projected for 2027, not 2025. Africa’s SVOD market reached $3.04 billion in 2025 and is projected to reach $4.58 billion by 2030, at an 8.54% compound annual growth rate.

The rights market is tracking that trajectory from a different direction. AFCON broadcast territories grew nearly threefold between 2021 and 2025 — but the revenue per territory remains thin outside Europe and the MENA region. CAF’s rights model increasingly depends on international broadcasters (in Europe and Asia) to establish the headline fee, while African broadcasters source rights at lower rates through intermediaries like NWTV.

That arrangement may be politically unstable: the same CAF that fought and terminated two major rights deals is now restructuring again. The Afreximbank-backed NWTV facility signals an appetite for African institutional capital to finance African broadcast rights — a different model than the one that prevailed under Lagardère and beIN. Whether it produces more stable economics, or simply replicates the same structural imbalance under different ownership, will be visible in the rights cycle that follows AFCON 2028 — when the tournament shifts to a four-year schedule, creating the scarcity that analysts expect to drive fees to a new high.

The satellite infrastructure that made SuperSport’s monopoly possible is declining in subscribers. The streaming alternative burned through nearly $300 million before being abandoned. And the most commercially successful AFCON in history generated $47 million in media rights — a significant number, but one that a single Premier League season deal dwarfs by a factor of four. The economics of African sports broadcasting are expanding. The business model for who captures that value remains unresolved.

Sources: MultiChoice annual reports (FY2024, FY2025); CAF commercial reports (AFCON 2023, AFCON 2025); SportsPro; Sports Media Africa; Sportcal; Afreximbank press releases; Deadline; Space in Africa.