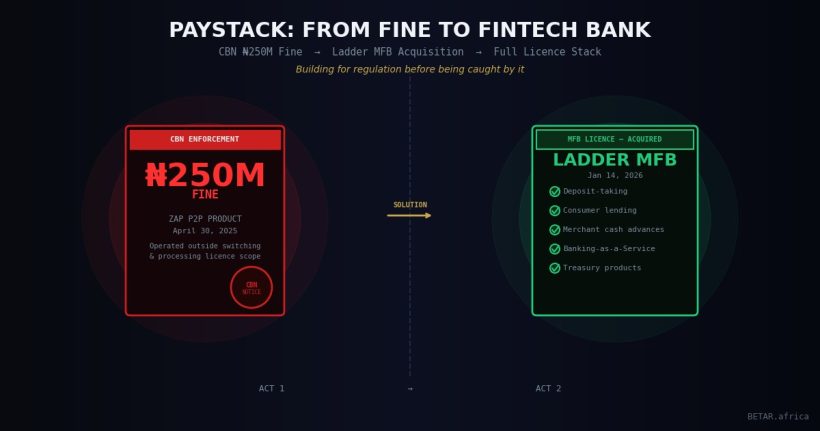

Nine months before Paystack announced it was becoming a microfinance bank, the Central Bank of Nigeria sent the company a signal it could not ignore: a N250 million fine for operating a consumer wallet outside the scope of its switching and processing licence. The fine — imposed in April 2025 over Paystack’s Zap P2P product — and the January 2026 acquisition of Ladder Microfinance Bank are not separate stories. They are the same story. Act one established the problem. Act two is the solution.

Together, the two events reveal something important about Nigeria’s fintech regulatory moment: the CBN is no longer tolerating grey zones, and the companies that survive the next regulatory cycle will be the ones that own their licence stack rather than depend on partnerships to paper over the gaps.

Zap, and the Cost of Operating in the Grey Zone

Paystack launched Zap in March 2025. It was the company’s first consumer-facing product — a peer-to-peer payment app that let users send and receive money directly — and a significant strategic departure for a company that had built its reputation entirely on merchant-facing infrastructure. Zap operated in partnership with Titan Trust Bank, which nominally held the deposits; Paystack was the product layer on top.

The CBN was not persuaded by the structural arrangement. Seven weeks after launch, on April 30, 2025, the regulator issued Paystack a N250 million (~$115,000) fine for operating Zap outside the scope of its switching and processing licence. Paystack’s licence authorises it to route transactions between financial institutions. It does not authorise the company to operate a product that, from a user perspective, functions like a wallet — regardless of which regulated entity technically holds the funds underneath.

Paystack’s public response was careful: “Paystack is working closely with the regulator as they further review Zap, and out of respect for the process, we won’t be making any public comments at this time.” The regulatory exposure, however, was unambiguous. Paystack had built a consumer product its licence did not cover. The fine made that gap visible.

It was also, by Nigerian fintech standards, modest. N250 million is not a company-ending sanction for a Stripe-backed business. The more significant cost was the signal: Paystack could not sustain a consumer product roadmap on a switching licence. If the company wanted to operate in the deposit and lending layer — which is where the durable revenue and the competitive moat both live — it would need a different licence entirely.

Ladder MFB: The Licence, Not the Business

The Ladder Microfinance Bank acquisition, announced on January 14, 2026, is best understood as a regulatory asset purchase rather than a business acquisition. Ladder MFB was incorporated on June 26, 2024 — a six-month-old institution at the point of acquisition, with no significant operating history and a shareholder register consisting of two named individuals. Paystack was acquiring the CBN-issued microfinance banking licence, not a going concern.

What that licence enables, and what Paystack’s switching licence explicitly does not, is the difference between a payments infrastructure company and a financial services company:

- Deposit-taking from customers and businesses

- Working capital loans and merchant cash advances

- Overdraft and credit facilities

- Banking-as-a-Service (BaaS) for other fintechs building on Paystack’s rails

- Treasury management products for corporate clients

Paystack has now rebranded Ladder as Paystack Microfinance Bank, operating it as a separate regulated entity within the group structure. The product roadmap it unlocks is everything Zap attempted to signal: a future in which merchants on the Paystack platform do not just receive payments but access credit, manage working capital, and run their financial operations from a single interface.

Amandine Lobelle, Paystack’s COO, articulated the strategic rationale plainly: “After 10 years of building payment infrastructure… businesses needed more than just getting paid to grow.”

The Stripe Playbook, Applied in Lagos

Paystack’s trajectory is a direct local implementation of what its parent company, Stripe, has been executing globally. Stripe has been pursuing a US banking licence via a Merchant Acquirer Limited Purpose Bank charter in Georgia — a structure that would allow direct access to payment networks without a sponsoring bank intermediary. In the UK and across Europe, Stripe is already a direct network member. The pattern is consistent: reduce dependency on third-party financial institutions by owning the licence at every layer of the stack.

Buying an existing MFB — rather than applying for a greenfield licence — compresses the timeline significantly. A new microfinance bank application in Nigeria typically takes two or more years from submission to operational approval. Acquiring Ladder gave Paystack an operational licence immediately, at a cost that has not been publicly disclosed but almost certainly represents a fraction of the regulatory and capital cost of building from scratch.

Who Else Is Exposed?

Paystack’s situation is not unique. Nigeria’s fintech ecosystem includes dozens of companies that have, in varying degrees, tested the boundaries of their licence categories as product ambition outpaced regulatory clarity. The CBN’s enforcement posture has hardened since 2024: the Paystack fine, alongside sanctions against other payment operators, the BVN phone-number lock mandate, and new AI-based AML requirements, collectively signal a regulator that is actively auditing whether licensed fintechs are operating within their permitted scope.

The companies most exposed are those operating consumer-facing financial products — particularly wallets, lending products, and savings features — under payment service bank licences or switching licences that were designed for narrower applications. The CBN’s review of Zap established a precedent: partnership structures with licensed banks do not automatically transfer liability for unlicensed activity.

Competitive Implications

The acquisition reshapes Paystack’s position in a market that has been actively consolidating. Moniepoint — which already holds an MFB licence — was upgraded by the CBN to national microfinance bank status in January 2026, a designation that requires N5 billion minimum paid-up capital and permits full operations across all 36 states. OPay, Kuda, and PalmPay received the same upgrade simultaneously. The national MFB tier is forming into a distinct competitive category: companies that have sufficient capital and regulatory standing to operate across the full financial services stack in Nigeria.

Paystack MFB enters that category from a different starting point. Where Moniepoint and OPay built mass consumer bases first and scaled the licence, Paystack’s competitive position is built on merchant infrastructure. The working capital and BaaS products the MFB licence enables are merchant-oriented plays — lending against transaction history, extending credit to the businesses that run on Paystack’s rails. That is a narrower, less commoditised surface than consumer neobanking, and potentially a more defensible one.

Flutterwave, the other switching-licensed giant, has not followed Paystack into the deposit-taking layer. Instead, it acquired Mono in January 2026 — an open banking data platform — positioning it in financial data infrastructure rather than balance sheet products. Whether that is a strategic choice or a capital constraint will become clearer as CBN enforcement of licence boundaries continues.

For Paystack, the message of the last nine months is simpler: in Nigeria’s regulated financial services market, you cannot build in the grey zone indefinitely. The fine arrived at the edge of the zone. The acquisition is the exit from it.

BETAR.africa | Business Desk. Related coverage: BETA-1069 — Africa Banks Are Buying the Fintechs They Could Not Build | BETA-1027 — Nigeria Fintech Compliance Cost Stack.