Africa Electricity Tariff Reform Wave 2026: Who Gains, Who Loses, and What It Means for the Energy Transition

From Nigeria to Ghana, Uganda to South Africa, electricity regulators across the continent have approved the biggest tariff increases in a generation. The logic is clear: cost-reflective pricing is the prerequisite for private investment. But the political pain is real, and the distributed energy dividend may be the reform’s most important — and least discussed — consequence.

LAGOS / NAIROBI / ACCRA — For most of Africa’s post-independence history, politically set electricity tariffs have been treated as a social entitlement. Governments priced power below cost, accumulated utility debt, deferred maintenance, and wondered why blackouts persisted. The result was a vicious cycle: cheap power that wasn’t reliably delivered, utilities too broke to invest, and foreign capital that went elsewhere.

That cycle is breaking — slowly, and with considerable political turbulence.

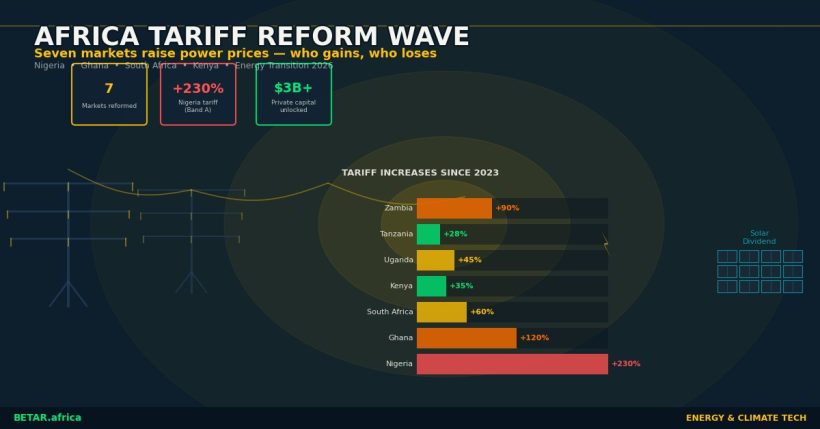

Since 2023, at least seven African electricity markets have pushed through major tariff restructuring: Nigeria, Ghana, Uganda, Tanzania, Kenya, South Africa, and Zambia. The increases range from 15 percent to over 200 percent depending on the market and customer class. Regulators, backed by the International Finance Corporation, the African Development Bank, and a growing consensus among infrastructure investors, argue that cost-reflective tariffs are the non-negotiable foundation for a viable private power sector — and without a viable private power sector, Africa’s energy transition is a policy document, not a reality.

The argument is winning. But the consequences — for households, for small businesses, and for the distributed energy players whose economics are being rewritten — are only beginning to play out.

The Scale of the Shift

Nigeria provides the starkest example. Under the Electricity Act 2023 and the subsequent Multi-Year Tariff Order (MYTO) revision, the Nigerian Electricity Regulatory Commission (NERC) approved a tariff increase for Band A customers — commercial and industrial users who receive at least 20 hours of power daily — from approximately N68 per kilowatt-hour in 2022 to over N225 per kilowatt-hour by mid-2025. That is a nominal increase of more than 230 percent across three years.

The reform is deliberate. NERC is implementing cost-reflective pricing for higher-consumption customers first — insulating the poorest residential users from the immediate shock while sending the investment signal to private generators. Bands B through E, serving customers with 16 hours or fewer of supply per day, have seen more modest increases.

Ghana’s trajectory is similar. The Public Utilities Regulatory Commission (PURC) has approved three successive tariff revisions since 2023, with the most recent — an 18 percent increase effective January 2026 — specifically designed to reduce the government’s quasi-fiscal exposure to ECG, the state electricity distributor. Ghana’s power sector accumulated over $1.5 billion in arrears to independent power producers between 2018 and 2023; cost-reflective tariffs are the IMF-backed path to ending that structural drain.

Uganda’s Electricity Regulatory Authority completed a comprehensive cost-of-supply study in Q4 2025 that underpins new retail tariffs for commercial users. Tanzania’s Energy and Water Utilities Regulatory Authority approved a 15 percent tariff increase for industrial customers in Q1 2026. Kenya’s Energy and Petroleum Regulatory Authority is reviewing the retail tariff structure alongside a new feed-in-tariff framework for distributed generation. South Africa’s National Energy Regulator (NERSA) has approved above-inflation Eskom tariff increases in four consecutive years, with the 2025/26 bulk tariff sitting 18.65 percent above the prior year.

Zambia, still recovering from the Kariba reservoir drought crisis, is attempting to use tariff reform to accelerate the solar diversification it was forced into by climate shock.

The Investment Logic

The link between tariff cost-reflectivity and private power investment is not theoretical. It is the single most consistently cited barrier by infrastructure fund managers operating on the continent.

“The bankability question for any power project in Africa starts with the offtake,” says a partner at a leading African infrastructure fund who asked not to be named. “If the utility is buying power at $0.09 per kWh and selling it to customers at $0.04, you have a structural deficit that eventually becomes a payment default. No debt fund can underwrite that credit risk.”

AIIM, one of Africa’s largest infrastructure asset managers with over $3 billion under management in energy assets, has published research showing that the correlation between cost-reflective tariffs and private power investment flows is statistically significant across markets. Markets that have sustained cost-reflective pricing for at least three consecutive years attract substantially more private generation capacity than those that haven’t.

The IFC’s 2025 Africa Private Power Tracker identified tariff reform as the primary enabling condition for the 47 GW of private capacity that Africa needs to add by 2030 to meet universal access targets. Without it, the tracker notes, even blended finance instruments — guarantees, first-loss tranches, concessional lending — cannot overcome the revenue risk embedded in below-cost tariff structures.

Nigeria’s electricity sector is already showing early signs of the reform dividend. Meristem Securities analysts noted a 34 percent increase in applications to NERC for new generation licences in the twelve months following the MYTO Band A revision. Whether those applications convert to financial close depends on transmission and distribution infrastructure — but the generation investment signal has shifted.

The Distributed Energy Dividend

There is an irony embedded in the tariff reform wave that energy transition analysts are only beginning to appreciate: the more expensive grid electricity becomes, the stronger the business case for leaving the grid.

For Nigeria’s Band A commercial customers, a grid tariff of N225/kWh+ is now directly competitive with — and in many locations more expensive than — a well-financed rooftop solar-plus-battery system with a 15-year amortisation schedule. CrossBoundary Energy, which develops commercial and industrial solar projects across Africa, has cited the MYTO revision as the single most important commercial development in the Nigerian C&I solar market in a decade.

“The math has flipped,” a CrossBoundary analyst told investors at a conference in Lagos in February 2026. “Before the tariff revision, the grid was a cheap competitor we had to undercut. Now we are cost-competitive with grid power for Band A customers, and we provide a reliability premium that the grid cannot match.”

Yellow Door Energy, which has developed over 200MW of commercial solar across Africa and the Middle East, has publicly flagged Nigeria and Ghana as its highest-growth markets for 2026-2027 precisely because of tariff reform. The company’s internal hurdle rate for new projects — based on grid parity calculations — is now cleared in both markets without requiring concessional financing.

The same dynamic is playing out in the mini-grid sector. As grid electricity prices rise, the threshold at which a mini-grid can offer competitive rates to peri-urban and rural customers while generating an adequate return for investors falls. GOGLA, the association for off-grid solar companies, estimates that a 20 percent increase in urban grid tariffs typically expands the viable mini-grid catchment area by 15 to 20 percent, as households and businesses on the grid’s weak fringe recalculate their options.

Battery energy storage — already experiencing its own cost deflation curve — is further accelerating the calculus. South Africa’s C&I BESS market grew by over 300 percent in installed capacity between 2023 and 2025, driven almost entirely by commercial users seeking to optimise against Eskom’s Block 4 tariffs and avoid demand charges during peak periods.

The Consumer Squeeze

The distributed energy dividend is real. It is also, for now, largely inaccessible to the customers who are most exposed to tariff increases.

Households in the bottom three consumption quintiles — the majority of African electricity users — do not have the capital or creditworthiness to install solar-plus-storage systems. Micro and small enterprises are similarly constrained. For these users, tariff reform without adequate social protection is simply a price increase.

Nigeria’s tiered approach — protecting lower-consumption residential customers in Bands D and E from the full Band A shock — is the most sophisticated reform design currently in operation on the continent. But it is not without friction. Politically connected commercial users have lobbied for classification as Band D or E customers despite consumption patterns that clearly qualify them as Band A. NERC has acknowledged the metering and classification integrity problem.

Ghana’s situation is more acute. The 18 percent PURC increase was applied uniformly across customer classes, with a parallel Low-Income Lifeline Tariff theoretically protecting the poorest residential users. Civil society organisations monitoring electricity affordability in Greater Accra have documented significant targeting failures in the lifeline tariff — households that should qualify are not accessing the protection because of metering irregularities, billing disputes, and lack of awareness.

The political risk is not hypothetical. South Africa’s 2023 Eskom tariff increase triggered the first organised consumer protest action in the electricity sector in years. Nigeria’s 2024 MYTO revision was met with a three-day commercial strike by market associations in Aba and Onitsha. Ghana’s January 2026 increase is still in its early months — but consumer advocacy groups have warned that the PURC decision, combined with currency depreciation and inflation, has pushed electricity costs beyond what small businesses in Accra’s informal economy can absorb.

The Political Risk

Cost-reflective electricity pricing is a reform that has been attempted — and reversed — multiple times across Africa over the past 30 years. The pattern is consistent: a technocratic consensus drives the reform through the regulatory process; the political system absorbs the shock until election pressure or street mobilisation triggers a rollback; the utility falls back into deficit; foreign investors lose confidence; and the cycle repeats.

The current wave has several features that may make it more durable. IMF programme conditionality in Ghana and Zambia gives institutional backstop to the reform. Nigeria’s Electricity Act 2023 embedded cost-reflective tariff principles in legislation, raising the threshold for reversal. South Africa’s Eskom tariff process, while politically contentious, is now well-established as an annual regulatory event rather than an exceptional measure.

But durability is not guaranteed. Nigeria’s 2023 fuel subsidy removal — the prerequisite for the MYTO Band A revision — is now being partially reversed through targeted subsidy programmes that undermine the macroeconomic rationale that made the power sector reform possible. Ghana faces a general election cycle in which electricity affordability will be a mobilising issue. Tanzania’s industrial tariff increase drew immediate pushback from the manufacturers association.

The critical variable is whether the investment flows that tariff reform is designed to unlock actually materialise quickly enough to produce visible supply improvements before political sentiment turns. If the lights get better because tariffs went up, reform survives. If the lights stay the same or get worse, it doesn’t.

Who Wins the Transition

The tariff reform wave is reshaping the competitive landscape of Africa’s clean energy sector in ways that are only beginning to be priced into investment theses.

The clearest winners are commercial and industrial solar developers with established Africa portfolios — CrossBoundary Energy, Yellow Door Energy, Distributed Power Africa, Starsight Energy — whose grid parity calculations have turned positive in at least four major markets this year. The pipeline visibility for C&I solar in Nigeria, Ghana, South Africa and Kenya has improved materially.

Battery energy storage developers are the secondary winners, as commercial users increasingly combine solar generation with storage to optimise against time-of-use tariffs and demand charges. The economics of BESS in African C&I applications have reached a tipping point that is independent of the technology cost curve — it is tariff structure, not panel prices, that is driving the current deployment surge.

The potential losers in the transition period are mini-grid developers operating in markets where grid extension is now being financed with the revenue surplus from higher tariffs. A better-financed utility extending the grid to peri-urban communities is a competitor to the mini-grid operators who invested on the assumption of a perpetual supply gap. That calculus is changing — and not all mini-grid investors are positioned for it.

For the 600 million Africans still without reliable electricity access, the tariff reform wave is a necessary but insufficient condition for progress. It attracts the private capital that government budgets cannot mobilise. But it requires paired investments in social protection, metering infrastructure, and — above all — actual generation and distribution capacity that delivers the supply improvement that justifies the price increase.

The reform wave is real. The investment signal is improving. Whether the power actually arrives in time to sustain the political will behind it — that is Africa’s energy transition question for 2026 and beyond.

This article is part of BETAR’s ongoing coverage of Africa’s energy transition. Related coverage: BETA-878 (Africa Clean Energy Finance Q1 2026), BETA-758 (Kenya’s Clean Grid Paradox), BETA-867 (Africa BESS 2026), BETA-588 (Nigeria DARES $750M Solar Mini-Grid).