Africa’s First Carbon-Financed Clean Cooking Programme: How AfDB Is Using Carbon Credits to Replace Charcoal

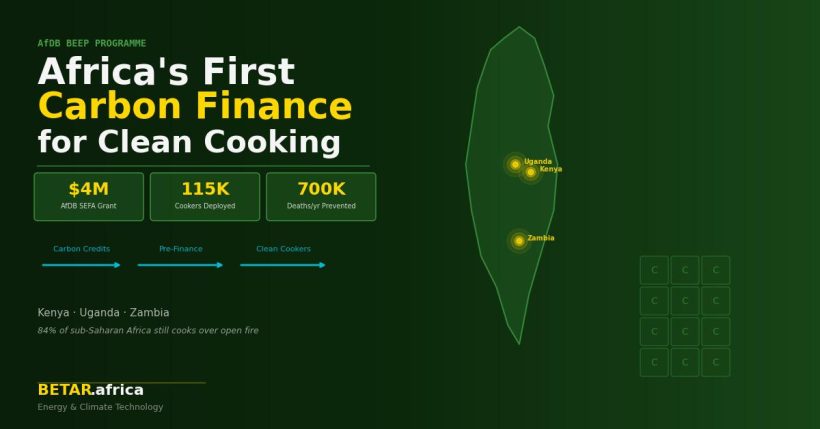

The African Development Bank’s $4 million SEFA grant anchors a $10 million blended vehicle that pre-finances induction cookers for 115,000 low-income households in Kenya, Uganda and Zambia — and recovers the cost through voluntary carbon market sales. It is the first time the AfDB has used carbon finance as a delivery mechanism for household energy access.

Every year, cooking kills more Africans than malaria. Smoke from charcoal stoves, wood fires and kerosene lamps — still the primary fuel source for 84 per cent of sub-Saharan households — contributes to an estimated 2.9 million deaths globally from household air pollution, with Africa bearing a disproportionate share. Women and children account for 60 per cent of early deaths attributed to smoke inhalation. And yet clean cooking has remained one of the continent’s most persistently underfunded energy transitions, squeezed between the difficulty of monetising household impact and the low margins of reaching low-income consumers at scale.

A new transaction from the African Development Bank — announced in July 2025 and now entering its active deployment phase — is attempting to fix both problems at once. As Africa’s climate finance debate broadens from utility-scale solar investment to the harder question of household energy access, BURN Manufacturing’s BEEP programme represents the most structurally sophisticated answer to that question yet attempted on the continent: a mechanism where carbon market revenues, not recurring grants, finance the cost of reaching low-income homes at scale.

In July 2025, the Bank’s Sustainable Energy Fund for Africa (SEFA) committed a $4 million reimbursable grant to BURN Manufacturing’s Burn Electric Cooking Expansion Program (BEEP) — the AfDB’s first-ever carbon finance transaction specifically designed for electric cooking. The structure is novel: rather than a direct subsidy, SEFA’s capital anchors a $10 million Special Purpose Vehicle (SPV) alongside a $5 million loan from the Spark+ Africa Fund and $1 million equity from BURN itself. That blended vehicle pre-finances the deployment of 115,000 BURN ECOA electric induction cookers to low-income, grid-connected households in Kenya, Uganda and Zambia — and the costs are recovered not from consumers, but from the sale of carbon credits on the voluntary carbon market.

The financing model: carbon credits as cost-recovery, not subsidy

The distinction matters. Africa has a long history of climate grant programmes that subsidise hardware into the market and then disappear when funding cycles end. BEEP is structured differently. BURN — already one of Africa’s largest voluntary carbon market participants and the first cookstove company to issue Carbon Credit Plus (CCP)-labelled credits — generates verified carbon credits when households switch from solid fuel cooking to electric induction. Those credits are sold on voluntary markets; the revenue pre-finances the upfront cost of each ECOA cooker before it reaches the consumer.

For the household, the ECOA induction cooker arrives through a Pay As You Cook (PAYC) model, integrated with mobile money platforms. The cooker retails at approximately Kshs. 14,000 (~$109) but is made accessible through daily repayment amounts of around Kshs. 240 (~$2), monitored via IoT sensors embedded in each unit. The carbon credit revenue effectively reduces the financing cost for BURN’s SPV — making the economics viable at a price point that households can sustain.

“SEFA plays a critical role in mitigating carbon market risks and enhancing the Programme’s financial sustainability,” the AfDB said in its July 2025 press release. For a market where voluntary carbon credit prices have been volatile and methodologies contested, that guarantee function is as important as the capital itself.

Why BURN, and why now

BURN Manufacturing has become Africa’s most capitalised clean cooking company over the past four years. The Nairobi-headquartered firm — which designs, manufactures and distributes cookstoves and induction cookers across more than ten African countries — secured a $15 million investment from the European Investment Bank in October 2024 to scale ECOA distribution in East Africa. BEEP adds a second major institutional backer and demonstrates the company’s ability to structure carbon finance alongside development bank capital.

The ECOA cooker itself is designed specifically for African grid conditions: it includes IoT connectivity for real-time energy monitoring, integrates directly with M-Pesa and other mobile money platforms, and is assembled at BURN’s Ruiru factory outside Nairobi. That local manufacturing base is significant — it means the carbon credits generated by switching households also support Kenyan manufacturing employment, a linkage that increasingly matters to impact investors applying ESG screens.

BURN’s carbon business is already at scale. The company is one of Africa’s largest issuers of cookstove carbon credits, selling verified emission reductions based on displaced charcoal and firewood use. The CCP label — the highest quality designation in the voluntary market — differentiates BURN’s credits from lower-quality issuances that have drawn scrutiny from buyers over the past two years.

The access gap BEEP is targeting

Sub-Saharan Africa had 923 million people without access to clean cooking in 2022, according to the International Energy Agency. That number has barely moved in a decade despite significant investment in the sector, because most interventions have focused on improved biomass stoves rather than genuine fuel switching. Electric cooking — where the IEA says the economic and health case is overwhelming — has been stalled by two linked barriers: appliance cost, and consumer uncertainty about electricity supply reliability.

BEEP addresses the first barrier directly through its carbon-financed PAYGo structure. On the second barrier, the programme targets grid-connected households specifically — a population that in Kenya, Uganda and Zambia is large enough to justify deployment at scale, but which has been left out of most off-grid mini-grid discussions. Targeting consumers who already have grid electricity but are still cooking with charcoal due to appliance cost is, in some respects, a lower-risk market than off-grid; the infrastructure problem is already solved.

The 115,000 cookers BEEP plans to deploy represent a meaningful fraction of the annual market. BURN has previously indicated that its goal is to reach one million ECOA households across East Africa within five years — a target it said would avoid 12 million tonnes of carbon emissions and benefit 6.5 million people directly. BEEP’s 115,000 units, delivered through a proven carbon finance channel, would account for more than a tenth of that target if executed on schedule.

Replication potential — and the carbon market question

The most consequential aspect of BEEP may be what it demonstrates for other markets and other actors. The AfDB holds SEFA grants of varying sizes across multiple clean energy programmes; the BEEP transaction establishes a template for channelling those grants into carbon-backed structures rather than straightforward subsidies. If the model works at 115,000 units — if carbon revenues genuinely cover SPV costs and households sustain repayment — then the same architecture could be replicated in Nigeria, Ghana, Tanzania and elsewhere with minimal modification.

The risks are real. Voluntary carbon markets remain opaque and price-volatile. Cookstove methodology disputes have resulted in credit invalidations for other issuers, though BURN’s CCP-labelled approach is specifically designed to address those concerns. PAYGo default rates in Africa’s clean energy sector average between 12 and 20 per cent depending on the market, which the SPV structure must absorb. And grid reliability in Zambia, in particular, remains uneven — which could affect actual electricity consumption data needed to generate verified credits.

But the ambition of the BEEP transaction is precisely to stress-test those assumptions at scale with institutional capital behind it. That is what development banks are supposed to do — take the first-mover risk so that private capital can follow. On that measure, the AfDB’s first carbon finance transaction for electric cooking is a bet worth watching.

Sources: AfDB press release, July 2025; BURN carbon blog; IEA Energy Access Outlook 2023; WHO Household Air Pollution fact sheet; Launch Base Africa, July 2025.