South Africa’s Platform Tax Pivot: Budget 2026 Makes Digital Marketplaces the VAT Collector

By BETAR.africa Policy & Regulation Desk

Published: March 2026

Beat: Digital Taxation | Issue: BETA-571

South Africa’s 2026 Budget, tabled on February 25, 2026, contains a VAT measure that has received far less attention than the headline threshold changes — but will matter significantly more to foreign platform operators doing business in South Africa.

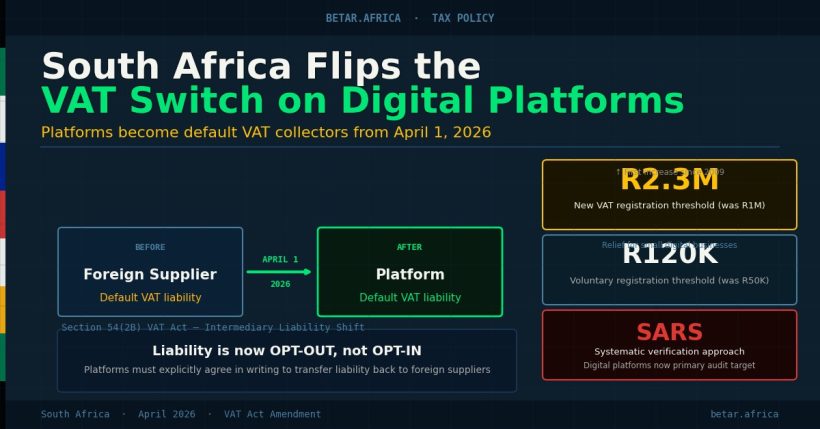

The proposed amendment would shift the default VAT liability for electronic services from individual suppliers to the intermediary platform operators through which those services are delivered. If enacted, this means platforms — not the drivers, freelancers, or sellers using them — become the first party responsible for accounting for and remitting VAT to the South African Revenue Service (SARS).

This is not a tax increase. It is a structural re-engineering of who hands the money to the government. For large platforms, that distinction carries significant compliance cost.

What the Budget Actually Says

The February 2026 Budget Review states that government intends to “refine the way VAT is accounted for when foreign suppliers use intermediary platforms to reach South African consumers” and to clarify “who is responsible for accounting for VAT” when digital services flow through intermediary structures.

The proposed change establishes a default rule: the intermediary platform operator accounts for VAT on electronic services, unless the parties to the transaction agree otherwise in writing. That opt-out clause matters — it allows platforms to contractually designate the underlying supplier as the VAT-responsible party — but it places the compliance burden of documentation and contractual management on the platform.

The Taxation Laws Amendment Bill, which typically enacts Budget proposals by November or December of the same year, is expected to contain the implementing provisions.

Who Is Affected

The affected universe is wide. The VAT Act’s definition of “electronic services” covers digital content, streaming, cloud services, software-as-a-service, online marketplaces, and — critically — intermediated transactions where a platform earns a fee for connecting a buyer and seller or a rider and driver.

Ride-hailing platforms. Uber and Bolt are the most visible affected operators. Both platforms already face a separate — and more immediately pressing — regulatory deadline under the National Land Transport Amendment Act, which required all e-hailing operators to register with the National Public Transport Regulator by March 11, 2026. As of early March, only three of twelve registered operators had completed the process, though Bolt confirmed it received its certificate of registration on February 27, 2026. The 2026 Budget VAT amendment adds a second compliance dimension: once enacted, Uber and Bolt would need to ensure VAT on ride fees is accounted for at the platform level, rather than by individual driver-partners.

Online marketplaces. Platforms intermediating goods or services sales — including marketplace operators in South Africa and foreign e-commerce platforms with South African customer bases — will need to map their transaction flows to determine whether the platform operator or the individual seller is liable.

SaaS and digital subscription services. Software platforms that distribute third-party applications or content (app stores, software marketplaces, content distribution networks) face the clearest compliance obligation under the proposed default rule.

Online learning and freelance platforms. EdTech platforms hosting independent instructors, and freelance marketplaces connecting contractors with clients, operate squarely within the affected category.

The April 2025 Layer: B2B is Already Different

To understand the 2026 amendment, it is necessary to understand what changed in April 2025. Regulations effective April 1, 2025 excluded business-to-business electronic services from the definition of “electronic services” for VAT purposes, where all South African recipients are VAT-registered vendors. This means foreign SaaS companies supplying only to VAT-registered South African businesses no longer need to register for VAT.

The B2B exclusion and the 2026 platform operator liability amendment operate on different axes. The B2B exclusion addresses whether registration is required; the platform amendment addresses who accounts for VAT when the end consumer is an individual (B2C). Together, they create a cleaner structure:

- – B2B transaction, no platform intermediary: Foreign supplier may be exempt from registration if all clients are VAT-registered.

- – B2C transaction through a platform: Platform operator is the default VAT-responsible party under the 2026 amendment.

The risk zone is mixed-customer platforms — those serving both registered businesses and individual consumers. The B2B exclusion is an all-or-nothing rule: a single non-VAT-registered customer negates the exemption. Platforms that cannot cleanly segregate their customer bases will need to ensure full platform-level VAT accounting.

The EU Comparison: South Africa Is Not First

South Africa’s move aligns with a global trend accelerated by the European Union’s ViDA (VAT in the Digital Age) package, which makes EU-based platforms the deemed supplier and default VAT accountable party for services intermediated to consumers. The EU’s DAC7 directive also imposed transaction reporting obligations on digital platforms.

The OECD’s Model Rules for Reporting by Platform Operators, published in 2020, provided the international template that both the EU and — increasingly — African jurisdictions are adopting. South Africa’s approach tracks the OECD model more closely than the EU’s more prescriptive implementation, but the compliance implications for multinational platform operators are substantively similar.

For platforms already complying with EU or UK digital services VAT rules, South Africa’s amendment should require incremental rather than structural compliance investment. The risk is assuming that existing global compliance frameworks automatically satisfy South African requirements — SARS operates a distinct registration, return, and payment regime.

Compliance Action Items

1. Map your transaction flows. Identify every instance where your platform intermediates a supply of electronic services to South African consumers. Determine whether the current VAT-responsible party is the platform or the underlying supplier.

2. Review your contracts. The opt-out mechanism requires written agreement. If you want underlying suppliers to remain VAT-responsible, document this in your standard supplier terms before the Taxation Laws Amendment Bill is enacted.

3. Assess B2B segregation. If you serve both business and individual clients in South Africa, evaluate whether you can cleanly ring-fence B2B transactions for the B2B exclusion. If not, assume the general rules apply to your full South African customer base.

4. Register if not already registered. Foreign-based platform operators with South African consumer transaction volumes above the R1 million threshold (R2.3 million from April 1, 2026) that are not yet registered with SARS should register now. The amendment increases exposure, not thresholds.

5. Monitor the Taxation Laws Amendment Bill. The effective date will be confirmed when the Bill is gazetted, typically mid-year, with enactment by November or December 2026. Use the remaining window to remediate compliance gaps.

The Broader Picture

South Africa’s 2026 Budget delivers multiple regulatory signals to the digital economy simultaneously: a significant VAT threshold increase for small businesses (from R1 million to R2.3 million), relief for the SMME sector, and a tightening of the platform accountability framework for large operators. The direction is consistent — reduce the compliance burden for small, locally-registered businesses; increase it for large, often foreign, platforms that have historically benefited from the complexity of indirect supply chains.

For digital platform operators in South Africa, February 25, 2026 was a date that passed quietly. The Taxation Laws Amendment Bill later this year will make clear it should not have.

Sources:

– South African National Budget Review 2026, National Treasury, 25 February 2026

– BDO: “South Africa — 2026 Budget Includes VAT Measures Affecting SEZs and Digital Platform Operators”, March 2026

– EY: “South Africa publishes amendments excluding certain B2B transactions from electronic services for VAT purposes”, April 2025

– Global VAT Compliance: “South Africa VAT digital services rules updated for 2025”, 2025

– Innovation Village: “South Africa Gives Uber and Bolt Until March 2026 to Comply With New Transport Law”

– ITWeb: “Only three of 12 e-hailers registered in SA as deadline looms”, March 2026

– OECD Model Rules for Reporting by Platform Operators, 2020

– EU ViDA (VAT in the Digital Age) Package, European Commission