Africa’s beauty and personal care market is on track to reach $66.19 billion in 2024 — a figure most business coverage ignores because the industry is framed as culture rather than commerce. Behind the product launches, YouTube tutorials, and salon visits sits a commercially significant sector shaped by import dependency, digital monetisation constraints, and a thin layer of locally-owned brands operating against multinational incumbents that control the majority of retail revenue.

This is the economics of African beauty.

The Market: Scale, Structure, and Who Controls It

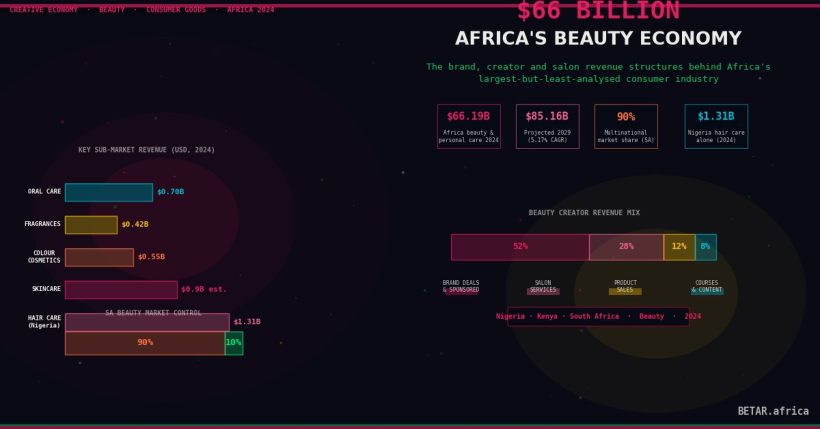

Africa’s beauty and personal care market — encompassing hair care, skincare, colour cosmetics, fragrances, and oral and personal hygiene products — was projected at $66.19 billion in 2024, growing to $85.16 billion by 2029 at a compound annual growth rate of 5.17% (Statista). A narrower cosmetics-only estimate from Market Data Forecast puts Africa’s cosmetics segment at $3.87 billion in 2024, forecast to reach $7.02 billion by 2033.

The control question is stark. In South Africa — the continent’s most sophisticated beauty retail market — multinational companies account for approximately 90% of personal care sales, with Unilever, Procter & Gamble, L’Oréal, and Revlon dominating formal retail (InvestSA consumer goods data). Indigenous brands compete primarily at the affordable end of the market or through direct-to-consumer channels.

Nigeria’s hair care sub-market alone is valued at $1.31 billion in 2024, projected to reach $1.96 billion by 2028 — a CAGR of approximately 10.6% (Statista). But Euromonitor’s analysis flags a critical caveat: the value increase is substantially driven by unit price inflation exceeding 60% in 2024, caused by naira depreciation making imported inputs more expensive. Volume demand declined as consumer spending power fell. A market that appears to be growing may be contracting in real terms.

African Beauty Brands: The Export Exception

The best-known African-founded brand to achieve documented commercial scale is Juvia’s Place, founded by Chichi Eburu — born in Nigeria, launched in the United States in 2016 with an initial $2,000 investment. Third-party revenue estimates place it at approximately $6 million annually (Owler/ZoomInfo, 2025), distributed through Ulta Beauty and direct-to-consumer channels in the US, Europe, and the UAE. Structurally, it is a US brand with Nigerian creative DNA — it captures export revenue, not African domestic market revenue.

Zaron Cosmetics, founded in Lagos, operates differently: 30-plus franchise locations across Nigeria, Ghana, Kenya, Uganda, Zimbabwe, Sierra Leone, Ivory Coast, and Cameroon, with over 1,000 distributors across African markets. Zaron is a genuine continental distribution play. No public revenue figures are available.

The clearest case study for the economics of building and exiting an African beauty manufacturing business is Interconsumer Products (ICP) in Kenya. Founded in 1995 by Paul Kinuthia, ICP grew to approximately Ksh1.7 billion (~$13 million) in annual revenue with around Ksh200 million in net profit at its peak. In 2013, L’Oréal acquired ICP’s health and beauty division for approximately Ksh1.5 billion (~$11–17 million), retaining the Nairobi plant as its regional production hub for East Africa. ICP’s story illustrates both what is achievable and the acquisition trajectory that often ends it.

Import Dependency: The Manufacturing Gap

Approximately 80% of raw materials used by African cosmetics manufacturers are imported — ingredients and packaging components alike — meaning even local manufacturers are structurally dependent on imported inputs (BeautyMatter; Beauty Africa). South Africa imported $56.9 million in US cosmetics alone in 2023 (US Trade Representative, March 2024).

Import duty economics compound the cost. Nigeria operates under the ECOWAS Common External Tariff with cosmetics attracting 20% under CET Band 4, with additional levies potentially raising effective rates further. South Africa levies 15% VAT on cosmetics imports on top of product-specific tariff rates. For consumers, this passes through entirely at the shelf price.

The extensions and weave supply chain illustrates where margin concentrates. Human hair extensions originate almost entirely from manufacturers in China, Vietnam, and India — wholesale pricing typically runs $30–80 at factory gate. The importer/wholesaler layer in Africa captures the dominant margin, adding freight, customs duties (typically 20–30% in most African markets), and their own markup before reaching salon or retail distribution. South Africa’s extensions market is estimated at $149 million by 2028 (Fortune Business Insights).

Creator Monetisation: The CPM Compression

Africa’s beauty creator economy operates under structural monetisation constraints that directly affect the economics of running a content-first beauty business.

YouTube advertiser-side CPM rates in Nigeria average approximately $2.50 per thousand views; creator RPM (after YouTube’s 45% cut) typically falls between $0.50 and $1.50. South Africa CPMs are structurally higher — around $10 advertiser-side — but largely because South African creators attract significant viewership from higher-CPM markets. Creators with predominantly domestic African audiences earn at Nigerian-range rates regardless of geography.

The mitigation is brand partnerships: globally, 60–80% of beauty creator income comes from brand deals, with AdSense contributing only 20–40%. A 100,000-view video generates approximately $300–500 in ad revenue but $3,000–15,000 with a brand integration at market rates. In Africa, the constraint is that local beauty brand marketing budgets are significantly smaller than global equivalents — meaning even well-followed African creators may be dependent on deals from multinationals with selective Africa-focused allocations, rather than a competitive local brand-deal market.

Meta launched in-stream ads, Instagram Gifts, and Facebook Stars in Nigeria and Kenya from June 2024 — expanding monetisation pathways beyond YouTube AdSense for the first time in those markets, though the underlying CPM economics remain unchanged.

Salon Tech: Global Platforms, Local Gaps

The salon booking technology market in Africa is being served by global platforms. Booksy — $65.9 million in global revenue in 2024, serving 140,000+ businesses across 25 countries — is present in South Africa. Fresha, the sector’s fastest-growing platform at $43.4 million in global revenue in 2024, operates on a free core model with monetisation through payment processing and premium features (GetLatka, 2024). Approximately 6,800 South African salons use digital scheduling platforms. The informal salon economy — the majority of hair services revenue across West and East Africa — remains largely outside digital booking infrastructure.

The real commercial opportunity is not booking: it is B2B beauty supply aggregation. Most African salon owners procure supplies through fragmented wholesale and distributor networks. A platform that aggregated supply procurement could capture margin currently distributed across the importer-wholesaler tier — but no Africa-native platform with documented commercial scale in this space has emerged.

The Structural Tension

Africa’s beauty economy has a fundamental structure problem: the continent is a consumption market, not yet a production market, for the commercial products that define the sector. Multinationals collect the majority of formal retail revenue. Raw materials for local manufacturers are imported. Extensions are manufactured in Asia. The platforms mediating salon commerce are built in the US and Europe.

The exceptions — Juvia’s Place as a creative export, Zaron as a continental distribution network, ICP as a manufacturing operation that reached scale before acquisition — demonstrate that the structure is not deterministic. But closing the manufacturing gap requires capital at a scale that venture investment in African beauty startups has not yet provided.

At $66 billion in total market size and growing, Africa’s beauty sector is commercially material. The question is which economic actors will capture an increasing share of its value chain.

Sources: Statista Africa Beauty & Personal Care Outlook 2024; Euromonitor Nigeria Hair Care Report 2024; Market Data Forecast Africa Cosmetics Market 2024; InvestSA Consumer Goods Sector Factsheet; US Trade Representative Cosmetics Resource Guide March 2024; Owler/ZoomInfo Juvia’s Place revenue estimate 2025; L’Oréal Finance ICP acquisition filing 2013; Fortune Business Insights Hair Extension Market Report; BeautyMatter Africa Manufacturing Analysis; GetLatka Fresha revenue data 2024; Booksy company data.