South Africa’s Spectrum Auction Returns: The 6GHz Battleground That Will Define 5G

ICASA is preparing its second major spectrum auction in five years, targeting six frequency bands for release in the 2026/27 financial year. The contested 6GHz band — where mobile operators want 5G expansion room and the WiFi industry wants unlicensed access — has turned a routine licensing process into a regulatory fight with direct consequences for how South Africa’s SMEs pay for connectivity.

South Africa’s telecoms regulator is moving forward with a spectrum auction that will shape the country’s mobile broadband landscape for the next decade. The Independent Communications Authority of South Africa (ICASA) has confirmed plans to release spectrum across six frequency bands in the 2026/27 financial year, with a consultant appointment expected before the end of March 2026 to manage the auction process.

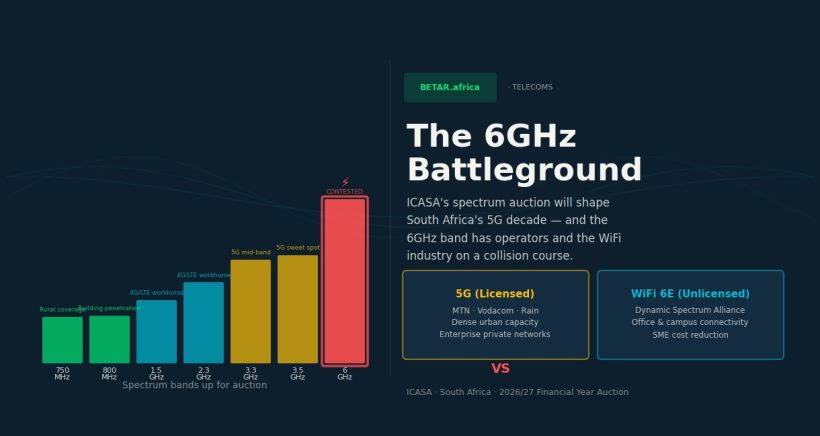

The bands on offer span a wide range of use cases: 750MHz and 800MHz (low-band, ideal for rural coverage and building penetration), 1.5GHz and 2.3GHz (mid-band, current 4G/LTE workhorses), and 3.3GHz and 3.5GHz (mid-band 5G, the global sweet spot for capacity and coverage balance). A separate proceeding on the 6GHz band is running in parallel — and it is that process that has drawn the fiercest industry attention.

Why the 6GHz Band Matters More Than the Others

The 6GHz band (5.925–7.125GHz) is the single largest block of contiguous mid-band spectrum available globally, and regulators worldwide are dividing sharply on how to use it. The choice is binary: allocate it to licensed mobile operators for 5G expansion, or release it as unlicensed spectrum for WiFi 6E (and its successor, WiFi 7), which any device can use without a licence fee.

South Africa’s mobile operators — primarily MTN, Vodacom, and Rain — are lobbying strongly for licensed mobile use. Their argument is that licensed 5G in the 6GHz band would enable the dense urban capacity needed to support enterprise 5G applications, private networks, and the fixed wireless access products that have become core revenue streams for all three operators.

The WiFi industry and enterprise tech lobby, represented through bodies aligned with the Dynamic Spectrum Alliance and domestic technology associations, are pushing for unlicensed access. Their argument: WiFi 6E delivers faster, cheaper indoor connectivity for offices, campuses, and industrial facilities — directly benefiting the SME sector and reducing dependence on mobile carrier pricing. The United States, Brazil, Saudi Arabia, and South Korea have already designated the 6GHz band as unlicensed. The European Union has opted for a hybrid approach, with the lower portion unlicensed and the upper portion still under review.

ICASA has not yet signalled which path South Africa will take.

The Operator Calculus: MTN, Vodacom, and Rain

For MTN South Africa, spectrum strategy is inseparable from its broader fixed wireless access (FWA) push. The operator has been rapidly expanding its 5G Home and Business Internet products — FWA services that use mobile 5G infrastructure to replace fibre for last-mile broadband. Additional mid-band spectrum in the 3.5GHz or 6GHz range would allow MTN to densify its 5G network without the capital cost of new tower builds. Sources familiar with MTN’s spectrum planning describe 3.5GHz as “runway” and 6GHz as “the next decade’s capacity reserve.”

Vodacom’s calculus is similar but complicated by its fibre commitments. As one of South Africa’s major FTTH operators, Vodacom has less incentive to cannibalise its own fixed network with aggressive FWA expansion. Its spectrum strategy at this auction is expected to prioritise defence — securing enough mid-band holdings to maintain competitive parity with MTN on 5G performance — rather than aggressive capacity acquisition.

Rain occupies a distinct position. The operator has built its entire business model around 5G and has no 2G/3G/4G legacy network to manage. Rain’s spectrum needs are acute: it currently holds a single 100MHz block in the 3.5GHz band and is widely expected to be an aggressive bidder for additional 3.5GHz and 6GHz spectrum. Analysts tracking the auction suggest Rain could be willing to outbid the larger operators on specific blocks to secure the spectrum it needs to scale its enterprise 5G offering and prevent a capacity ceiling from capping its growth trajectory.

Signal Distribution Reform: The Parallel Proceeding

Running alongside the spectrum auction is a separate ICASA process examining signal distribution regulation reform — the regulatory framework governing how signals are transported across South Africa’s broadcasting and telecoms infrastructure. This proceeding has drawn less public attention than the spectrum auction but has potentially larger structural implications.

At issue is the regulatory treatment of signal distributors like Sentech, which operates South Africa’s national broadcast transmission infrastructure, in an environment where IP-based content delivery has made legacy broadcast distribution economics increasingly fragile. Reforms could restructure access obligations and pricing for infrastructure that underpins both public broadcasting and commercial telecoms — an outcome that would affect the cost base of every mobile operator in the market.

What This Means for SME Connectivity Pricing

The 6GHz decision carries direct business consequences that extend well beyond the operators competing in the auction.

If the band is licensed to mobile operators, the additional 5G capacity should eventually lower the cost of mobile data — but the benefit flows primarily through operator pricing decisions that have historically lagged capacity gains. Enterprise and SME customers would access that capacity through carrier contracts, preserving operator margin structure.

If the band is released as unlicensed spectrum, the effect is more immediate and democratising: WiFi 6E routers operating in 6GHz deliver gigabit-class speeds across campuses, office parks, and commercial premises using cheap commodity hardware. An SME with a R3,000 access point could self-provision enterprise-grade connectivity without purchasing a carrier data plan. This scenario is a direct threat to the mobile operators’ fixed wireless access revenue line — which explains the intensity of their opposition.

The pricing stakes are not abstract. South Africa has the highest mobile data prices among comparable middle-income economies after adjusting for purchasing power. A 2025 Research ICT Africa study found that 1GB of mobile data in South Africa costs 3.2 times the equivalent in Kenya and 2.1 times the equivalent in Nigeria. Any regulatory decision that either compresses or preserves that pricing structure will have material consequences for the roughly 2.5 million SMEs that depend on mobile connectivity as their primary business internet.

Timeline and Process

ICASA’s timeline for the auction remains subject to the consultant appointment and the ongoing Information Memorandum process. Based on the 2026/27 financial year target, the auction is unlikely to conclude before the second quarter of 2026, with spectrum assignments potentially taking effect from mid-2026 at the earliest.

The 6GHz decision may be decoupled from the main auction and resolved through a separate regulatory proceeding, given the complexity of the policy choice and the active international debate. ICASA has previously used the ITU World Radiocommunication Conference (WRC-27) process as a reference point for contested spectrum decisions — meaning a final call on 6GHz might not come until after the WRC-27 decisions are published in late 2027.

For the operators, the uncertainty is itself a planning risk. Investment decisions around 5G network densification, enterprise private network proposals, and FWA product roadmaps are all contingent on the 6GHz outcome. The longer ICASA defers, the more capital planning at all three major operators stalls.

The Bigger Picture

South Africa’s 2026/27 spectrum auction is the latest chapter in a long-running story of regulatory lag in one of Africa’s most sophisticated — and most expensive — telecoms markets. The 2022 Rapid Policy Intervention spectrum assignment, while welcomed, was widely seen as years overdue, and the operators that benefited have been vocal about the competitive disadvantage they carried during the delay.

This auction’s outcome will determine whether South Africa’s 5G infrastructure remains concentrated in the hands of the three incumbent mobile operators, or whether unlicensed 6GHz creates a parallel connectivity layer that structurally lowers the floor on business connectivity costs. The 6GHz decision, in particular, is a genuine policy choice — not a technical inevitability — and ICASA’s position on it will define the regulator’s philosophy on spectrum governance for a generation.

BETA-522 | [TELECOMS-REG] | Policy & Regulation Desk