The problem with Africa’s climate finance conversation is that it is almost entirely about the wrong end of the pipeline. The billions announced at COP negotiations, the sovereign green bonds, the blended finance vehicles — these instruments reach companies that have already proven their technology, built revenue, and navigated regulatory frameworks. The founders who have none of those things get almost nothing.

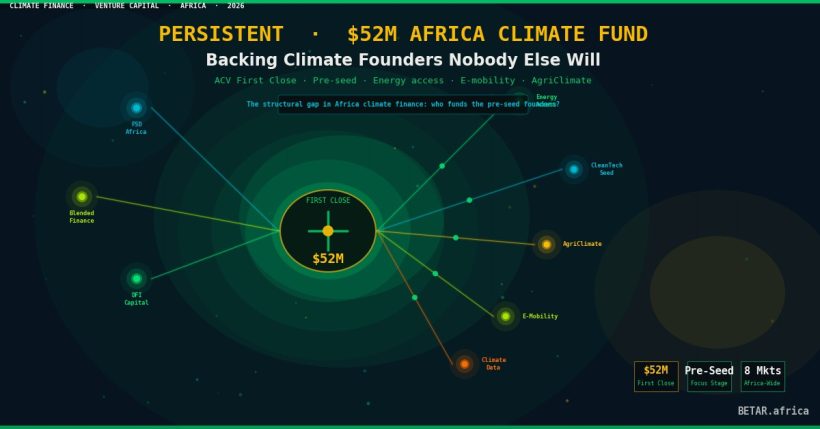

Persistent, a Nairobi-based climate venture builder with more than a decade of pre-fund operating history, has spent fourteen years working in the gap those instruments ignore. And on March 11, 2026, it announced a $52 million first close for its Africa Climate Venture (ACV) Fund — the institutional formalisation of a thesis that has backed twenty-three companies across twenty-two African countries since the organisation’s founding as a spinout from the pioneering clean-energy finance firm E+Co in 2012.

The fund’s target is $70 million. A first close at 74 percent of target is comfortably within the normal range for a fund of this profile — most institutional GPs expect to reach 60–80 percent of target at first close, with the remaining capital secured in the six to twelve months that follow. Persistent has indicated it expects a final close in the second half of 2026.

Why Pre-Seed Climate Is Structurally Unfunded

Less than three percent of climate finance reaching Africa lands at the pre-seed and seed stage, according to the Climate Policy Initiative’s 2025 Global Landscape of Climate Finance. The remainder flows to infrastructure-scale transactions, sovereign instruments, and growth-stage companies with proven revenue. The reasons are structural rather than ideological.

Early-stage climate hardware companies — solar mini-grid operators, clean cookstove manufacturers, climate-smart agritech startups — carry risk profiles that institutional capital is poorly equipped to price. Revenue timelines are long. Hardware costs require capital expenditure before a single unit ships. Regulatory frameworks for energy tariffs and grid interconnection are uncertain. Returns depend on market development work that is expensive and slow. Most venture capital funds — including Africa-focused climate funds — have opted for the easier path: entry at growth stage, where the technology works, the customer exists, and the exit timeline is shorter.

“The structural gap at the earliest stage of Africa’s climate startup ecosystem is where we have always operated,” said Tobias Ruckstuhl, Persistent’s Managing Partner, at the fund’s first close announcement. “The ACV Fund is our ability to do that at institutional scale — bringing in the LP capital that matches the patient, hands-on model we have built over more than a decade.”

The ACV Fund’s mandate reflects that history. It writes cheques of $250,000 to $1 million — smaller than virtually every Africa-focused climate fund currently operating — targeting seed and pre-seed companies in energy access, sustainable agriculture, water, waste, and e-mobility. These are sectors where a founding team can raise $500,000 and genuinely move the needle on product development, but where that $500,000 is almost impossible to source from the standard Africa VC playbook.

The LP Roster as a Signal

The investor composition of the ACV Fund is itself a story. FSD Africa Investments — the investing arm of FSD Africa, financed by the UK’s Foreign, Commonwealth & Development Office — serves as anchor LP. Nordic Development Fund, the Japan International Cooperation Agency (JICA), AfDB’s SEFA facility, FMO, the Soros Economic Development Fund (with a $7 million commitment), Impact Fund Denmark, and the Schmidt Family Foundation round out the first-close roster.

The presence of JICA alongside FSD Africa and Nordic Development Fund reflects a broadening of the DFI coalition around early-stage Africa climate. These are not impact-adjacent commercial funds making climate allocations. They are development finance institutions whose mandates are explicitly designed for patient, concessional-adjacent capital — the precise profile that pre-seed climate hardware requires.

“Persistent’s model — combining early-stage equity with dedicated venture-building services — addresses the gap that purely financial instruments cannot close,” said Catherine Kariuki, Head of Investment at FSD Africa Investments. “Founders in the climate space need more than capital at this stage. They need technical support, market development expertise, and regulatory navigation. Our anchor commitment reflects confidence in that integrated approach.”

The $7 million Soros commitment through the Soros Economic Development Fund, the investment vehicle of the Open Society Foundations, adds a dimension that pure DFI capital lacks: a commercially-minded, impact-oriented LP whose participation signals that the fund’s return profile is credible beyond concessional finance.

The Venture Building Facility: A Separate Instrument

Alongside the $70 million ACV Fund, Persistent has structured a $5 million Venture Building Facility as a legally distinct vehicle. The distinction matters for readers tracking how capital is structured in this space.

The Venture Building Facility does not make equity investments. It provides services — technical assistance, business development, regulatory navigation, and market access support — to early-stage climate companies, including companies that Persistent has not yet invested in. This means a founder in the Persistent ecosystem can access hands-on operational support even before any equity transaction takes place. The Facility is funded separately from the ACV Fund, with its own LP base, and is structured to be deployed as grant-equivalent or near-grant support rather than return-generating capital.

The separation is deliberate. Mixing technical assistance with investment capital creates conflicts of interest: a fund that charges portfolio companies for services it provides has an incentive to over-service, while a combined structure obscures whether returns are driven by investment selection or service fees. Persistent’s decision to ring-fence the facility reflects the institutional maturity of the overall structure.

What the Model Looks Like in Practice

Persistent’s track record before the ACV Fund illustrates how the thesis plays out. Among its portfolio companies is Burn Manufacturing, the Kenyan clean cookstove producer that has become one of the largest manufacturers of improved cookstoves in Africa — a company that received early-stage support from Persistent’s predecessor vehicles before reaching commercial scale. The arc from early catalytic support to commercial scale is exactly the trajectory the ACV Fund is designed to replicate at greater frequency and with more structured capital behind it.

The portfolio approach creates a network effect that individual investments cannot. ACV Fund portfolio companies share procurement pipelines, market access relationships, and regulatory expertise developed across Persistent’s twenty-two-country operating footprint. A solar mini-grid startup in Zambia and a climate-smart agritech company in Ghana both benefit from the same relationships with off-takers, grid operators, and government procurement systems that Persistent has built over fourteen years. For a $500,000 pre-seed company, that network is worth more than the cheque.

Reading This Against Africa’s Broader VC Shift

The ACV Fund’s first close arrives at a moment when Africa’s venture capital ecosystem is reconfiguring in ways that make Persistent’s positioning more relevant, not less. As BETAR’s analysis of the Africa Series A drought and the rise of local VC documented, US-based venture capital participation in African deals fell by 53 percent between early 2025 and early 2026. The gap is being filled by African institutional capital — development finance institutions, government-linked funds, and Africa-native VCs with patient mandates.

The climate sector is experiencing the same dynamic with additional intensity. Global commercial climate funds that entered Africa at growth stage are finding exit conditions difficult. Hardware companies with 8–12 year return timelines do not fit the standard VC fund life cycle. The retreat of commercially-oriented global capital from early-stage Africa climate is not a temporary cycle — it is a structural feature that development-oriented capital models like Persistent’s are best positioned to serve.

The ACV Fund’s LP base reflects this reality exactly. It is not built around commercial fund-of-funds or institutional endowments seeking Africa beta. It is built around patient, mission-aligned capital that can hold a $250,000 seed cheque for eight years and call that a successful deployment if the portfolio company is still standing, growing, and providing energy access to underserved communities.

The Funding Gap That Remains

At $52 million first close toward a $70 million target, the ACV Fund is a meaningful intervention. It is not a solution to the structural financing gap it is designed to address.

The International Energy Agency estimates that achieving universal electricity access in Sub-Saharan Africa by 2030 requires approximately $25 billion in annual investment — the vast majority of it in the distributed, off-grid, and mini-grid infrastructure that pre-seed companies like those in Persistent’s pipeline are building. A $70 million fund deploying $250,000–$1 million cheques can seed dozens of companies. It cannot capitalise an ecosystem.

What it can do — and what Persistent’s fourteen-year track record suggests it does well — is prove the model. The ACV Fund’s first close with FCDO, JICA, and Soros as co-investors sends a signal to other institutional LPs that the pre-seed Africa climate thesis is credible, structured, and capable of attracting serious capital. If the fund performs and reaches final close as expected in late 2026, the next Persistent vehicle will likely be larger, and the cohort of GPs willing to operate at this stage will be wider.

That is how an ecosystem is built: not in one announcement, but in successive proof points that expand the frontier of what institutional capital believes is possible.

BETAR.africa covers Africa’s technology, business, and innovation economy. This article draws on Persistent’s first close announcement (March 11, 2026), FSD Africa Investments commentary, Climate Policy Initiative Global Landscape of Climate Finance 2025, and IEA Africa Energy Outlook 2025. Burn Manufacturing is cited as a historic example from Persistent’s portfolio of predecessor vehicles; inclusion does not imply current ACV Fund portfolio status.