Africa’s Renewable Energy Auction Crunch: Record-Low Bids, Rising Cancellations — Why the Projects That Win Are Not Getting Built

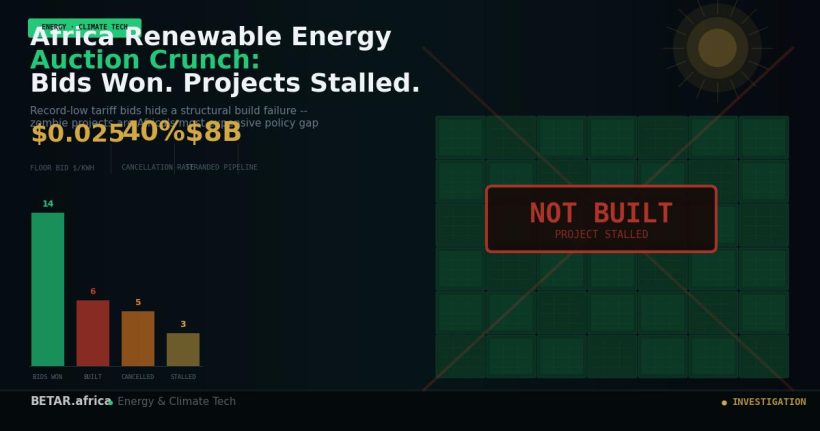

Across Africa, renewable energy auctions are producing some of the lowest electricity tariff bids ever recorded. South Africa’s Round 7 REIPPPP saw bids below $0.025 per kilowatt-hour — cheaper than coal, cheaper than gas, competitive with anywhere on earth. Egypt’s 1 GW solar race attracted AMEA Power and Scatec at similarly aggressive prices. Kenya’s first competitive independent power producer auction under its new Electricity Act generated bids from multiple developers for the same generation capacity. On paper, the continent’s renewable energy transition is accelerating. On the ground, a growing number of those winning projects are stalled, suspended, or quietly cancelled — and the gap between bid and build is becoming one of the continent’s most expensive policy failures.

The phenomenon has acquired an informal name among infrastructure lawyers and development financiers: the zombie project. A zombie project has won an auction, holds a power purchase agreement, occupies a grid queue position, and appears in government statistics as commissioned capacity. But it has not achieved financial close. It is not under construction. It may never be built. And while it occupies the queue, it blocks other developers from moving forward.

BETAR.africa has spoken with developers, development finance institution officials, and energy policy advisers across five markets to understand how a sector that should be capitalising on record-low solar costs is instead building a growing inventory of unfinanced promises.

The Hedging Arithmetic

The core problem is visible in the numbers. Solar panel prices have fallen roughly 90% over the past decade. The levelised cost of solar electricity, absent financing costs and currency risk, is now genuinely competitive with fossil fuel generation across most of Sub-Saharan Africa. This is why auction bids are low — developers are passing through real cost reductions.

But the financing cost is not absent. And currency risk is not abstract.

Consider the Egypt case. Egypt’s pound has lost more than 50% of its value against the US dollar since 2022. Solar development in Egypt requires imported equipment — panels, inverters, racking systems — priced in US dollars or euros. Construction financing is typically US dollar-denominated. But Egyptian power purchase agreements pay in Egyptian pounds, either directly or with a currency adjustment mechanism that does not fully insulate developers from depreciation risk. A project that was viable at a tariff of $0.025/kWh when the pound was at 30 to the dollar has a materially different economics when the pound is at 50 to the dollar — and developers negotiating PPAs in 2024 had no way to know where the rate would be by financial close in 2026.

The same calculation applies in Nigeria (naira depreciation of more than 60% since 2023), Ghana (cedi down 40% over two years), and to a lesser extent Kenya (shilling depreciation of roughly 25% since 2021). Each of these markets has run competitive renewable energy procurement in the same period that their currencies have been under pressure. The developers who submitted the lowest bids typically assumed either a stable exchange rate or the availability of hedging instruments that, in practice, are not accessible at commercially viable cost.

IFC and MIGA have been working for the past 18 months on a currency hedging product specifically designed for African renewable energy PPAs. The fact that a new product category is required to make the sector financeable is, itself, a signal about the scale of the problem. The product — which would cap currency depreciation exposure at a premium comparable to political risk insurance — remains in development. The zombie projects are already in the queue.

The Grid Connection Bottleneck

Currency risk is the headline problem, but grid connection delay is a close second — and in some markets it is the binding constraint.

Kenya’s KETRACO, the state-owned transmission company, has a publicly disclosed grid connection queue that extends to 2028 for some substations serving the regions where solar development is most economically viable. Developers who won Kenya’s first competitive renewable energy auction under the 2023 Electricity Act have been told that their grid connection date has slipped by 12 to 18 months from the timeline assumed in their bid. At current financing costs, an 18-month delay in a project with $50 million in committed equity and construction financing in place is not an inconvenience — it is a potential project-killer.

South Africa’s grid queue problem is better documented but no less severe. Eskom’s application-to-connect backlog runs to more than 80 GW of projects — representing more than twice the country’s total installed generation capacity — and the queue management system introduced in late 2023 has improved transparency without meaningfully accelerating connection times. REIPPPP Round 7 winners are working through the new framework, but developers who submitted bids based on 2026 grid connection dates are increasingly revising their financial close targets toward 2027.

Tanzania’s situation reflects a different dynamic: the grid does not exist in the areas where the best renewable resources are. Large solar and wind resources in the country’s central and southern regions are stranded because TANESCO’s transmission network was built to serve the old hydro-dependent northern grid. Any meaningful scale-up of utility-scale renewables in Tanzania requires either a major transmission investment or a distributed generation strategy that bypasses the national grid entirely. Neither is cheap or fast.

Who Is Absorbing the Risk

The question of who ultimately absorbs the currency and grid risk determines whether the sector continues to attract developers at all.

The honest answer is that, currently, developers are absorbing it — through longer bid preparation periods, more conservative financial models, higher tariff bids, or simply declining to bid in markets where the risk is not mitigated. The consequence is visible in tender outcomes: South Africa’s REIPPPP Round 7 received fewer bids per MW of capacity than Rounds 4 and 5, despite lower solar costs. Egypt’s second 1 GW solar tender attracted fewer international bidders than its first. Kenya’s competitive IPP process took longer to reach bid submission than initially scheduled.

Development finance institutions are aware of the problem and are responding, but slowly. The African Development Bank’s Renewable Energy Framework specifically identifies currency risk and grid connection delay as priority barriers. MIGA’s political risk guarantees can cover some forms of government-side breach, including termination of PPAs, but they do not address the commercial currency risk that is driving the most immediate project failures. The IFC’s Infrastructure Crisis Facility has been expanded, but deployment timelines at the project level remain long.

CrossBoundary Energy, one of the most active independent power producers working in African markets below the utility scale, has built its business model partly around the grid risk problem — by targeting commercial and industrial clients who can offtake power without requiring a national grid connection. The C&I model is a genuine solution for a specific segment of the market, but it does not address the utility-scale capacity additions that most national governments’ electrification plans require.

The Benchmark Problem

There is a policy dimension to the zombie project problem that is not getting sufficient attention: the use of auction clearing prices as a proxy for energy transition progress.

International climate finance bodies, development banks, and national governments routinely cite low renewable energy bid prices as evidence that Africa’s energy transition is accelerating and that climate finance is not needed at the scale previously assumed. The argument goes: if solar can compete with coal at $0.025/kWh, the transition is essentially self-financing through the market.

This argument confuses bid price with delivered capacity. A bid price is a number on a form submitted to a procurement agency. Delivered capacity is a power plant generating electricity at that price. The distance between the two — financial close, construction, commissioning — is where the zombie project problem lives. And that distance is being systematically obscured by reporting frameworks that count auction wins as energy transition progress before any steel is in the ground.

IRENA’s Africa renewable energy tracking data, which is widely cited in COP30 preparation documents, counts “awarded” capacity as a forward indicator. It does not separately track “awarded but not financially closed” capacity, which is the zombie category. If the zombie share of awarded capacity is 20–30% — a figure consistent with what developers and financiers describe, though no authoritative dataset currently exists — then Africa’s reported renewable pipeline is materially overstating its actual construction trajectory.

What Fixes It

The solutions are known, and some are in development. Currency hedging instruments for renewable PPAs — the IFC/MIGA product being developed — would directly address the largest single source of project failure. Grid queue reform — transparent, enforceable connection timelines with financial consequences for transmission companies that miss them — would address the second largest. And reporting reform — separating awarded from financially-closed capacity in all official tracking frameworks — would at least make the problem visible to the policymakers who need to act on it.

None of these are quick. The IFC currency product is 18 months into development. South Africa’s grid queue reform is iterating through multiple legislative instruments. IRENA’s data collection relies on national government reporting, which is slow to change.

What is fast is the rate at which Africa’s renewable energy auctions are producing capacity that exists only in spreadsheets. The continent has the solar resources, the falling technology costs, and the political commitments to justify a renewable energy transition at scale. What it does not yet have is the financial infrastructure to turn those commitments into electrons. Until it does, the gap between bid and build will keep widening — and the zombie projects will keep multiplying.

— Energy & Climate Tech Reporter, BETAR.africa

Related coverage: Africa Clean Energy Finance Q1 2026: DFI Shift and Commercial Bank Pullback | Africa Electricity Tariff Reform Wave 2026 | Egypt’s 1GW Solar Race