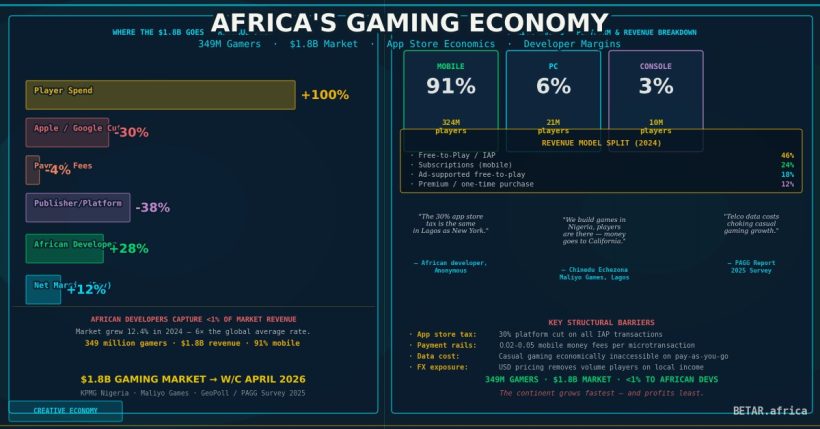

Africa’s gaming market generated $1.8 billion in revenue in 2024 — a 12.4% increase on the prior year and six times the global average growth rate of 2.1%, according to the 2025 Africa Games Industry Report published by KPMG Nigeria and Lagos-based publisher Maliyo Games. The continent added 32 million new gamers in a single year, reaching a total player base of 349 million. Africa is, by growth metrics, one of the most compelling gaming markets on the planet.

African developers captured less than 1% of it.

That is the central economic tension in the continent’s gaming sector. Africa hosts hundreds of millions of players, produces a growing body of locally developed content, and is growing faster than any comparable region — yet the revenue generated by those players flows overwhelmingly to multinational publishers, app store operators, and payment infrastructure providers headquartered elsewhere. Understanding why requires following the money through every layer of the value chain.

The Mobile Monoculture

Mobile is not a subcategory of Africa’s gaming market. It is the market. Approximately 91% of African gamers identify mobile as their primary platform, according to a 2025 survey of 6,000-plus respondents across six countries by GeoPoll and the Pan Africa Gaming Group. Revenue figures confirm the distribution: mobile accounts for roughly 90% of the continent’s $1.8 billion in annual gaming revenue.

The explanation is structural. Console and PC gaming require hardware that most African consumers cannot afford at prevailing price points, particularly in markets with high import duties. Kenya imposes a 25% import duty plus 16% VAT on gaming hardware, effectively multiplying the retail price of a PlayStation or mid-range gaming PC to a multiple of median monthly income. Mobile gaming, by contrast, runs on hardware that hundreds of millions of Africans already own for other purposes — and which is increasingly affordable.

Within mobile gaming, the dominant revenue model is free-to-play with in-app purchases (IAP): games distributed for free, monetised through optional digital items, currencies, or content upgrades purchased inside the game. This model accounted for approximately 46% of Africa’s 2024 gaming market by revenue model share.

The App Store Tax

Every transaction completed through Apple’s App Store or Google’s Play Store — the two dominant distribution channels for mobile games globally — incurs a platform commission. The standard rate for both is 30%. A player who spends $10 in-app on a game published by an African developer generates $3 for Apple or Google before a single cent reaches the developer.

Both platforms operate tiered structures that reduce this burden for smaller operators: Google charges 15% on the first $1 million a developer earns annually; Apple’s Small Business Program offers the same 15% rate for developers earning under $1 million per year. In practice, given that only three African game studios crossed the $1 million revenue threshold in all of 2024 — up from two the year prior — most African developers technically qualify for the lower rate. But qualifying for the lower rate on revenues below $1 million is cold comfort when the sector’s fundamental challenge is reaching meaningful revenue at all.

A structural shift landed in March 2026: Google settled its long-running antitrust dispute with Epic Games and announced it would drop Play Store commissions to 20% globally, with implementation rolling out through 2027. The change also opens Android to rival payment systems and third-party app stores. For African developers, a reduction from 30% to 20% is meaningful — but the more significant implication is the potential for direct-to-consumer distribution channels that bypass platform fees entirely.

The Payment Wall

The app store fee is only the first structural barrier. The second is payment infrastructure.

“Traditional platforms like Google Play or Apple rely on credit cards, and therefore many players just can’t buy the content they want,” Lucy Hoffman, Co-Founder and COO of Carry1st, told Marketplace/NPR. Hoffman’s figure for the scope of the problem: card penetration across Africa stands at approximately 2.7%. The 90%-plus of African gamers without credit card access face a structural barrier to in-app purchases — not a lack of willingness to pay, but an absence of the payment rails that global platforms were built around.

Carry1st, the Cape Town-headquartered mobile games publisher and Africa’s most capitalised gaming company at $65.5 million in total funding, built its business model around solving this friction. Its Pay1st platform aggregates more than 120 local payment methods — M-Pesa in Kenya, bank transfers in Nigeria, mobile wallets in Ghana, and equivalent systems across six countries — into a single embedded payment layer that games can integrate without building country-specific payment stacks.

The commercial outcome has been demonstrable. Since Pay1st’s deployment, Carry1st saw Call of Duty Mobile transaction volumes increase six-fold annually on the African markets it manages. The platform now serves more than one million paying gamers on the continent, and mobile money has matched credit cards as the most common in-game purchase method across its portfolio.

“As large companies like Sony that have really strong footholds in tier-one and tier-two markets start thinking about where the next billion customers and gamers are going to come from, our pitch is that Africa is a prime market for that,” said Cordel Robbin-Coker, Carry1st Co-Founder and CEO, following the company’s strategic investment from Sony’s Africa innovation fund in January 2024. Carry1st’s $27 million Series B, led by BITKRAFT Ventures with participation from Andreessen Horowitz, had closed the year prior.

Esports: Tournament Margins at African Scale

Africa’s competitive gaming sector is growing — but the prize pool economics reveal the gap between player base and revenue capture clearly.

The PUBG Mobile Africa Cup 2025, organised with Carry1st involvement and backed by smartphone brand Infinix, offered a $8,000 prize pool across its format, with the winner qualifying for the PUBG Mobile Global Championship Finals. The IESF African Esports Championship 2024 (PUBG Mobile format, 14 teams) offered $25,000 in total prizes. Carry1st’s Call of Duty Mobile Africa qualifier series across seven regional events distributed $15,000 in total prize money.

The contrast with mature esports markets is stark: prize pools for equivalent-tier tournaments in Southeast Asia or North America run into six and seven figures. Africa’s esports sector — estimated at $40 million for the continent — is generating broadcast viewership and brand sponsorship value that its prize pools do not yet reflect. MTN, Gloo, and Gamers Connect are among the corporate sponsors active in tournament backing, a signal that the brand spend is moving in advance of prize pool growth.

What a Developer Actually Nets

The practical developer economics for a successful African mobile game are illuminating. Consider a studio generating $1 million annually in player revenue — a threshold only three African studios reached in 2024.

At Google Play’s standard 30% commission: $700,000 remains after platform fees. From that, marketing and user acquisition costs — the dominant expenditure for mobile game growth — consume a further significant share. Payment processing for any transactions outside app store billing adds 1.5-3%. Customer support, server infrastructure, and content updates are ongoing. Net margins for mobile game studios globally typically land in the 15-25% range after all operating costs, with higher margins for studios that have achieved scale and reduced acquisition costs through organic growth.

For the three African studios at the $1 million revenue threshold, this implies net income in the range of $150,000 to $250,000 annually — viable, but thin relative to the capital required to build competitive games. The 59% of African studios that the KPMG/Maliyo report identifies as receiving no external investment are building on self-funded economics that compress development cycles and content quality.

Hugo Obi, CEO of Maliyo Games and co-author of the KPMG Africa Games Industry Report, has been direct about the structural dynamic: Africa’s gaming talent is abundant, its player base is growing rapidly, but the revenue infrastructure — payment rails, publisher relationships, and development capital — has not kept pace with either.

The Structural Gap

Africa’s gaming market is growing at six times the global average. Its developers capture less than 1% of a $187 billion global industry. Both facts are simultaneously true — and the distance between them is a measure of infrastructure deficit, not creative or commercial capacity.

The components of that infrastructure are in motion: Carry1st’s Pay1st is expanding payment access, Google’s Epic settlement is opening distribution channels, and Sony’s Africa investment signals institutional capital recognition of the continent’s player base. The question for African developers is whether the infrastructure catches up before the window of platform-building closes — or whether, as in music and film, the value generated by African users continues to flow to the external systems that serve them.

Named sources: Lucy Hoffman, Co-Founder & COO, Carry1st (Marketplace/NPR, March 2024); Cordel Robbin-Coker, Co-Founder & CEO, Carry1st (CNBC, January 2024); Hugo Obi, CEO, Maliyo Games (2025 Africa Games Industry Report, KPMG Nigeria).