Africa’s Short-Form Video Creator Economy: The Attention Is African. The Money Is Not.

Nigerian creators have built a global short-form video industry. Afrobeats dance challenges originating in Lagos rack up hundreds of millions of views on TikTok. Nairobi food creators draw audiences across four continents. South African comedy Reels go viral in markets where creators have never set foot. Yet for most African short-form creators, platform revenue from that attention is either structurally suppressed or absent entirely — while the infrastructure that would connect viral reach to sustainable income remains incomplete.

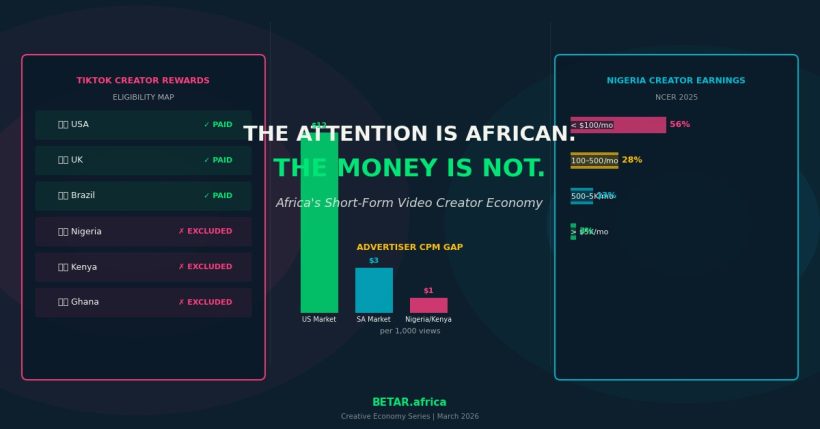

The African creator market was valued at $5.10 billion in March 2025 and is projected to reach $29.84 billion by 2032, according to market research cited by Techpoint Africa. But those aggregate figures obscure a more granular reality: 56% of Nigerian creators earn under $100 per month, and just 3% clear more than $5,000, according to the Nigeria Creator Economy Report (NCER) 2025, developed in collaboration with the Federal Ministry of Art, Culture, Tourism, and the Creative Economy. The short-form video segment sits at the sharpest edge of that divide.

Platform Payment Economics: Who Gets Paid

TikTok’s Creator Rewards Program — the company’s primary direct creator payment mechanism, replacing the earlier Creator Fund — is available in eight markets globally: the United States, United Kingdom, Germany, France, Japan, South Korea, Mexico, and Brazil. Nigeria, Kenya, Ghana, and Tanzania are not on the list. Neither is the rest of Sub-Saharan Africa, with the narrow exception of South Africa and Egypt, which qualify only for TikTok’s Effect Creator Rewards scheme — a separate program that pays creators when their augmented reality effects are used by other users, not for standard video content.

The practical consequence is that Nigeria, TikTok’s second-largest African market with an estimated 34 million monthly active users, receives zero direct platform payment for video content. “The money I made from the platforms themselves has been so small that I can’t even count it as real income,” Foyin Ogunrombi, a South African-Nigerian beauty creator, told OkayAfrica in a piece examining TikTok’s structural exclusion of African creators.

In markets where the Creator Rewards Program operates, payment rates run between $0.40 and $1.00 per 1,000 qualifying views — a substantial improvement on the legacy Creator Fund’s $0.02–$0.04 per 1,000 views, but one that benefits none of Africa’s largest creator populations. For African creators who hold accounts with VPN-assisted registration in eligible markets, payments are inconsistent and withdrawal infrastructure is unreliable; PayPal access is limited across much of the continent, and Stripe — the primary payout processor for many platform programmes — has limited coverage outside South Africa and a handful of North African markets.

YouTube’s Shorts monetisation programme is available across more African markets, but the economics are comparably thin. YouTube Shorts RPM rates globally range from $0.01 to $0.06 per 1,000 views — already a fraction of long-form YouTube RPMs of $2.00–$5.00 — with creators whose audiences skew toward Sub-Saharan Africa earning at the lower end of that range. The structural reason is the same as in podcasting and display advertising: African markets attract lower advertiser CPMs. Brands placing ads against African audiences bid $0.50–$2.00 CPM for short-form inventory versus $8–$15 CPM in the US — a 5–8× differential that flows directly through to creator RPM.

Instagram’s Reels monetisation programme, once an active payer through the Reels Play Bonus, has been largely discontinued globally as Meta shifted strategy. African creators using Reels rely almost entirely on brand deals rather than platform-native payment.

Brand Deal Mechanics: The Real Revenue Model

Brand partnerships are not a workaround to missing platform income — for most African short-form creators, they are the entire business model.

In Nigeria, a TikTok creator with 500,000 followers can expect to earn between ₦50,000 and ₦200,000 (approximately $30–$125 at mid-2025 exchange rates) per branded post, depending on niche, engagement rate, and brand category. Fintech brands and telecoms — MTN, Opay, PalmPay — typically sit at the upper end of the range; food and beverage brands cluster lower. Deals are almost always negotiated directly or through informal management arrangements; Nigeria lacks a mature talent agency infrastructure for mid-tier short-form creators, meaning rate-setting is inconsistent and creators regularly undervalue their audience.

South Africa’s short-form market is more formalised. Creator rate cards published by market analysts in 2025 show South African TikTok and Instagram Reels creators charging:

- Micro (10,000–50,000 followers): R2,700–R9,000 per branded post

- Mid-tier (50,000–500,000 followers): R9,000–R90,000 per post

- Macro (500,000–1 million followers): R90,000–R180,000 per post

- Mega (1 million+): R180,000 or more per campaign asset

The South Africa–Nigeria gap is only partially explained by exchange rates. Brand marketing budgets in South Africa are structurally larger relative to media spend, the influencer marketing industry is more sophisticated, and creators have better access to formal MCN (multi-channel network) representation that enforces rate floors.

Short-form brand deals differ from long-form YouTube integrations in ways that matter economically. Short-form deals typically bundle higher frequency at lower per-unit rates — a brand might commission 20 TikTok posts over a quarter for what one long-form YouTube mid-roll integration would cost. The UGC (user-generated content) market adds a further dimension: brands increasingly commission African creators to produce raw, unbranded-looking video content that the brand then runs through its own channels and paid media, without publishing on the creator’s account. These deals, priced globally at $150–$300 per short-form video asset, represent a growing share of creator income but carry no audience-building value for the creator.

Data Costs: The Invisible Tax on African Short-Form

The structural earnings gap for African short-form creators is not only a platform policy problem. High mobile data costs impose an economic ceiling on audience size that constrains creator monetisation at its foundation.

Nigeria’s 1GB data price reached an average of ₦637.5 in July 2025, a dramatic increase from prior years driven by naira depreciation and network operator cost pressures. Streaming one minute of TikTok video at standard quality consumes approximately 7–10MB of mobile data. For a Nigerian viewer on a typical 1GB bundle, that translates to roughly ₦4–₦6 in data cost per minute of content consumed — a non-trivial expense at an income level where data spending already represents 6.2% of average monthly income, according to Alliance for Affordable Internet data. Kenya’s comparable figure is 7.9%.

The economic consequence is a compressed addressable audience. Nigerian TikTok’s 34 million monthly active users skew heavily toward WiFi-connected urban viewers; mobile-only consumers scroll selectively rather than browsing freely, which depresses the session lengths and view counts that determine brand deal valuations. High data costs don’t just hurt viewers — they structurally limit the viral ceiling for African creators by constraining the casual browsing behaviour that drives short-form discovery. A Nigerian creator trying to break 1 million views faces audience infrastructure constraints that a Brazilian or Indonesian creator with comparable data affordability does not.

Nigeria’s national data spend reached ₦721 billion per month as of July 2025 — up 307% from July 2023 — driven by rising prices rather than rising consumption volumes. Internet subscriptions actually fell by 3.41 million in the first half of 2025, suggesting affordability ceilings are already reducing the online population, not expanding it.

The Infrastructure Gap Behind the Earnings Gap

TechCabal’s February 2026 analysis of Africa’s creator economy concluded that “infrastructure, not influence, defines creator earnings in Africa.” The finding holds at every level of the short-form stack.

Payment infrastructure gaps mean platform programmes that exist — YouTube’s Shorts monetisation, TikTok’s Effect Creator Rewards in South Africa — often go unclaimed because creators lack compliant payment accounts, banking documentation, or access to the international payment rails platforms require. Brand deal payments frequently arrive late or in fragmented instalments due to agency cash flow constraints; contracts are informal; disputes are resolved through relationships rather than legal frameworks.

Platform inclusion decisions reflect advertiser demand, not audience size. TikTok’s criteria for Creator Rewards eligibility require markets where advertiser CPMs are high enough to fund creator payouts profitably. Nigerian CPMs have not cleared that threshold. Until African digital advertising spending grows materially — driven by formalisation of FMCG digital budgets, fintech performance marketing, and pan-African brand investment — the platform economics case for full creator programme inclusion remains weak.

The $5.10 billion aggregate valuation of Africa’s creator market is real but concentrated. A small number of mega-creators in Lagos, Johannesburg, Nairobi, and Accra earn at globally competitive rates and represent the visible face of the sector. Below them, a long tail of short-form creators with genuine audiences — 50,000 to 500,000 followers — operate in an economic environment where viral reach and financial return remain systematically disconnected.

Closing that gap requires three parallel changes: platform inclusion decisions that extend Creator Rewards eligibility to Nigeria and Kenya at minimum; domestic digital advertising budgets that lift the CPM floor; and creator management infrastructure that gives mid-tier short-form creators access to the rate negotiation capacity that South African peers increasingly enjoy. Until then, Africa’s short-form creators will keep building the attention economy — on economics designed for someone else’s market.

BETAR.africa is Africa’s source for business, technology, and innovation journalism.