Nigeria After FATF: Can Africa’s Biggest Fintech Market Now Set the Rules?

The grey-list removal unlocked a capital flows argument. The CBN moved fast. Now comes the harder question: does processing 11 billion transactions give Nigeria the regulatory standing to set continental standards — or does that require something more?

On October 24, 2025, the Financial Action Task Force removed Nigeria from its grey list after the country completed a 19-point reform program, achieving Compliant or Largely Compliant status on 37 of 40 FATF recommendations. The European Commission followed the same day, removing Nigeria from its high-risk third-countries list. The combined signal was unambiguous: Nigeria’s financial system had met the international community’s baseline standards for anti-money laundering and counter-terrorism financing controls.

The IMF had estimated that grey-listing reduced Nigeria’s capital inflows by approximately 7.6 percent of GDP — a significant drag on a market of 220 million people with one of Africa’s deepest financial ecosystems. Removal from the grey list did not automatically reverse those flows, but it removed the formal barrier. For Nigerian fintechs that had been navigating due diligence friction with European and American institutional investors for two years, the signal mattered.

The CBN’s response to the removal was not to pause. It accelerated.

The Regulatory Cascade That Followed

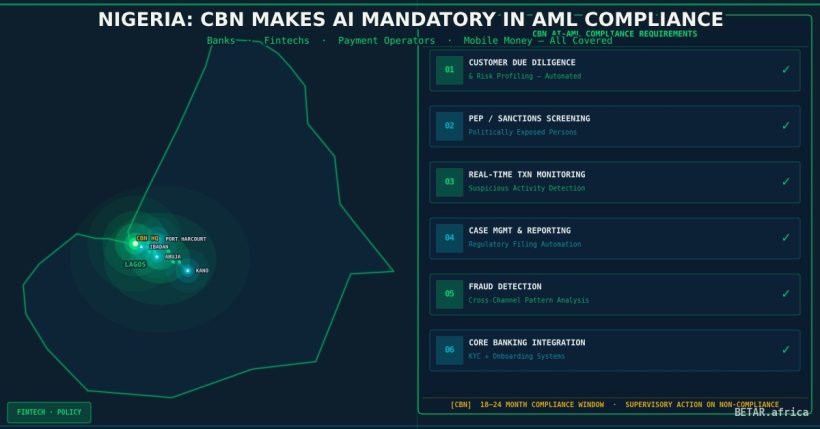

In the four months since FATF removal, the Central Bank of Nigeria has issued three significant fintech security directives in rapid sequence. Mandatory biometric liveness verification for all new account openings took effect in January 2026, requiring banks and fintechs to tie account creation to a biometric record rather than a phone number alone. In February, the CBN published its AI AML Baseline Standards — the first African central bank framework requiring machine learning-based transaction monitoring as a compliance obligation, not merely a best-practice recommendation. In March, it restricted BVN-linked phone number changes to once per lifetime, effective May 1, closing a SIM-swap fraud window that had enabled an estimated 62,000 fraud incidents in 2023 alone.

None of these are incremental tweaks. Taken together, they represent a deliberate architectural shift: the CBN is moving Nigeria’s fintech compliance stack from reactive fraud-reporting toward real-time identity-to-behaviour assurance — catching fraud at account creation (liveness), at the network layer (the TIRMS SIM recycling database), and in transaction flow (AI AML monitoring). The February 2026 CBN Fintech Policy Insight Report named this ambition explicitly: Shared Fraud Defence Framework, Fintech Trust and Safety Charter, HAWK (a central industry fraud intelligence desk), Project Stallion (a cyber operations centre), and BVN Watchlisting.

The CBN’s stated goal is not just better domestic compliance. It is continental standard-setting.

The Credibility Question

Nigeria’s transaction volume argument is substantial. NIBSS processed approximately 11 billion transactions in 2024 — a figure that reflects the scale of a payments ecosystem anchored by Opay’s estimated 40 million users, Flutterwave’s regional infrastructure position, and Moniepoint’s merchant network. By transaction volume, Nigeria is not just Africa’s largest fintech market. It is not obviously close.

But volume and regulatory standing are not the same thing. South Africa’s Financial Intelligence Centre and Financial Sector Conduct Authority have built compliance architecture over decades, underpinned by the country’s Basel III alignment and deep capital market linkages to London and New York. Kenya’s Central Bank has pioneered mobile money regulation through M-Pesa’s evolution and published some of the continent’s most detailed digital credit frameworks. Ghana’s Bank of Ghana has pursued a deliberate and incremental virtual asset licensing regime that has earned international credibility as a proportionate response to emerging risks.

Each of these frameworks rests on a different foundation. South Africa’s authority derives from institutional depth and capital market integration. Kenya’s from first-mover mobile money governance. Ghana’s from regulatory proportionality. Nigeria’s claim — if it is to be made — rests on a different proposition: that systemic scale, combined with the compliance architecture being built now, creates an obligation to lead because the risks are largest where the volume is highest.

That argument has precedent. The United States Federal Reserve’s influence over global banking regulation was not derived from philosophical authority. It was derived from the fact that the dollar underpins international trade and the consequences of American banking failure are global. Nigeria is not the dollar. But in African fintech, the network effects of scale are beginning to produce analogous dynamics: what Nigeria mandates for AML, its fintech partners across the continent must accommodate if they want access to Nigerian payment rails.

What Capital Flows Actually Tell Fintechs

The 7.6 percent of GDP figure is a macro argument. The fintech experience of grey-listing was more granular and more corrosive. Enhanced due diligence requirements imposed by European and American institutional investors added months to fundraising timelines, required additional compliance documentation that smaller fintechs lacked the legal bandwidth to produce, and in several cases led to deal structures that reduced founder economics in exchange for investor risk mitigation.

Removal from the grey list does not automatically eliminate enhanced due diligence for every counterparty. Institutional compliance policies lag the FATF registry by months. Correspondent banking relationships — in which Nigerian banks rely on US or European banks to clear dollar transactions — carry their own ongoing compliance thresholds. The grey-list removal removed the formal basis for enhanced scrutiny; it did not immediately change the institutional muscle memory of four years of treating Nigerian counterparties as elevated-risk.

What the removal signals to the next tier of investors — growth equity funds and strategic investors evaluating Nigeria’s fintech infrastructure now — is that the floor has been credibly established. The regulatory architecture being built by the CBN in 2026 is the evidence that the floor holds.

The question for a Series B fintech in Lagos, or a pan-African payment processor evaluating whether to build on Nigerian rails, is whether the CBN’s compliance cascade creates more friction than it resolves. Biometric liveness verification requires integration with NIBSS-connected identity infrastructure. AI AML monitoring requires ML engineering capacity that tier-two fintechs and microfinance banks may need to procure from third-party vendors. BVN phone lock creates user experience friction at the edge — particularly for the 68.59 million BVN holders who are already underserved by digital financial services and cannot easily navigate remediation processes if locked out.

The CBN’s architecture is coherent as a fraud prevention strategy. Whether it is also coherent as a financial inclusion strategy is a question the February 2026 Fintech Policy Insight Report does not fully answer.

Can Nigeria Set the Rules?

The continental regulatory standards conversation is moving faster than most observers anticipated. The African Union’s Continental AI Strategy and the Africa AI Council’s emerging framework for responsible AI in financial services are both in formation. Nigeria’s NITDA has published Africa’s most detailed AI risk-tier framework. The CBN has published its AI AML Baseline Standards before any other African central bank. South Africa’s FSCA and Kenya’s CBK are watching.

Continental regulatory standard-setting in financial services does not happen through declaration. It happens through precedent: one regulator sets a requirement, other regulators watch how it lands, and the successful ones get adopted — or adapted — by their peers. The CBN’s liveness checks requirement, the AI AML standards, and the HAWK fraud intelligence desk are all potential precedents.

What Nigeria cannot yet claim is the full package: scale plus architecture plus institutional credibility with international standard-setting bodies, plus demonstrated enforcement track record. The FATF removal addressed the compliance architecture argument. The 2026 regulatory cascade is building the institutional credibility argument. Enforcement track record takes longer.

Nigeria after FATF is not yet Nigeria as Africa’s regulatory standard-setter. It is Nigeria making the credible case that it could be — on a timeline that is shorter than most of its competitors have assumed.

— Technology Desk, BETAR.africa