Africa’s education technology sector once attracted record venture capital. Today, that capital has largely gone. Understanding what broke — and who survived — matters for the 300 million Africans who still lack quality education access.

In 2021, Africa’s education technology sector looked like it was about to transform the continent’s learning crisis. Global venture capital was flooding in. Platforms were signing growth rounds. EdTech was the sector where impact investing and return-chasing capital agreed, at last, that the fundamentals worked.

Four years later, that thesis has been tested to destruction.

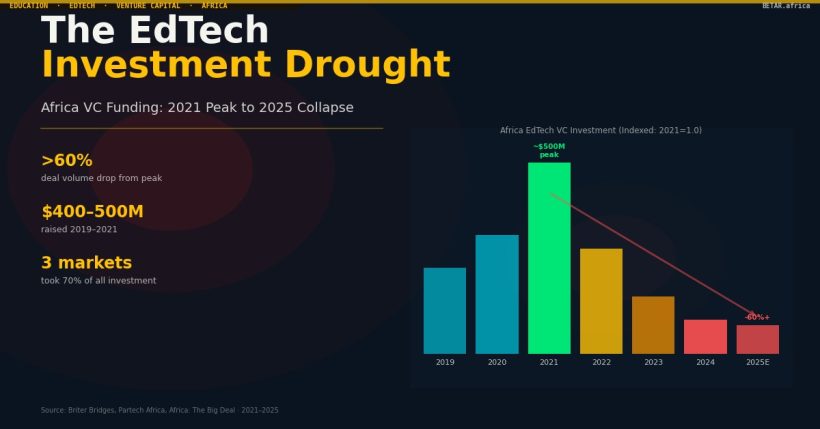

African EdTech raised an estimated $400–500 million in combined funding between 2019 and 2021, including a surge of late-stage rounds and international investor participation driven by COVID-19 pandemic tailwinds, according to data tracked by Briter Bridges and Partech Africa. By 2024–2025, that pipeline had contracted sharply. Deal volume fell by more than 60 percent from peak levels. Several high-profile platforms shut down, pivoted away from consumers, or retrenched to home markets. The sector that was supposed to be Africa’s next fintech is now in the midst of a consolidation that few investors anticipated and fewer platforms survived.

What happened is not a single story. It is three converging failures — in unit economics, in investor patience, and in infrastructure — that arrived at the same time.

The Numbers Behind the Collapse

At its 2021 peak, African EdTech attracted venture investment from Owl Ventures, Pearson Ventures, Novastar Ventures, Horizons Africa, and a range of impact funds drawn by pandemic-era tailwinds. Remote learning demand had spiked. School closures across the continent had created perceived urgency. Investors who had previously passed on Africa’s education market rushed to catch what looked like an inflection point.

The inflection was real. The durability was not.

Nigeria, Kenya, and South Africa accounted for approximately 70 percent of all EdTech investment between 2019 and 2023, per Briter Bridges’ tracking of disclosed deals. Francophone Africa — home to more than 150 million people and some of the continent’s sharpest learning deficits — received a fraction of that total. The capital concentration was not a reflection of demand; it was a reflection of investor comfort zones and English-language platform scalability assumptions.

When post-pandemic conditions normalised and the macro environment tightened in 2022–2023, the EdTech funding gap widened dramatically. US venture capital — which had accounted for a significant share of African EdTech deal participation — pulled back from emerging markets broadly. African EdTech, which had not yet proved sustainable unit economics at scale, was among the first sectors to feel the withdrawal.

Who Folded, Who Pivoted

The casualty list tells the story of a model that worked in controlled conditions but broke against African market realities.

Andela’s trajectory is the most instructive. The pan-African developer training platform raised more than $200 million over its life, including a $100 million round from SoftBank Vision Fund in 2021. It trained tens of thousands of software engineers across Nigeria, Kenya, Uganda, Rwanda, and Egypt. Then it pivoted: Andela exited the direct-training model, closed its physical campuses, and repositioned as a global talent marketplace connecting African engineers to international employers. The shift was commercially defensible — the marketplace model generates revenue at lower cost than the training model — but it illustrates exactly the unit economics problem that undermined the EdTech investment case. Training Africans is expensive. Monetising African learners in African markets is harder still.

Coursera’s Africa retrenchment was quieter but equally significant. The global MOOC platform, which had expanded into sub-Saharan Africa through university partnerships and government deals, scaled back its direct market investment when conversion rates and retention metrics failed to justify the cost of localisation and mobile-optimised delivery. The platform remains available; strategic priority is not Africa.

uLesson, one of Nigeria’s most-funded consumer EdTech platforms, made the survival choice: a pivot from B2C to B2B and government partnership models. The company has expanded state-level contracts in Nigeria, repositioning itself as a school system supplementary resource rather than a subscription product competing for household spend. The pivot preserves the business. It also concedes the original consumer thesis.

The Unit Economics Problem That Nobody Solved

Beneath the individual platform failures is a structural problem that Africa’s EdTech sector has not resolved — and that investors belatedly recognised.

Device penetration among school-age learners remains a binding constraint. Smartphones are widespread among adults in urban Nigeria and Kenya; they are far less accessible among the secondary-school students who are the primary market for most EdTech platforms. Tablets and laptops — the devices that deliver the richest learning experience — are largely absent outside fee-paying private schools.

Connectivity costs compound the problem. Data prices in sub-Saharan Africa remain among the highest in the world relative to income levels, despite meaningful progress in countries like Rwanda and Ethiopia. A student streaming video content for two hours of tutoring is spending a significant share of household daily data allowance. Even zero-rated content partnerships — which several platforms pursued with mobile operators — proved limited by the fundamental cost of maintaining quality learning on intermittent, expensive connections.

Willingness to pay closes the trap. In markets where household education expenditure is already stretched by school fees, uniforms, and textbooks, the marginal parent cannot reliably sustain a monthly subscription for supplementary digital content. The platforms that built consumer subscription models discovered this at scale. Revenue-per-user figures that made sense in pitch-deck projections did not survive contact with market reality.

“The capital that reached Africa’s EdTech sector in 2020–2021 was pricing in a demand signal that was real — disruption was happening — but it was not pricing in the infrastructure and affordability constraints that make monetisation so difficult,” said a senior programme officer at one of the continent’s major education-focused foundations, speaking on background. “The gap between willingness to learn and willingness to pay, in a context where data is expensive and devices are scarce, is wider than anyone wanted to admit.”

Who Is Still Investing — and What They Are Backing

The retreat of venture capital has not meant the end of EdTech investment in Africa. It has meant a decisive shift in who is investing and what they will fund.

The Mastercard Foundation has emerged as the most consequential funder of early-stage African EdTech in the post-boom period. Through its EdTech Fellowship programme — delivered via CcHUB in Lagos and MEST Africa in Accra — it provides non-dilutive grant capital of up to $100,000 per cohort company, alongside mentorship and market access. The focus is deliberately on underserved learners: girls, rural communities, learners with disabilities, and refugee populations that commercial EdTech platforms have not reached.

The African Development Bank’s Human Capital Development Department continues to support EdTech through blended finance instruments, primarily targeted at government-partnership models with demonstrable classroom impact. The IFC has maintained exposure to select B2B platforms. Novastar Ventures, which has held EdTech positions for longer than most Africa-focused VCs, continues to back companies with proven government or enterprise revenue rather than consumer subscriptions.

The common thread is institutional revenue. The platforms receiving investment in 2025–2026 are predominantly B2B or B2G — selling to schools, universities, employers, or governments rather than directly to learners or households. Enko Education, which operates a network of pan-African secondary schools and hybrid learning models, and Educate!, which delivers vocational skills training through school system partnerships in Uganda, Rwanda, and Kenya, both represent the model that survives: institutional revenue, government relationships, and unit economics that do not depend on household willingness to pay.

What the Drought Means for Africa’s Workforce Pipeline

The EdTech investment contraction matters beyond the sector itself. It directly affects the continent’s ability to build the skilled workforce that Africa’s economic transformation requires.

Africa needs an estimated 17 million additional skilled workers in digital and technical fields by 2030, according to analysis by the IFC and development partners. The bootcamp and short-course sector — covered in BETAR’s analysis of ALX, Moringa School, and Decagon — has partially filled the gap that university systems and venture-backed platforms have not. But bootcamp unit economics face the same market realities: high cost of quality instruction, limited learner financing options, and employer willingness-to-hire constraints that remain concentrated in Nigeria, Kenya, and South Africa.

The supply-side problem and the demand-side problem are both real, but they are not the same problem. VC pullback is primarily a supply-side story — risk appetite recalibration, IRR failure, and macro environment changes drove investors out. But the platforms that received capital and still failed mostly hit demand-side walls: device scarcity, data cost, and household affordability. Both diagnoses are correct, and conflating them produces the wrong remedy. Restoring venture appetite will not fix connectivity pricing. Subsidising data will not repair investor confidence in consumer subscription models.

The AU’s design of CESA 2026–2035 — the continental education strategy framework replacing the expired 2016–2025 programme — is an opportunity to embed EdTech infrastructure in policy architecture that shapes national education budgets. If the new framework creates government procurement channels for digital learning tools, it could provide the institutional revenue floor that surviving platforms need to scale sustainably. If it does not, the structural problem persists: the capital willing to fund African EdTech at growth stage has largely gone, and the market conditions that would restore it do not yet exist.

The 300 million Africans who still lack quality education access are not waiting for venture conditions to improve. The platforms, governments, and development finance institutions that remain in the market are the ones now determining what their educational futures look like.