Africa’s Fashion Design Economy: The Margin Squeeze Behind a $31 Billion Market

African designer brands are capturing global attention, but the economics of building a viable business reveal an industry structurally constrained by imported raw materials, unreliable infrastructure, and e-commerce platforms still searching for a sustainable model.

By Creative Economy Desk | BETAR.africa

Filed: 11 March 2026 | Publication target: W/C 6 April 2026

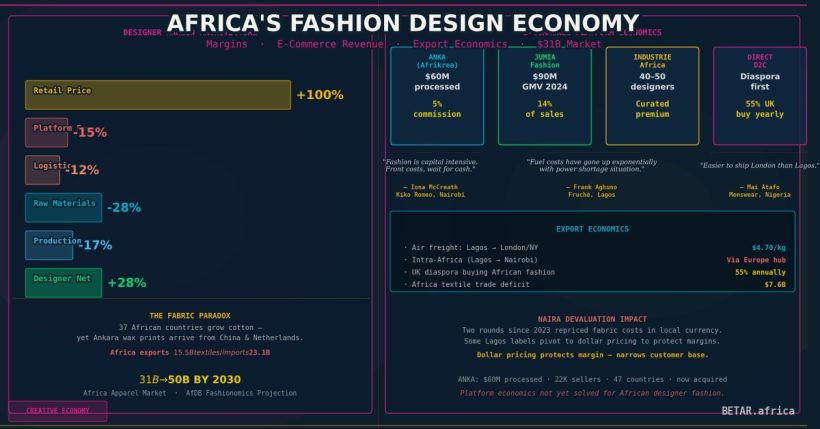

Africa’s apparel market is worth an estimated $31 billion — a figure the African Development Bank’s Fashionomics Africa programme projects will reach $50 billion by 2030. UNESCO’s 2023 global fashion report put the continent’s annual textile exports at $15.5 billion and forecast a 42% increase in demand for African haute couture over the next decade, driven by diaspora consumers and a growing premium placed on provenance in global fashion markets.

The commercial opportunity is not in doubt. What the headline figures obscure is where the money actually goes — and how little of it typically reaches the designers at the centre of the industry’s international narrative.

The E-Commerce Platform Equation

The most data-rich window into African fashion’s commercial architecture is ANKA, the Côte d’Ivoire-founded marketplace formerly known as Afrikrea. Over its operating life, the platform processed $60 million in total transaction volume and connected 22,000 sellers from 47 African countries to global buyers — a significant proof point for demand. By 2024, ANKA had reached $4.1 million in annual revenue and claimed to have broken even on a SaaS model that charged sellers approximately 5% commission on order value, one of the lowest take-rates of any fashion marketplace globally.

The low commission was a deliberate strategic choice to attract African designers who operate on thin margins — but it was not sustainable at scale. In May 2024, ANKA shut down its consumer-facing marketplace, citing inflation, deteriorating payment infrastructure across African markets, and rising logistics costs. The SaaS business — tools for designers to manage their own storefronts and customer relationships — continued, but the marketplace that had become the sector’s flagship digital retail venue closed.

By October 2025, the platform had been acquired in a bankruptcy process by New York-based Global Shop Group. Matilda Ceesay, the acquiring company’s CEO, framed it as a mission acquisition: “I deeply believe in what this platform represents: a powerful movement that has connected African and diaspora creators to customers worldwide.” For the 22,000 sellers who had built their digital presence on ANKA’s infrastructure, the transaction underscored the structural fragility of the Africa-facing D2C e-commerce model.

The ANKA trajectory is instructive. Jumia Fashion, operating at the mass-market end of the spectrum, generated an estimated $90 million in fashion GMV in 2024 — approximately 14% of Jumia’s total $641.9 million in platform sales. But Jumia’s fashion inventory is dominated by imported fast fashion and generic apparel rather than African designer labels, which require a different commercial infrastructure: curation, brand storytelling, and a buyer willing to pay a premium.

Industrie Africa, a curated B2C marketplace founded by Nisha Kanabar that stocks 40 to 50 designers across 12 African countries, operates on what it describes as “above-standard margin splits” with designers, though it has not publicly disclosed its commission structure. The gap between what platforms say and what they publish reflects an industry where commercial terms remain opaque, making it difficult for designers to benchmark their own business models.

The Margin Structure Problem

Across standard fashion industry pricing, the keystone model applies: production cost doubles to wholesale price, which doubles again to retail recommended price. A garment costing $50 to make becomes a $100 wholesale item and a $200 retail item. For mid-tier brands, multipliers of 2.5x to 3x on COGS at wholesale — and a further 2x at retail — generate gross margins of 30% to 60%, before operating costs.

African designer brands nominally follow this structure. In practice, their cost of goods sold is structurally higher — and more volatile — than the formula assumes.

Iona McCreath, founder of Nairobi-based label Kiko Romeo, frames the cash flow challenge directly: “Fashion is a very capital intensive industry in which you have so much money tied up in stock. You have to front those costs as a designer.” That capital intensity is amplified when raw material costs are denominated in foreign currency.

Frank Aghuno, founder of Lagos-based label Fruché, has pointed to the compounding effect of energy costs on production economics: “Fuel prices have gone up exponentially, especially with the power shortage situation.” In markets where industrial electricity is unreliable, fashion production facilities run on diesel generators — a cost that does not appear in Western margin benchmarks.

For Nigerian designers specifically, two rounds of naira devaluation since 2023 have repriced fabric and trim costs in local currency terms, compressing margins on any inventory purchased before the devaluations. Some labels have responded by shifting to dollar-denominated pricing for international sales. Ian Audifferen of Lagos-based Tzar Studios described the calculus: “When there’s that quality stamp on it, people pay if they can afford it.” Dollar pricing protects margin but narrows the accessible customer base.

The Fabric Paradox

The structural irony of African fashion economics is embedded in its raw materials. Thirty-seven of Africa’s 54 countries produce cotton. The continent accounts for 7.3% of global organic cotton production, with output growing 90% between 2019 and 2020. Yet the fabric most associated with African fashion — Ankara wax print — is predominantly manufactured in China and the Netherlands, then imported to West Africa where it is sold to designers whose input costs are therefore priced in euros or yuan.

In Kenyan retail markets, Ankara fabric trades at between 250 and 2,000 Kenyan shillings per yard ($1.90 to $15.50), with premium Dutch wax prints commanding the highest prices. For designers building collections around Ankara, kente, or adire, the raw material cost base fluctuates with exchange rates they cannot hedge.

UNESCO’s 2023 trade data quantifies the structural disconnect: Africa exports $15.5 billion in textiles annually but imports $23.1 billion in textiles, clothing, and footwear — a $7.6 billion deficit that reflects the continent’s limited spinning, weaving, and printing capacity. African designers are, in economic terms, paying a processing premium to source the materials most associated with their own creative identity.

Export Economics: Diaspora Demand vs. Intra-African Barriers

The strongest commercial pull for African designer exports is the diaspora. Research cited by African Business found that 55% of the African diaspora in the UK purchase at least one item of African-branded apparel per year, representing a consistent premium consumer segment with established demand and international purchasing power.

Logistics costs for serving that demand are manageable. Air freight from Nigeria to the UK or US runs at approximately $4.70 per kilogram at baseline commercial rates — meaningful for a small label shipping individual orders, but workable at scale.

Intra-African trade is a different equation. Mai Atafo, one of Nigeria’s most commercially successful menswear designers, has stated plainly: “It’s actually easier to deal with someone in the UK and US than someone within Africa. The excise duties for sending goods from Lagos to Nairobi doesn’t make it profitable.” Routing cargo between major African cities frequently requires transiting through European hubs, adding both cost and transit time. The result is that pan-African commercial scale remains largely aspirational for designers who cannot absorb the logistics overhead.

The IFC estimates that only 12% of African small businesses directly export. Most African fashion designers reach international markets through intermediaries — either diaspora buyers who carry items on trips home, or international stockists who absorb the logistics complexity in exchange for margin.

Cross-border e-commerce in African creative goods is growing at an estimated 25% annually, but the ANKA experience demonstrates that aggregating that demand into a viable marketplace model is not straightforwardly profitable. Instagram remains the primary sales channel for approximately 60% of African fashion brands — direct social commerce that avoids platform fees but also avoids the infrastructure, logistics management, and customer acquisition tools that marketplace models provide.

The Scaling Constraint

The Afreximbank Canex programme, which has directed a $2 billion creative industries fund toward African fashion and wider creative sectors, has documented what designer scaling looks like in practice. Vanhu Vamwe, a Zimbabwe-based label, grew from zero to approximately 50 international stockists following Canex investment and competition prize support. The AfDB’s Fashionomics Africa Investment Readiness programme offers seed grants of up to $20,000 per finalist designer in its accelerator cohorts.

The capital scale required to move from artisanal label to growth-stage brand — production capacity, inventory financing, logistics infrastructure, marketing — remains the principal constraint. Omoyemi Akerele, founder of Lagos Fashion Week and one of the industry’s most consistent voices on commercial development, has noted that the sector’s institutional momentum is real: “People increasingly seek products ‘Made in Africa’ as symbols of pride and identity affirmation.” Converting that affirmation into repeatable revenue at scale is the unsolved economic problem that the $50 billion market projection depends on answering.

Data sources: African Development Bank Fashionomics Africa; UNESCO Creative Economy Report 2023; IFC ANKA investment release; TechCabal; Business of Fashion; Semafor; Statista Apparel Africa Market Outlook 2025–2029; OkayAfrica.