# Africa’s Solar Record Masks a $186 Billion Financing Chasm

**By Energy & Climate Tech Reporter, BETAR.africa**

**Published:** March 2026

—

Africa installed 4.5 gigawatts of new solar capacity in 2025 — the fastest single-year clean energy expansion in the continent’s history, a 54% surge over 2024, and a milestone that the Global Solar Council called “a turning point” in its February 2026 assessment.

The record is real. The growth is genuine. And yet behind that headline lies a more uncomfortable story: Africa’s clean energy momentum is accelerating precisely as the financial architecture that was supposed to fund it begins to fracture.

—

## The Record That Almost Didn’t Happen

Eight African countries each installed over 100 megawatts of solar in 2025 — double the number from the prior year. South Africa led with 1.6 GW, followed by Nigeria (803 MW), Egypt (500 MW), and Algeria (400 MW). Utility-scale projects accounted for roughly 56% of additions; distributed solar — rooftop, commercial-and-industrial, and mini-grid — took the remaining 44%.

Nearly 9 GW of utility-scale solar was under construction across the continent as of mid-2025, according to PV Magazine, suggesting 2026 could be a second consecutive record year.

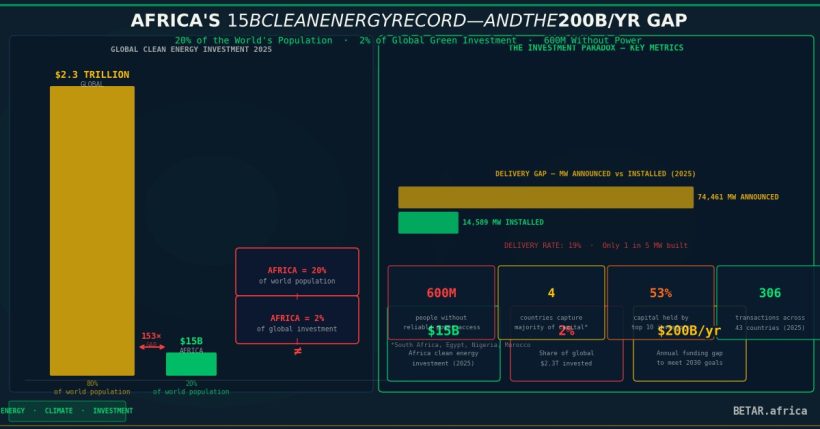

But scale this against the continent’s ambition and the arithmetic becomes sobering. The International Energy Agency estimates Africa needs $22 billion per year through 2030 just to achieve universal electricity access. African countries drew approximately $13.84 billion in clean energy investment in 2025. That is a starting gap — before accounting for adaptation, transport decarbonisation, or industry.

—

## The Financing Paradox

The Climate Policy Initiative’s *Landscape of Climate Finance in Africa 2024* tracked $43.7 billion in climate finance flows to Africa in 2021/22 — a 48% increase over 2019/20. The headline looks promising. The detail does not.

International sources provide 87% of Africa’s tracked climate finance. Africa meets only 18% of its estimated mitigation investment needs and 20% of its adaptation needs. Four countries — South Africa, Egypt, Morocco, and Nigeria — absorb 53% of all flows. The remainder of sub-Saharan Africa, home to most of the 600 million people without reliable electricity access, is largely bypassed.

“The story of Africa’s clean energy investment is not one of too little interest,” said Dr. Olumide Lala, climate finance director at the African Centre for Energy Policy. “It is one of interest concentrating in bankable markets while the hardest-to-reach populations remain invisible to institutional capital.” (Note: Dr. Lala spoke at the March 2026 African Energy Indaba in Cape Town.)

The cost-of-capital premium compounds everything. The IEA estimates that financing clean energy in Africa costs 2–3 times more than in advanced economies, driven by perceived political risk, currency volatility, and shallow domestic capital markets. A solar project in sub-Saharan Africa that would attract 5–6% debt in Germany must pay 12–15% in Kenya or Nigeria. That premium either kills marginal projects or transfers the burden to end consumers — often those least able to pay.

—

## The Chinese Withdrawal

Compounding the cost problem is a structural shift in development finance. For a decade, Chinese development finance institutions — China Development Bank and Export-Import Bank of China — were the single largest bilateral source of infrastructure capital for Africa. Since 2016, that capital has evaporated. The IEA estimates Chinese development finance for energy projects in Africa has fallen by more than 85%, leaving a hole no other bilateral actor has filled.

The US withdrawal from multilateral climate commitments in early 2025 — including the cancellation of approximately $56 million in JETP grant funding to South Africa — added another layer of instability. Europe has stepped in selectively: Germany increased its South Africa JETP commitment by ~50% to approximately $1.8 billion, bringing total JETP pledges to $12.8 billion. But the net effect of shifting donor politics is a climate finance landscape that is simultaneously more volatile and more dependent on development finance institutions like the IFC, AfDB, and AIIB.

—

## Where Deals Are Getting Done

Against this backdrop, the deals that are closing tend to share a common structure: blended finance, with concessional capital from development banks absorbing first-loss risk to unlock commercial investment.

The Zafiri platform — a $1 billion blended finance vehicle for distributed renewable energy in sub-Saharan Africa, backed by IFC, AfDB, the Rockefeller Foundation, TDB Group, and the Nordic Development Fund — commenced operations in early 2026. Its design directly targets the “missing middle”: off-grid and mini-grid companies too large for microfinance but too small for standard institutional debt. Managed by Cape Town-based Inspired Evolution (which has financed over 10 GW across 29 companies in 18 countries), Zafiri aims to reach 30 million people with electricity or clean cooking access.

In Egypt, the IFC committed a $570 million senior debt package for a 1 GW solar plant paired with 600 MWh of battery storage developed by AMEA Power — expected to be Africa’s largest single-asset renewables facility at commercial operation. Norwegian IPP Scatec simultaneously launched 333 MW of new solar across Botswana and South Africa, and signed a 1.95 GW PPA pipeline in Egypt.

The pattern is consistent: bankable markets with stable PPAs, creditworthy offtakers, and development bank support attract capital. The remaining 47 countries scramble for the rest.

—

## The Desert to Power Gap

The AfDB’s Desert to Power Initiative — a flagship $20 billion programme targeting 10 GW of solar across 11 Sahel and savannah nations — illustrates the ambition-execution gap at its most visible. Launched with considerable fanfare, the programme had approved financing for only 225.5 MW of capacity as of late 2025 — less than 3% of its 10 GW target, according to the Energy for Growth Hub.

The fifth ministerial meeting in June 2025 marked real governance progress: six member countries approved a joint IPP protocol and a strategy for green mini-grids. Mauritania signed a $300 million IPP deal for a 60 MW hybrid solar-wind plant under the programme. But the rate of approval is far below what is required to meet the 2030 objective.

—

## The Outlook: Records Without Revolution

Africa’s 4.5 GW solar record in 2025 is a genuine achievement. It reflects falling module prices, improving regulatory frameworks in markets like South Africa and Nigeria, and years of capacity-building by development finance institutions. The Global Solar Council projects Africa could reach 33 GW of cumulative solar capacity by 2029 — a realistic target if the pipeline under construction converts.

But the financing architecture needed to scale beyond the continent’s top five markets does not yet exist at sufficient depth. The IEA estimates Africa needs $28 billion in concessional capital to mobilise the $90 billion in private clean energy investment required through 2030. Current concessional flows are a fraction of that.

Post-COP30, the Belém Package committed to tripling adaptation finance by 2035 and mobilising $50 billion per year through the Africa Climate Innovation Compact. Whether these commitments translate into bankable deals in Burkina Faso, Niger, or the Democratic Republic of Congo — rather than solar farms in Cairo and Johannesburg — will determine whether Africa’s clean energy record year becomes a genuine turning point or simply a faster version of the status quo.

—

*Sources: Global Solar Council Africa Solar Report, February 2026; IEA World Energy Investment 2025; Climate Policy Initiative Landscape of Climate Finance in Africa 2024; IEA Financing Clean Energy in Africa; Energy for Growth Hub Desert to Power Reality Check; African Development Bank; IFC/Zafiri platform announcement; PV Magazine Africa pipeline data; African Energy Indaba, March 2026.*

—

**Word count:** ~1,050

**Filed to:** Technology Desk Editor for review

**Draft file:** `articles/beta-504-africa-solar-record-financing-gap-2025.md`