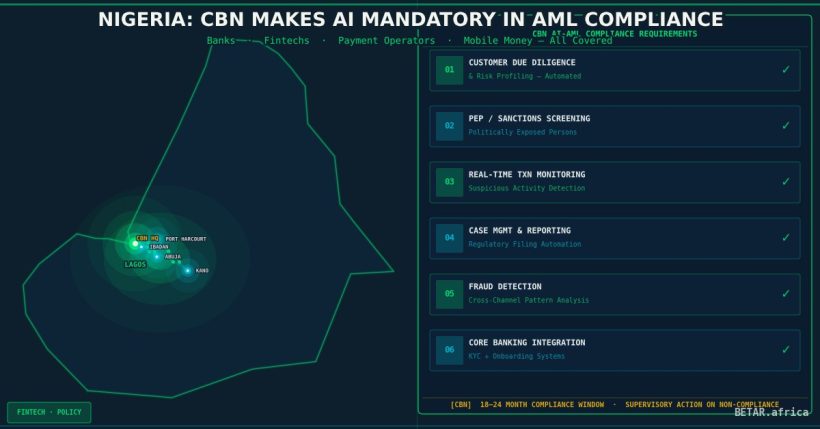

Nigeria has become one of the first African countries to formally mandate AI-powered anti-money laundering systems — not just permit them. A Central Bank of Nigeria circular dated March 10, 2026 sets baseline standards that require banks, fintechs, mobile money operators, and international money transfer operators to deploy automated, AI-driven AML infrastructure within 18 to 24 months, depending on their licence category.

The standards do not describe a technology preference. They describe a compliance architecture: what an institution’s AML system must do, how it must be validated, and what happens when it fails.

What the Standards Require

The CBN’s baseline AML standards apply to six functional domains that any compliant system must address:

1. Transaction monitoring

Institutions must deploy automated systems capable of generating alerts on suspicious transaction patterns in real time or near-real time. The use of AI and machine learning to identify anomalies — velocity patterns, network relationships, atypical transaction amounts — is formally recognised and encouraged. Rule-based systems alone will no longer meet the standard.

2. Case management

Alert outcomes must be tracked through a documented workflow: triage, investigation, escalation, and disposition. The system must maintain an audit trail that the CBN can examine during off-site surveillance or on-site examination.

3. KYC and KYB processes

Know-Your-Customer and Know-Your-Business requirements must be integrated with the AML system — not operated in parallel silos. Customer risk profiles must be dynamically updated based on transaction behaviour, not just at onboarding.

4. Sanctions and PEP screening

Politically Exposed Person (PEP) lists and sanctions databases must be checked at onboarding and updated continuously. The system must flag changes in customer PEP status or sanctions exposure between onboarding and transaction execution.

5. Audit trails and data security

Every system action — alert generation, case disposition, escalation decision — must be logged in a tamper-evident audit trail. Data security standards for AML system records align with CBN’s existing data governance requirements.

6. Vendor management

Institutions that source their AML system from a third-party vendor must maintain oversight of the vendor’s model accuracy, update cadence, and service continuity. The CBN holds the institution responsible for its AML system’s performance regardless of whether the system is built in-house or licensed.

The AI Accountability Requirement

The most significant new obligation in the standards is the independent annual validation requirement. Any institution deploying AI or ML models in its AML system must commission an independent review — annually — that assesses:

- Accuracy: Is the model correctly flagging suspicious activity without an unmanageable false positive rate?

- Bias testing: Is the model producing systematically different alert rates for customers in identifiable demographic segments, and if so, why?

- Model drift: Has the model’s performance degraded since its last update, and is it still calibrated to current transaction patterns?

This requirement moves AI governance from a theoretical concern to a regulatory obligation. In most markets, AI model validation is an internal risk management practice. In Nigeria, under these standards, it becomes an externally reportable requirement — one that the CBN will examine during thematic reviews.

For institutions that have deployed vendor-provided AML models, the annual validation requirement applies to the vendor’s model. A fintech that has licensed a transaction monitoring system from an identity/compliance vendor cannot outsource its CBN audit readiness to that vendor. The institution must be able to present independent validation findings.

Deadlines and Filing Requirements

The circular establishes a tiered compliance timeline:

| Institution type | Compliance deadline |

|---|---|

| Deposit Money Banks (DMBs) | 18 months from circular date (~September 2027) |

| Mobile Money Operators | 24 months (~March 2028) |

| International Money Transfer Operators | 24 months (~March 2028) |

| Payment Service Providers | 24 months (~March 2028) |

| Other financial institutions | 24 months (~March 2028) |

Critically, all institutions — regardless of tier — must submit an implementation roadmap to the CBN within 90 days of the circular’s issuance. This roadmap must describe the planned system architecture, vendor selection (if applicable), integration milestones, and validation approach.

The 90-day roadmap deadline falls in the first week of June 2026. Institutions that have not yet begun assessing their AML infrastructure are already behind.

Nigeria’s Position Relative to FATF Standards

The timing of the circular is not coincidental. Nigeria has been on the FATF grey list — meaning it is subject to increased monitoring for deficiencies in its AML/counter-terrorism financing framework — and has been working to exit. A formal, enforceable standard for automated AML systems strengthens Nigeria’s technical compliance posture under FATF Recommendation 10 (Customer Due Diligence) and Recommendation 20 (Reporting of Suspicious Transactions).

The CBN’s framing of AI and ML as formally recognised AML tools — rather than experimental supplements to a rule-based baseline — signals a compliance maturity claim: Nigeria’s financial sector is not just building AML systems, it is building defensible, independently validated ones.

FATF evaluators assess not just whether an institution has a suspicious transaction reporting function, but whether it is operationally effective. A system that produces alerts validated annually for accuracy is a more credible demonstration of effectiveness than a rule-based filter generating high false-positive volumes that compliance teams have learned to ignore.

What This Means for Nigerian Fintechs

The standards create a compliance cost hierarchy. For large DMBs with dedicated compliance technology teams and existing AML infrastructure, the circular primarily requires upgrading rule-based systems to AI-supplemented ones and commissioning the new annual validation process. Incremental.

For smaller fintechs — especially mobile money operators and PSPs — the circular may require building AML infrastructure from a low baseline. Many smaller Nigerian fintechs currently operate compliance functions that rely on manual review, vendor-provided rule sets, or basic transaction limits. The baseline standards describe a system architecture that many do not yet have.

The 24-month timeline for non-DMB institutions is more generous than the 18-month DMB window, but the 90-day roadmap obligation applies to all. Institutions that file an underdeveloped roadmap risk attracting early CBN attention before the compliance deadline arrives.

The market for AML-as-a-service and compliance infrastructure is likely to see significant demand from Nigerian fintechs over the next 18 months. Vendors who can offer NIBSS-integrated, CBN-audit-ready, independently validatable AML systems — with documentation structured around the CBN’s six-domain standard — will find a large, time-pressured captive market.

Enforcement Mechanism

The CBN has specified four oversight mechanisms:

- Off-site surveillance — ongoing monitoring of AML system outputs submitted in regulatory filings

- On-site examinations — physical review of system architecture, audit trails, and validation records

- Thematic reviews — sector-wide assessments focusing on specific compliance areas (e.g., PEP screening, transaction monitoring false positive rates)

- Sanctions — unspecified regulatory penalties for non-compliance or operating an ineffective AML system

The “operating an ineffective AML system” clause is notable. It means that institutions cannot achieve compliance simply by deploying a system. They must demonstrate that the system is performing effectively — a higher bar that the annual validation requirement is designed to provide evidence for.

The Bottom Line

The CBN’s AML baseline standards are a framework shift: from manual review and rule-based filters to AI-validated, annually assessed, audit-trail-documented systems. Nigeria is requiring its financial sector to build AML infrastructure that would be at home in a Tier 1 European banking compliance function — within 18 to 24 months, with roadmaps due in 90 days.

For fintechs that have grown fast on the assumption that compliance would remain a cost-efficient background function, the new standards reframe compliance as product infrastructure. What must be built, how it must be validated, and how it must be presented to regulators is now specified. The question is who builds it fast enough.

BETAR.africa tracks regulatory developments across all 54 African nations. Sources: CBN circular (March 10, 2026); TechCabal, Techeconomy, Channels TV, Innovation Village, VoveiD. Related: BETA-623 (CBN liveness checks), BETA-555 (CBN AI in AML — initial assessment), BETA-610 (NCC/CBN refund framework).