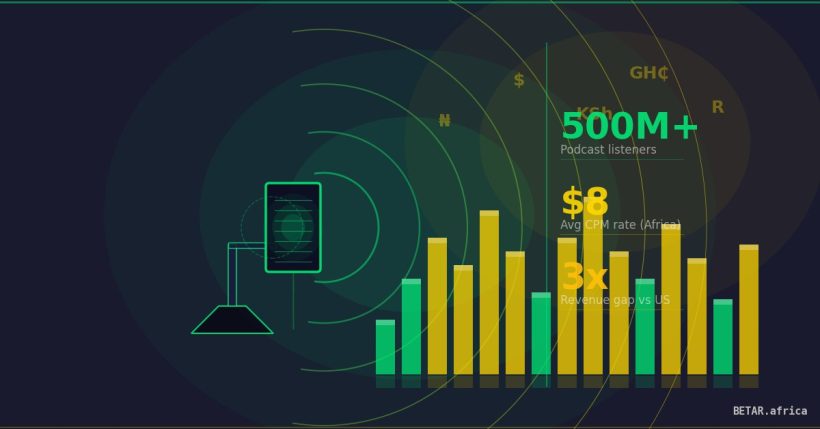

Nigeria has an estimated 80 million podcast listeners. South Africa has 42.7 million. Kenya has 23 million. By audience scale, African podcasting is a major industry. By advertising revenue, it barely registers. South Africa’s podcast advertising market generated approximately $6.57 million in 2024, according to Statista market data — a figure smaller than the annual sponsorship budget of a single mid-tier European radio network. That is not an audience problem. It is a monetisation architecture problem.

Understanding why requires examining how African podcasts actually make money — and why the economics structurally disadvantage African creators relative to global peers at equivalent audience sizes.

The CPM Gap and Its Structural Causes

Podcast advertising is priced on a cost-per-thousand-impressions (CPM) model. In the United States, host-read mid-roll sponsorships — the dominant format for podcast monetisation — command CPMs of $25 to $40 on established shows, per industry benchmarks compiled by Ad Results Media and Adopter Media (2025). In African markets, equivalent host-read sponsorships generate CPM rates in the $5 to $15 range — a gap of three to five times, driven by three compounding structural factors.

The first is audience geography. Global advertisers applying programmatic or network-based buying assign lower CPM values to audiences in emerging markets, regardless of listener engagement or purchasing power. A Lagos-based podcast listener generates a fraction of the advertising value of a New York listener in a data-driven buying model — even if that Lagos listener has equivalent or higher disposable income within their market context.

The second is measurement infrastructure. The Interactive Advertising Bureau (IAB) certifies podcast measurement technology to verify download and listening data to industry standards. Most African podcast hosting platforms and distribution networks are not IAB-certified. Advertisers willing to pay premium rates for verified audience data cannot verify African podcast audiences at the level of rigour they apply to US or European buys. The premium paid for certainty in Western markets is not available in African ones.

The third is brand budget fragmentation. Nigeria’s largest podcast advertisers — telcos (MTN, Airtel), fintechs (Palmpay, OPay), and FMCG companies — allocate podcast-specific budgets that are a fraction of their overall media spend. The podcast line item in a Nigerian brand’s media plan is structurally smaller than the equivalent in a US brand’s plan, compressing the price advertisers will pay regardless of audience quality.

Platform Economics: The Spotify Gap

Spotify for Podcasters offers direct monetisation through its Partner Program, providing creators with a share of advertising revenue inserted by the platform. When the programme launched in January 2025, it was available in four markets: the United States, United Kingdom, Canada, and Australia. It has not been extended to Nigeria, Kenya, or South Africa as of early 2026.

The commercial consequence is direct: African podcasters cannot access Spotify’s programmatic ad insertion revenue on their content, regardless of how many Spotify listeners they have. The platform distributes their content across its African subscriber base but does not share advertising revenue from that content with creators in those markets.

Spotify’s Africa-specific intervention has taken a different form. The Spotify Africa Podcast Fund, launched in 2022, allocated $100,000 across 13 grantees — an average of approximately $7,700 per recipient — as production support rather than an ongoing revenue mechanism. Donald Aryee, co-founder of Ghanaian podcast network The Gold Coast Report (host of Sincerely Accra, one of the 2022 grantees), described the fund as recognition rather than income: the grant covered production costs for a season but did not resolve the underlying monetisation infrastructure problem for African creators.

Apple Podcasts Subscriptions, the other major platform monetisation mechanism, charges subscribers $0.99 to $9.99 per month in markets where the product is available. African creator participation requires an Apple developer account and operates in currencies and payment infrastructures that add friction for both creators and audiences. Subscription conversion rates in African markets are structurally lower than in high-card-penetration markets.

The Direct Brand Deal Model

For viable African podcasts, direct brand sponsorships — negotiated independently of any platform — are the primary income mechanism. This requires audience size, engagement data, and a pitch process that functions as a sales function.

Aisha Salaudeen, co-founder of Lagos podcast production company Twenty-Seven Productions, described the commercial reality plainly: “Advertising is the most popular means of monetisation.” The pitch sequence she outlined tracks the economics precisely: “After the first season, I was able to go to these brands and say, these are the numbers. Let’s talk.” Building a track record before approaching advertisers is not optional — it is the entry condition for the conversation.

Justin Norman, founder and host of The Flip podcast (Johannesburg), confirmed the structure with a specific case: “In the case with MFS Africa, they sponsored one season just to start, and after that season they were interested in continuing.” The initial season commitment purchases audience proof; the renewal converts proof into a stable revenue relationship.

Dan Aceda, founder of SemaBOX — Nairobi’s leading podcasting studio and creator support hub — articulated the minimum viable audience benchmark for sponsor interest: “If a podcast has only about 4,000 listeners, but they always listen and every episode consistently has about 4,000–5,000 listeners, sponsorship partners tend to be very interested.” Engagement consistency matters more to brand buyers in African markets than raw listener volume — a reflection of the market’s preference for demonstrable audience loyalty over unverified scale.

The brand deal mechanics held through 2024. Mantalk.ke, a Nairobi podcast co-hosted by Eli Mwenda and Oscar Koome, ran 250 episodes over five years before securing its first major corporate sponsor in October 2024 — when Johnnie Walker came on board alongside Spotify production support. The show had accumulated 170,000 subscribers across YouTube and social media before brands took commercial interest. The partnership was sentiment-aligned rather than product-focused: “It’s them promoting positive media — it’s not product-focused. It’s more to do with the sentiment of ‘keep walking’ and walking through life’s challenges,” Mwenda told African Business in June 2025. The trajectory — years of self-funded production, audience accumulation, then a values-aligned brand relationship — confirms the direct deal model as the structural norm for commercially viable African podcasting.

The advertiser-side friction persisted into 2025. Danny, co-host of Zimbabwean podcast 2 Broke Twimbos, told Africa Podcast Day 2025 that “securing advertisers has been difficult, with most successful advertising sponsorships coming from the diaspora” — a dependency that maps directly onto the geography-driven CPM gap: diaspora-based advertisers apply US and UK CPM floors to African podcast buys, making them structurally more viable brand partners than domestic advertisers operating with compressed local media budgets. Benjamin Pius, CEO of Broadcast Media Africa, characterised the structural position in May 2025: “Podcasting and on-demand audio are Africa’s next frontier for content engagement — full of promise but still economically underdeveloped.”

Production Cost Economics

The cost floor for a professionally produced African podcast varies significantly by market and production standard.

At the entry level — a home-studio recording using a quality condenser microphone (R1,200–R3,000 in South Africa; ₦40,000–₦100,000 in Nigeria), a USB audio interface (R600–R2,000), and free or subscription DAW software — a creator can produce broadcast-quality audio for a capital outlay of $150–$400 and ongoing hosting costs of $10–$50 per month.

At the professional tier — studio-recorded, professionally edited, with intro/outro music licensing, show notes, and distribution management — costs rise substantially. SemaBOX in Nairobi rates production sessions from KSh 2,000 ($16) to KSh 35,000 ($292) per episode. A weekly professional podcast at Nairobi rates, produced at the mid-tier level, costs approximately KSh 8,000–12,000 per episode ($63–$95), or roughly $3,300–$5,000 per year for 52 episodes. Lagos and Johannesburg professional production is broadly comparable after currency conversion, with higher cost variance across studio providers.

What the cost analysis reveals is that the revenue threshold for breakeven is significantly higher than casual audience estimates suggest. A podcast with 10,000 monthly listeners per episode, monetised at $10 CPM through direct brand deals, generates approximately $400–$600 per month in sponsorship revenue across two to three ad slots per episode. That figure covers professional studio costs at Nairobi rates but leaves little margin for creator income. The equivalent audience in the US market at $30 CPM generates $1,200–$1,800 per month — demonstrating the 3× multiplier effect of CPM differential on creator economics at identical audience sizes.

SemaBOX’s internal data, reported in 2022, found that Nairobi’s top 70 podcasts generated approximately $48,000 cumulatively in a year — an average of $686 per podcast. That figure, even allowing for growth since 2022, illustrates the gap between podcast prominence and podcast income in the African market.

The Monetisation Threshold Problem

The structural implication is a market access problem as much as a revenue problem. To earn $3,000 per month from podcast advertising at African CPM rates — a threshold that would cover production costs and a modest creator income — a Nigerian podcast needs approximately 300,000 monthly downloads. The equivalent threshold in the US at $30 CPM is roughly 100,000 monthly downloads. The Nigerian creator must build three times the audience to reach the same income.

Maurice Otieno, Executive Director of Baraza Media Lab in Kenya, identified the foundational constraint: “The internet is not widely distributed and the cost of data is still very high. Once this is sorted, either through investments in the infrastructure or in innovation, then it can become easier to monetize.” Audience scale is ultimately a data cost and connectivity problem in markets where streaming 40 minutes of audio represents a non-trivial daily data expense for many listeners.

The podcast network model — aggregating multiple shows under a single sales umbrella to offer brands scale across a curated audience — represents the most credible structural response to the CPM and measurement problem. By packaging audience across 10 to 20 shows for a single brand sponsorship, networks can offer advertisers IAB-equivalent reach guarantees through aggregated data, improving effective CPM for all member creators. South Africa’s BizPodcasts and Nigeria’s The Podcast Network represent early iterations of this model; their development will determine whether African podcast monetisation can approach the structural parity that audience size would already justify.

Sources: South Africa podcast advertising market $6.57M (Statista, 2024); Nigeria 80M listeners, South Africa 42.7M, Kenya 23M (The Creative Brief Africa, 2025); Global host-read podcast CPM benchmarks $25–$40 (Ad Results Media; Adopter Media, 2025); African CPM range $5–$15 (BETAR.africa analysis of direct brand deal rates reported by African podcast industry sources); Spotify Partner Program markets January 2025 (Spotify Newsroom); Spotify Africa Podcast Fund $100,000 / 13 grantees (Reuters Institute for the Study of Journalism, 2024); Donald Aryee / The Gold Coast Report (Reuters Institute); Aisha Salaudeen / Twenty-Seven Productions (TechCabal, August 2022); Justin Norman / The Flip (TechCabal, August 2022); Dan Aceda / SemaBOX — studio rates and creator economics (TechCabal, August 2022); Maurice Otieno / Baraza Media Lab (TechCabal, August 2022); Eli Mwenda / Mantalk.ke — brand deal economics and Johnnie Walker sponsorship (African Business, June 2025); Danny / 2 Broke Twimbos — advertiser difficulty and diaspora sponsorship dependency (Africa Podcast Day 2025); Benjamin Pius / CEO, Broadcast Media Africa (Broadcast Media Africa, May 2025); Production equipment cost benchmarks (BETAR.africa analysis of South African and Nigerian electronics retail pricing, 2025); SemaBOX cumulative earnings data (TechCabal, 2022); Podcast hosting costs (Buzzsprout; Spotify for Podcasters platform pricing).