AfDB Backs Saviu Ventures — Development Finance Enters Francophone Africa VC

The African Development Bank’s €6.5 million commitment to Saviu II marks a structural shift: the continent’s flagship development lender is now a named LP in a fund built entirely around Francophone Africa’s underserved startup ecosystem.

By Kwame Asante, Business Reporter | BETAR.africa | 11 March 2026

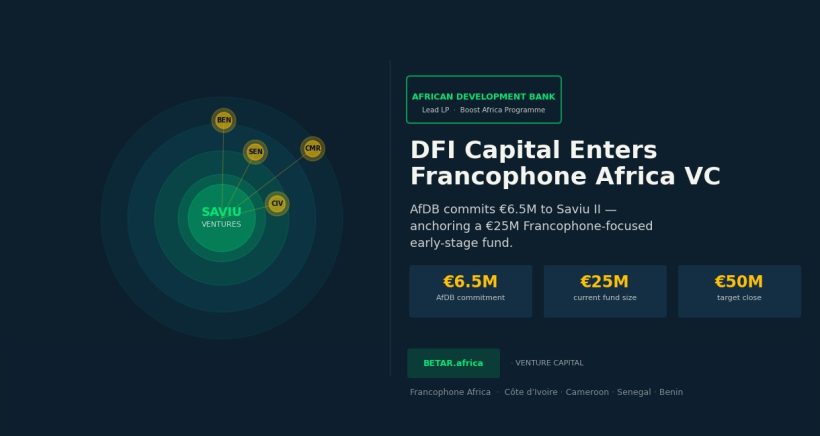

When the African Development Bank’s board of directors approved a €6.5 million investment in Saviu Ventures’ second fund on February 27, 2026, it did more than write a cheque. It placed an institutional imprimatur on a thesis that a small cohort of Francophone-focused investors have been building since 2018: that the startup ecosystems of Côte d’Ivoire, Cameroon, Senegal, and Benin are systematically underfunded — and that the gap is not a reflection of market quality, but of capital geography.

The commitment, confirmed in an AfDB press release on March 2, comprises €4.5 million from the Bank’s own balance sheet and a further €2 million deployed on behalf of the European Commission under the Boost Africa Programme — a blended finance instrument designed to absorb first-loss risk and crowd in commercial capital. The total package positions AfDB as one of the lead limited partners in a fund targeting a final close of between €30 million and €50 million.

A Fund Built for the Overlooked Majority

Saviu Ventures was founded in 2018 by Benoit Delestre and Samuel Touboul, both of whom came to African VC through routes that cut through the continent’s DFI infrastructure. Touboul spent time at Proparco, the French development finance institution and AFD subsidiary, before joining Saviu; Delestre built and exited two fintech companies in Europe before turning to early-stage investing in Francophone markets.

Their thesis has been consistent: seed to Series A, B2B tech-enabled businesses, ticket sizes of €500,000 to €3 million, with at least 60 percent of commitments deployed in Francophone West and Central Africa. That geography — encompassing Côte d’Ivoire, Cameroon, Senegal, Togo, Benin, and others — accounts for roughly 200 million people and a combined GDP larger than many better-covered markets, but has historically attracted a fraction of the venture capital flowing into Lagos, Nairobi, and Cairo.

Saviu I, the inaugural €10 million vehicle, closed in 2018 and built a portfolio of twelve companies including Julaya, the B2B neobank now considered a benchmark for Francophone West African fintech, and Lapaire, an eyewear retail chain operating across five countries in the sub-region.

Saviu II marked its first close at €12 million in November 2023 and reached €25 million by early 2025, with capital from the Dutch Good Growth Fund (DGGF), Proparco, and AXIAN Investment, the pan-African private group. The AfDB commitment, announced in March 2026, brings the vehicle within range of its lower-end final close target and carries a signal value beyond the euros.

Why AfDB’s Anchor Position Matters

Development finance institutions have shaped African VC since its earliest institutional iterations. The European Investment Bank and AfDB were the first movers in the mid-2010s, providing the catalytic capital that made funds like TLcom, Partech Africa, and Novastar viable for commercial LPs. But their involvement has historically clustered around pan-continental or Anglophone-focused vehicles.

A DFI of AfDB’s scale taking a named LP position in a fund with a mandate explicitly restricted to Francophone markets is a different signal. It validates the market segmentation argument — that Francophone West and Central Africa is not merely an emerging allocation within a broader Africa fund, but a distinct investable universe requiring dedicated capital and local expertise.

“The AfDB’s commitment signals that multilateral development finance is moving from observer to active participant in Francophone Africa’s venture ecosystem,” Benoit Delestre, Managing Partner of Saviu Ventures, said at the time of the fund announcement. “For our portfolio companies, it changes the conversation — they can now point to the continent’s flagship development institution as a vote of confidence in their markets.”

The blended finance structure reinforces this. By deploying the European Commission’s Boost Africa tranche as a first-loss layer, AfDB is effectively subsidising the risk profile for subsequent commercial investors. That architecture — DFI first-loss, then commercial LP capital — is the standard playbook for unlocking private capital into high-risk, high-potential markets. Its application here suggests institutional consensus that Francophone Africa VC is at an inflection point analogous to where pan-African VC was a decade ago.

The Pipeline It Unlocks

The interest in Francophone markets extends beyond Saviu. Teranga Capital, the Senegal-focused private equity manager, secured DFI backing from Proparco in late 2025 — including a portfolio guarantee instrument that functions similarly to the Boost Africa first-loss mechanism. JANNGO Capital, co-founded by Fatoumata Ba, has anchored a number of Francophone-market deals including co-leading GoCab’s $45 million mobility fintech round in February 2026 alongside E3 Capital — a raise that underscored both the appetite for the region and the growing depth of the investor bench.

Saviu’s own pipeline reflects the maturation. Beyond early portfolio wins like Julaya and Lapaire, the fund has backed Paps, the Senegal logistics platform; Waspito, a Cameroon-based healthtech; and Workpay, the Kenya-headquartered HR and payroll platform that has since extended its infrastructure to serve employers across Francophone West African markets including Côte d’Ivoire and Senegal. The geographic breadth of that list — extending beyond Côte d’Ivoire into Central Africa and even Anglophone East Africa — reflects an investment universe that is expanding as founders increasingly build cross-border from Francophone bases.

The Institutional Capital Stack Shifts

The Saviu II LP table is itself a map of where development finance is moving. DGGF is a €350 million Dutch impact vehicle extended through 2029 with an active Francophone mandate. Proparco has accelerated its VC commitments across the continent following AFD’s broader strategic push into digital economy investments. AXIAN, headquartered in Madagascar with operations across francophone markets, brings the commercial LP validation that pure DFI tables often lack.

Ghana adds a further dimension. In May 2025, Ghana’s National Pensions Regulatory Authority issued investment guidelines requiring pension funds to allocate a minimum five percent of assets under management to domestic private equity and venture capital by 2026 — the first African country to mandate, not merely permit, such allocations. With Ghanaian pension assets exceeding GH¢86 billion at end-2024 (NPRA Annual Report, 2024), the directive could unlock over $300 million for the domestic VC and PE ecosystem. It also signals that institutional capital beyond DFIs is being formally directed toward the asset class.

The cumulative effect of AfDB’s Saviu commitment, the Ghana pension directive, and the JANNGO-led GoCab raise is a Francophone investment climate that is beginning to resemble — structurally, if not yet at scale — the institutional depth that Anglophone hubs built over the previous decade. The money is following the thesis.

Reporting by Kwame Asante, Business Reporter, BETAR.africa. Primary sourcing: AfDB official press release (2 March 2026), Saviu Ventures fund announcement, and fund manager public statements. Delestre quote sourced from Saviu Ventures second-close announcement statement (early 2025). Additional sourcing: NPRA Investment Guidelines (May 2025); NPRA Annual Report (2024); AVCA member disclosures; Proparco press releases.