Africa Has the Battery Minerals. Morocco Has the Gigafactory. Here Is the Gap.

Gotion High-Tech’s Kenitra plant is a genuine milestone — the first battery cell gigafactory on the African continent. But the lithium arrives from Zimbabwe, the refining happens in China, and the cars go to Europe. The question mineral-rich African governments cannot afford to skip is why they are not in this story at all.

The factory exists. That part is settled. China’s Gotion High-Tech broke ground in May 2025 on a $5.6 billion battery gigafactory in Kenitra, Morocco — a complex that will reach 20 gigawatt-hours of production capacity in its first phase and 100 GWh at full scale, employing 10,000 people and supplying battery cells to Renault, Stellantis, and other European automakers assembled at Morocco’s adjacent automotive cluster. First production is scheduled for Q3 2026.

BETAR.africa covered the factory announcement when construction began. (BETA-542: Morocco Gotion Gigafactory: Africa’s First Battery Cell Plant.) The specs are on record. The question worth asking now — before first production, before the supply agreements are locked in, before the industrial narrative hardens into received wisdom — is a different one. The Kenitra gigafactory is the most significant battery manufacturing investment in Africa’s history. Does it benefit Africa?

The honest answer is: partially, selectively, and less than the headline suggests.

The Phosphate Argument — Real but Narrow

Morocco’s pitch to Gotion rested partly on minerals. Morocco holds roughly 70 percent of the world’s identified phosphate reserves — a genuine and significant resource position. Phosphate-derived lithium iron phosphate, or LFP, chemistry is the battery architecture Gotion uses. The argument runs: Morocco has the phosphates, LFP batteries need phosphates, therefore Morocco is a natural host.

The argument is real but considerably narrower than it sounds. LFP chemistry does use lithium iron phosphate as its cathode material, and Morocco’s phosphate reserves are a legitimate industrial input. But phosphate in raw or processed form is not battery-grade lithium iron phosphate cathode powder. The refinement steps between mined phosphate rock and finished cathode material are chemically intensive, require specialised processing infrastructure, and are currently dominated by Chinese producers with decades of process expertise.

More importantly: Morocco does not have lithium. LFP batteries need lithium as well as iron and phosphate. For Kenitra’s production volume, that lithium will come from somewhere else — primarily Zimbabwe, Chile, and Australia, refined through Chinese chemical processing chains before arriving in Morocco as battery-grade lithium carbonate or hydroxide. The phosphate logic gives Morocco a genuine but secondary minerals argument. The primary driver of Kenitra’s location is not minerals.

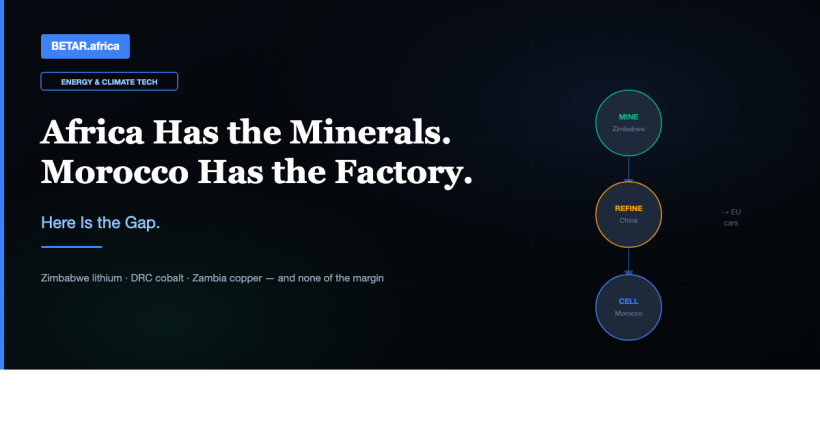

Where Gotion’s Lithium Actually Comes From

Zimbabwe holds some of the world’s largest and highest-grade hard-rock lithium deposits — Bikita, Arcadia, Zulu, and the Sabi Star complex among them. Chinese mining companies, including Sinomine, Chengxin Lithium, and Prospect Resources’ acquiring consortium, have invested heavily in Zimbabwean lithium extraction over the past three years. In late 2022, Zimbabwe imposed an export ban on raw lithium ore, designed to force in-country beneficiation — an attempt to capture value above the mine-gate.

The export ban is partial progress. Zimbabwe is now producing spodumene concentrate rather than raw ore — one processing step up the value chain. But concentrate is a long way from battery-grade lithium carbonate or hydroxide. That conversion happens in China, at facilities the same Chinese mining companies that own the Zimbabwean mines also operate on the mainland. The economic chain runs: Zimbabwe provides the rock, Chinese companies extract it and ship concentrate, Chinese refineries convert it, Chinese manufacturers incorporate it into LFP cathode powder, and that material travels to Morocco to be assembled into battery cells for European cars.

Zimbabwe earns royalties and some beneficiation margin on the concentrate step. The margin on refining, cathode production, and cell assembly — the majority of the battery value stack — accrues in China. This is not a Moroccan failure. It is the structure of the current global battery supply chain, and it applies to Kenitra as much as to any other non-Chinese cell manufacturing facility.

The DRC Cobalt Question — And Why It Is Partly Obsolete

The Democratic Republic of Congo supplies approximately 70 percent of the world’s mined cobalt — a position of extraordinary strategic importance in the conventional battery narrative. The DRC cobalt question seems obvious: does Kenitra change anything for Congolese mining communities and government revenues?

The answer is complicated by a chemistry shift that has been underway for several years. LFP batteries — the architecture Gotion uses in Kenitra — contain no cobalt at all. LFP’s cathode chemistry is lithium, iron, and phosphate. The cobalt-intensive architectures are NMC (nickel-manganese-cobalt) and NCA (nickel-cobalt-aluminium), used primarily in premium EV segments and some energy storage applications. As LFP has gained market share globally — its lower cost and longer cycle life make it the dominant choice for mass-market EVs and stationary storage — cobalt demand growth has slowed.

The real risk for the DRC is not that Kenitra uses its cobalt, but that the global EV industry is structurally de-cobaltifying. If LFP continues to displace NMC in mainstream EV applications, the cobalt-dependent assumption behind Congolese mining revenues faces a secular challenge that no individual factory decision changes. The DRC’s strategic imperative is to diversify its minerals processing ambitions beyond cobalt — into copper, which LFP and all other battery chemistries still require in large quantities, and into battery-grade manganese, which next-generation LMFP (lithium manganese iron phosphate) architectures will need at scale.

Why Morocco Won — And It Was Not the Minerals

Understanding why Kenitra happened in Morocco rather than in Zimbabwe, Zambia, or the DRC requires confronting the actual investment decision criteria. The minerals contribution was secondary. The primary factors were structural.

Morocco has an EU Association Agreement that grants Moroccan-manufactured goods tariff-free access to European markets. For a battery manufacturer whose primary customers are European automotive groups, this is an existential trade advantage — especially as the EU’s Carbon Border Adjustment Mechanism and battery regulation framework tighten rules of origin requirements. A battery cell made in Morocco and shipped to Renault’s French factories arrives without tariffs and with EU regulatory compliance built in. A cell made in Zimbabwe faces a different calculation entirely.

Morocco has an existing automotive manufacturing cluster in Tangier and Kenitra — Renault and Stellantis already produce vehicles there. The customer base for Gotion’s battery output is, in part, literally adjacent. Morocco has grid reliability, logistics infrastructure, a trained industrial workforce, and an investment-grade sovereign credit rating. It has a government with the institutional capacity and financial tools to structure the incentive package Gotion required. These are not soft factors — they are the conditions that make a $5.6 billion irreversible capital commitment possible.

Zimbabwe has the lithium. The DRC has the cobalt. Zambia has the copper. None of them, in 2025, had the combination of trade access, customer proximity, grid stability, industrial cluster, and sovereign investment environment that Morocco assembled. The minerals were neither sufficient nor the deciding factor.

What It Would Take — And Whether the Window Is Still Open

The uncomfortable implication for Harare, Kinshasa, and Lusaka is that the path to capturing battery manufacturing value is not primarily about minerals endowment. It requires building the enabling conditions that Morocco built, in sectors and at investment scales where the continent has not traditionally succeeded.

Zimbabwe’s lithium export ban is a partial first step — it attempts to move up one tier from raw ore to concentrate. But the refining and cell manufacturing tiers require sustained industrial policy, reliable electricity (Zimbabwe currently has severe grid deficits), logistics, and a creditworthy investment environment that can attract anchor tenants. Zambia’s copper processing ambitions face similar constraints: the ore is there, but the smelter and refinery capacity is inadequate, grid supply is intermittent, and the policy environment has historically deterred the scale of foreign investment required.

The DRC faces the most complex challenge. A country with the world’s largest cobalt reserves and significant lithium potential has virtually no domestic battery processing capacity, chronic grid deficits, and infrastructure gaps that represent decades of underinvestment. The AfDB and other multilateral lenders have flagged DRC battery minerals processing as a priority — but flagging and financing are different things.

The window is not permanently closed. The global battery supply chain is still being built. Second and third gigafactory waves across Africa are possible. Morocco has demonstrated that the enabling conditions can be assembled on the continent. But the decisions in Kinshasa, Harare, and Lusaka that would make their minerals endowment translate into manufacturing presence need to happen now — before the supply chains lock in, before the trade frameworks calcify, before the Chinese processing and European assembly relationships become the only model anyone can imagine.

The Kenitra gigafactory is a real milestone. Africa’s first battery cell plant is not nothing — it is proof that large-scale battery manufacturing investment is possible on the continent, that an African government can structure an anchor industrial deal, and that the continent’s clean energy supply chain role can be more than extraction. The question is whether it remains an isolated achievement or becomes the first node in a genuinely continental battery economy.

That answer will not be determined in Morocco. It will be determined in the mineral-rich countries that have not yet built what Morocco built — and whether they move before the opportunity passes.