For three weeks in May 2024, internet performance across seven East African countries collapsed. A ship anchor dragged across the seabed off KwaZulu-Natal had severed the SEACOM and EASSy cables simultaneously. The outage revealed something East Africa’s digital economy had quietly avoided examining: who actually owns the infrastructure on which it runs. The answer, increasingly, includes the Gulf.

The New Landlords

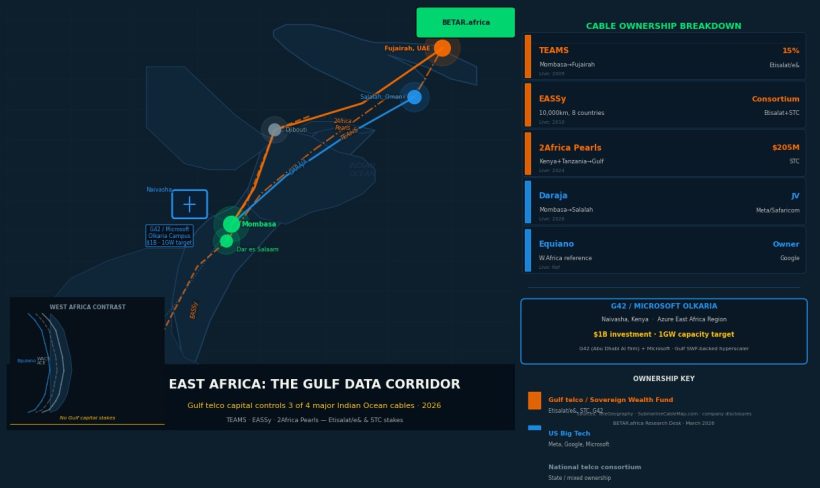

In May 2024, Abu Dhabi AI conglomerate G42 and Microsoft announced a $1 billion “comprehensive digital ecosystem initiative” for Kenya. At its core: a geothermal-powered hyperscale data centre campus at Olkaria, Kenya’s volcanic fields in Naivasha, built through a joint venture between G42 and Kenyan firm EcoCloud. Phase one alone costs $600 million. The eventual buildout target is 1 gigawatt of capacity, making it among the largest planned data centre investments on the continent. It will serve as Microsoft’s East Africa Azure Cloud Region, covering Kenya, Uganda, Rwanda, and Tanzania.

The Olkaria campus is the most visible Gulf capital entry into East Africa’s digital infrastructure — but it is not the oldest. The TEAMS (East African Marine System) cable, which connects Mombasa to Fujairah in the UAE, has carried a 15% stake held by Etisalat (now e&) since the cable launched in 2009. The Kenyan government holds 20%; Telkom Kenya 23%. The cable is both a connectivity asset and a structural dependency: Mombasa is physically tethered to a UAE-owned landing point.

Both Etisalat and Saudi Telecom (STC) hold consortium membership in EASSy, the 10,000-kilometre backbone cable that stitches together eight East African coastal countries from Sudan to South Africa. Gulf operators hold capacity stakes, not operating control — but the distinction matters less when a cable goes down.

The newest link in the Gulf-East Africa cable chain is the 2Africa Pearls system. STC contributed $205 million to the Gulf extension of Meta’s 2Africa cable, which lands in Kenya and Tanzania and is expected to come fully online in 2026. And in October 2025, Meta and Safaricom announced the Daraja cable: a 4,108-kilometre direct link between Mombasa and Salalah, Oman — the first fibre connection to physically bridge the East African coast to the Arabian Peninsula.

Daraja is technically Meta-owned, with Oman as the landing destination rather than a co-investor. But the direction of travel is unmistakable. East Africa is becoming the Indian Ocean terminus of a Gulf digital corridor.

The Sovereignty Gap Nobody Talks About

East Africa’s data protection laws have moved fast. Kenya’s Data Protection Act (2019) requires that at least one serving copy of personal data be stored on a server physically located in Kenya. Tanzania’s Personal Data Protection Act (2022) and Ethiopia’s Personal Data Protection Proclamation (2024) contain comparable domestic storage requirements. Rwanda has embedded data residency expectations in sector regulation since at least 2017, when it compelled MTN to relocate its data centre from Uganda.

None of these laws prohibit foreign ownership of the infrastructure that stores that data.

This is the structural gap. A Gulf sovereign wealth fund can own the data centre, comply fully with Kenya’s Data Protection Act, and still retain operational control over the physical hardware — the cooling systems, the network interfaces, the uptime decisions. Data residency (where the bits are stored) and infrastructure sovereignty (who owns what the bits run on) are treated, across the region’s legal frameworks, as entirely separate questions.

“The issue is not just where data lives but who controls the conditions under which it is accessible,” the Internet Society warned in its 2025 policy brief on submarine infrastructure resilience. The May 2024 outage made the physical version of this argument vividly. The Carnegie Endowment’s Jane Munga, in a March 2025 analysis, identified East Africa’s regulatory fragmentation — multiple countries with separate licensing frameworks for cable landing stations — as a vulnerability that foreign infrastructure owners can exploit commercially, even without malicious intent.

“African regulators have consistently focused on data residency as the primary instrument of digital sovereignty — where the data sits — while leaving largely unaddressed the more consequential question of who controls the infrastructure on which it sits and under what legal framework that control can be exercised. These are not the same question, and conflating them has left the continent’s data protection architecture with a significant structural gap.”

— Alison Gillwald, Executive Director, Research ICT Africa, 2025 policy paper on digital infrastructure governance

For G42’s Olkaria campus, the sovereignty question is particularly pointed. G42 is controlled by Sheikh Tahnoun bin Zayed Al Nahyan, the UAE national security adviser and Abu Dhabi’s intelligence chief. When US Congressional hearings in 2024 scrutinised G42’s ties to Chinese technology and its data access practices, the scrutiny landed weeks after Kenya signed its billion-dollar partnership. African governments were not part of that conversation.

West Africa Does It Differently

The contrast with West Africa is instructive. West Africa’s submarine cable infrastructure is characterised by two ownership models: national telecom consortiums (WACS, ACE) and US Big Tech (Google’s Equiano, Meta’s 2Africa). Gulf capital has no direct investment in West African cables. The private sector breakthrough — MainOne, acquired by US data centre firm Equinix in 2022 — brought American capital, not Gulf capital.

East Africa’s geography explains the divergence. The Indian Ocean route from East Africa to the Gulf is the natural corridor for both cable systems and data traffic. Gulf states building their own digital corridors — partly to reduce dependence on maritime chokepoints like the Strait of Hormuz — find East Africa a logical terrestrial waypoint. West Africa faces the Atlantic; East Africa faces Arabia.

The implication is that East Africa is not inheriting a neutral global internet. It is inheriting an internet whose physical infrastructure is being shaped by the geopolitical interests of Gulf states flush with sovereign capital and building their own digital empires.

The Case for the Infrastructure

The capacity argument for Gulf investment is real and should be taken seriously.

Only 38% of Africa’s population used the internet in 2024, according to the ITU. In East Africa, the usage gap — people with network coverage who do not actually connect — stands at 68%. Entry-level broadband costs the average East African 4.2% of their monthly income, more than double the UN affordability threshold. The IFC estimates the continent needs $13 billion in undersea infrastructure investment between 2025 and 2027 just to close its bandwidth deficit.

Before the 2Africa cable’s activation in late 2025, most East African cloud traffic was routed through South Africa — a 4,000-kilometre detour that added latency, cost, and congestion. G42’s Olkaria campus, whatever the ownership concerns, creates the region’s first genuine hyperscale cloud region. For a Kenyan startup trying to access Azure, the difference is material.

New America’s 2025 analysis found that three hyperscale providers — AWS, Microsoft, and Google — already control 60% of African cloud spending. The arrival of G42 does not add a new dominant player; it reshapes the political economy of who backs the existing one. Microsoft’s partnership with G42 is not a displacement of US tech influence — it is an expansion of it, financed by Gulf capital.

The Threshold Question

What is the sovereignty risk threshold? At what point does Gulf investment in East African digital infrastructure become a liability rather than an asset?

The Internet Society’s 2024 East Africa outage report documented that landlocked countries — Rwanda, Uganda, Burundi, Malawi, Zimbabwe — have zero direct submarine cable access and depend entirely on transit agreements through coastal neighbours. For those countries, any cable investment, regardless of ownership, expands resilience. The calculus is different for Kenya or Tanzania, which already have multiple landing points.

The critical test is not ownership but conditionality: what commitments, if any, do Gulf investors attach to infrastructure deals? G42’s partnership terms with Kenya have not been made public. The TEAMS cable agreement, signed in 2006, predates East Africa’s data protection frameworks entirely. The 2Africa Pearls extension is governed by consortium arrangements that no East African government negotiated unilaterally.

The Communications Authority of Kenya licenses cable landing stations and can set operational conditions. It has not published a framework for reviewing the national security implications of foreign infrastructure ownership. The Tanzania Communications Regulatory Authority has similarly been silent.

East Africa’s data is increasingly stored on locally-resident hardware. Who built that hardware, who holds the keys to its operating systems, and under what legal framework a foreign sovereign could request access to it — these questions remain, for now, officially unasked.

Primary sources: Microsoft/G42 announcement (May 2024); Internet Society East Africa Submarine Cable Outage Report (2024); Internet Society Policy Brief on Submarine Infrastructure Resilience (2025); Carnegie Endowment, “Beneath the Waves” (March 2025); New America, “Africa’s Digital Sovereignty Trap” (2025); ITU connectivity data (2024); IFC infrastructure investment projections; Kenya Data Protection Act 2019 (Section 50); TeleGeography Africa Telecommunications Map (2025).