Ghana’s 5G Reset: How the NGIC Experiment Failed and What Comes Next

By BETAR Technology Reporter | Accra, 14 March 2026

On the morning of 4 March 2026, Next-Gen InfraCo (NGIC) held a press event in Accra to announce it had finally switched on Ghana’s 5G backbone — a milestone the company had promised for years. By that same afternoon, the National Communications Authority (NCA) had published a formal Notice of Proposed Licence Amendment that will strip NGIC of the exclusivity clause at the heart of its business model.

The timing was deliberate. Ghana’s regulator had run out of patience.

After more than three years of deployment delays and licence fee defaults, the NCA issued the amendment notice pursuant to Section 14 of Ghana’s Electronic Communications Act, 2008 (Act 775), proposing to remove NGIC’s exclusive right to deploy and operate a shared 5G infrastructure. The notice gives the company 90 days to make representations before the change takes effect.

“The Authority considers this action to be in the public interest,” the NCA stated, “with the objective of promoting competition and innovation in the provision of 5G services and ensuring optimal and efficient use of spectrum as a national resource.”

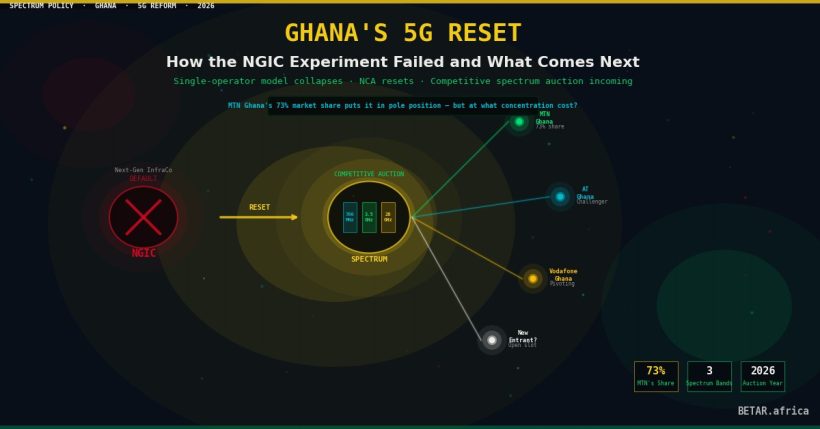

The regulatory reset signals the end of an ambitious experiment in shared infrastructure — and opens a competitive auction that could reshape Ghana’s telecoms market well before the country’s 70th Independence Day in March 2027.

The Shared Model That Stalled

Ghana’s original 5G strategy broke from the global playbook. Rather than auctioning spectrum to competing operators, Accra set up NGIC as a single wholesale network operator that would build shared infrastructure and sell access to the market’s mobile network operators. The model was designed to avoid the duplicated capital expenditure seen in more fragmented markets and to ensure coverage reached beyond profitable urban corridors.

On paper, the logic was sound. In practice, it collapsed under the weight of NGIC’s financial difficulties. The company has paid only $6 million of its total licence fee obligations, with a further $6 million agreed in principle but currently subject to a restructuring request — leaving Ghana’s 5G rollout tied to a single operator whose balance sheet was already stretched before commercial launch.

Industry analysts had flagged the structural risk for months. “Ghana chose not to auction spectrum in the conventional sense,” one telecoms analyst noted at the time of NGIC’s original appointment. “The question was always whether one entity could mobilise the capital required at the pace the government expected.”

The answer, it turns out, was no.

The Dual-Track Pivot

Communications Minister Samuel Nartey George announced the policy shift in late February 2026, telling industry stakeholders that the government would make frequency resources available through a competitive national tender. Cabinet has since signed off on the plan, with the auction expected to commence within weeks following Mobile World Congress in Barcelona, where Ghana’s spectrum plans drew significant international attention.

The new model is not a wholesale abandonment of NGIC. The NCA’s amendment retains NGIC’s wholesale licence — the company can still sell shared infrastructure access to operators. But it can no longer function as the sole gateway to 5G in Ghana. Individual operators will be free to acquire spectrum independently, deploy their own networks, and compete with NGIC’s wholesale product on price and coverage.

The government has attached a hard deadline: 70 percent population coverage by March 2027, tied to the symbolic significance of Ghana’s Independence Day jubilee. The NCA insists on a coordinated launch date so that no single operator can roll out 5G ahead of others — a condition designed to prevent a first-mover lock-in that could entrench existing market asymmetries.

Whether Ghana can move from contested exclusivity clause to functional 5G networks at scale in twelve months is an open question that analysts are watching closely. The country has historically struggled to deliver spectrum on schedule: the network NGIC nominally “launched” in November 2024 still had not enabled commercial MNO 5G services by early 2026.

MTN’s First-Mover Arithmetic

Whoever writes the competitive auction rules, one operator stands to benefit disproportionately from market opening: MTN Ghana.

With a 73.25 percent share of Ghana’s mobile subscriber base as of Q3 2025 — against Telecel Ghana at 19.25 percent and AT Ghana at 7.5 percent — MTN is not just the market leader; it operates in a different commercial orbit from its nearest rival. It already has more than 5,000 telecom sites nationwide, and has committed to deploying at least 500 additional sites in 2026 alone, a tenfold acceleration from the roughly 50 sites it added in the prior year. The company’s three-year capital programme is budgeted at $1.1 billion.

MTN Ghana has been in active discussions with the Ministry of Communications about acquiring both 700 MHz and 3,500 MHz spectrum. The combination matters. The 700 MHz band — so-called “sub-1GHz” spectrum — travels farther and penetrates buildings more effectively, ideal for broad coverage and rural reach. Paired with 3,500 MHz for capacity, the blend enables Fixed Wireless Access (FWA): 5G broadband delivered directly to homes and businesses via rooftop receivers, bypassing the need for fibre cabling in areas where it remains uneconomical to lay.

For MTN Ghana, FWA is not a secondary use case — it is a core revenue strategy that would extend its dominance in mobile into the fixed broadband segment that Ghana’s relatively thin fibre infrastructure has left largely uncontested.

Telecel Ghana has called for transparent and competitive allocation of spectrum to prevent the auction from simply rubber-stamping MTN’s structural advantage. “Competition works when the rules are designed to enable it,” a Telecel representative said, without specifying whether the company would seek the same spectrum combination as its larger rival.

What Happens to NGIC?

NGIC’s fate under the new model is the question that industry observers are watching most closely. Having launched its backbone network — somewhat defiantly, on the same day the NCA moved to strip its exclusivity — the company now faces a harder commercial reality. Its value proposition was built on being the only route to 5G in Ghana. That moat is gone.

What remains is a wholesale infrastructure network competing in a market where operators with their own spectrum will have little incentive to pay for shared access. NGIC’s survival will depend on whether it can offer price, coverage, or speed advantages over what operators can build independently — and whether its financial restructuring allows it to invest in the network quality necessary to make that case.

The outcome matters beyond NGIC’s shareholders. If the wholesale model fails commercially, it will discourage future shared-infrastructure experiments across a continent where duplicated capital expenditure is one of the primary reasons rural connectivity has lagged urban coverage by years. Ghana set a precedent by trying the shared-infrastructure route first; how it exits that model will set a different kind of precedent.

A Regional Signal

Ghana’s 5G auction sits inside a broader pattern of African spectrum market activity. South Africa’s ICASA is running a parallel auction process for additional mobile broadband spectrum in 2026–27 (BETA-522), while Nigeria’s investment in hyperscale data centre capacity has accelerated demand for the fibre and spectrum backhaul that underpins any 5G rollout (BETA-509). Across both markets, the lesson is consistent: single-operator or single-vendor models carry concentration risk that competitive pressure eventually forces open.

For the analysts tracking African telecoms investment, the more significant signal in Ghana’s pivot is not the revocation of NGIC’s exclusivity — that outcome was widely expected once the licence fee default became public. It is the speed with which the government moved to salvage a credible 5G timeline by designing a market rather than waiting for NGIC to fix its balance sheet.

The March 2027 deadline is ambitious by any standard. Whether Ghana’s new dual-track model produces a 5G market that reaches 70 percent of the population in twelve months — or whether it produces a protracted auction dispute that delays deployment further — is the story that will define whether this regulatory reset delivered on its promise.

The spectrum clock is running.

BETAR covers the African technology and business ecosystem. Related coverage: South Africa’s ICASA spectrum auction process and Nigeria’s data centre investment wave.