Three of West and East Africa’s largest higher education systems are simultaneously under financial strain. The consequences extend well beyond campus walls — into the talent pipelines that determine whether Africa’s digital economy ambitions are credible.

The lecture hall at the University of Ghana’s Balme Library still fills every morning. The generator outside the Faculty of Science keeps the equipment running through another dumsor window. On paper, the campus functions. Below the surface, a financial architecture that has held African public universities together for three decades is quietly buckling under the combined weight of austerity budgets, IMF fiscal targets, and governments that have learned to treat higher education as the expenditure line most easily deferred.

In Nigeria, Ghana, and Kenya — the three largest higher education systems in West and East Africa by enrolment — 2026 is a year of simultaneous financial stress. The coincidence is not accidental. It reflects a structural dynamic: as governments across the continent borrow more and service more debt, the fiscal compression that follows finds its easiest targets in the recurrent expenditure of institutions that cannot go on strike as effectively as a power utility, or default as visibly as a road contractor.

The consequences are not abstract. Africa’s technology sector, its financial services industry, and its healthcare systems all depend on a university pipeline producing graduates who can code, analyse, diagnose, and build. When that pipeline is underfunded, the shortfall does not show up immediately — it shows up five years later, in talent gaps, in accelerated brain drain, and in the EdTech and skilling sector that scrambles to patch the holes the formal system left behind.

Nigeria: The TETFUND Trap

Nigeria’s university funding structure rests on two pillars: direct federal government grants to public universities, and the Tertiary Education Trust Fund (TETFUND), a levy on private sector companies that channels infrastructure and research capital to tertiary institutions. For years, this two-pillar model masked the inadequacy of each component individually.

The federal education budget in 2025 stood at ₦3.52 trillion — approximately 7 percent of total federal spending. The African Union’s Continental Education Strategy for Africa (CESA 2016–2025) set a target of 26 percent of national budget allocation to education — a figure Nigeria has never approached. The gap between the two figures is not new; what is new is the compounding effect of inflation on the real value of allocations that have not kept pace with naira depreciation, rising utility costs, or the salary demands of an academic staff that has been negotiating through the Academic Staff Union of Universities (ASUU) for decades.

A landmark ASUU agreement reached in 2025 averted what had become a near-annual strike cycle, providing a 40 percent salary increase for university staff, a commitment to a National Research Council funded at one percent of GDP, and expanded institutional autonomy. The agreement is genuinely significant — it acknowledged, for the first time at a federal policy level, that the strike cycle was a symptom of structural underfunding, not just a labour relations failure.

What the agreement cannot resolve is the threat to TETFUND itself. Nigeria’s 2024 Tax Reform Bill proposes to redirect a portion of TETFUND’s education tax levy toward the Nigeria Education Loan Fund (NELFUND), reducing TETFUND’s income base progressively through 2030. ASUU has described this as an existential threat. TETFund disbursements per university are already modest — ₦2.52 billion per institution in 2026, up from ₦1.9 billion in 2024, but still a fraction of what each institution requires to maintain aging infrastructure and expand research capacity. Reducing that levy while leaving the grant line unchanged would remove the one capital investment mechanism that public universities have reliably accessed.

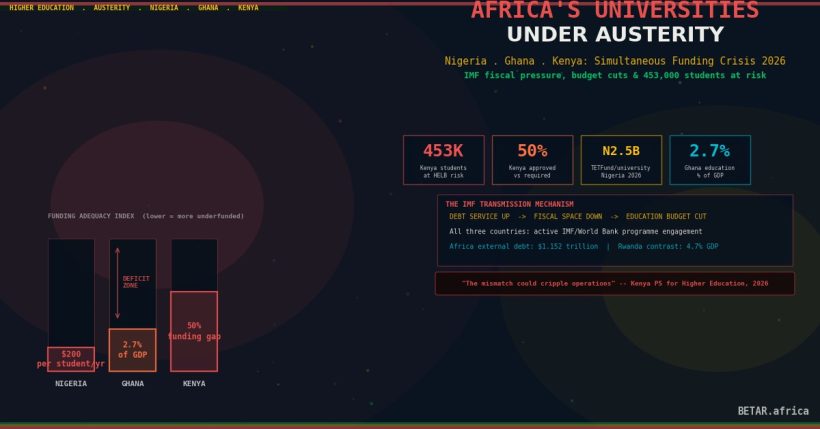

The per-student funding picture is more stark when viewed in real terms. Nigeria’s federal universities enrolled approximately 1.6 million students in 2024/25. At current allocation levels — applying education’s share of the ₦3.52 trillion federal budget, converted at Q1 2026 exchange rates and divided across enrolled students — total federal university funding amounts to less than $200 per enrolled student per year. The equivalent figure in Mauritius is more than ten times higher.

Ghana: The GETFund Reallocation Problem

Ghana’s higher education funding crisis has a specific architectural cause: the Ghana Education Trust Fund (GETFund) was never designed to finance recurrent secondary school costs, but it is increasingly being used to do exactly that.

GETFund was established to provide supplementary infrastructure financing across all education levels. In the 2026 education budget — allocated at GHS 43.2 billion, the smallest year-on-year increase since 2021 at 2.6 percent — GETFund is directing 42 percent of its total allocation toward the Free Senior High School (Free SHS) programme, covering costs that should be funded from general budget appropriations. The reallocation leaves tertiary infrastructure funding chronically undersupplied.

The 2026 education budget as a share of GDP stands at 2.7 percent — below UNESCO’s recommended 4-6 percent, and notably below Ghana’s own 2025 figure of 3.1 percent. Civil society monitoring group EduWatch has described the trajectory as a regression, noting that the combination of a below-inflation budget increase and the Free SHS reallocation of GETFund effectively reduces real investment in tertiary education for the second consecutive year.

The operational consequence for Ghana’s public universities is a fee freeze imposed by the Ghana Tertiary Education Commission, which has directed institutions to maintain 2024/25 fee structures while awaiting approval of new schedules. For universities that depend on internally generated funds — student fees paid by non-scholarship students — this freeze erodes purchasing power without any compensating increase from central government. The result is a slow deterioration in laboratory facilities, lecturer-to-student ratios, and library acquisitions that does not generate headlines but accumulates systematically over years.

Kenya: The Insolvency Threshold

Kenya’s university funding crisis is the most acute of the three, and the most precisely quantified. As of March 2025, government officials had identified 23 public universities as facing insolvency risk — a figure that reflects a structural funding shortfall that has been building since the consolidation of the university sector in the previous decade.

The State Department for Higher Education requires Sh311.9 billion for the 2026/27 financial year. Its approved allocation in the Budget Policy Statement is Sh155.2 billion — a shortfall of approximately 50 percent before the academic year begins. HELB (the Higher Education Loans Board), which provides student loans that are the primary mechanism through which students pay fees that universities then use for operating costs, faces a KSh43.6 billion funding deficit — with over 100,000 students at risk of exclusion from the loan programme as a direct result.

The scholarship programme has been cut more severely than the loan programme: against a requirement of Sh47.36 billion, the approved allocation is Sh17.92 billion — 37.8 percent of what is needed. The students who lose scholarship access are not distributed randomly across the population. They concentrate among low-income students, first-generation university entrants, and students from counties with weaker secondary school infrastructure. The austerity does not affect the university system uniformly; it narrows the access pathway precisely for those the expansion of the past decade was designed to reach.

The government’s own officials are not disputing the picture. Beatrice Inyangala, Kenya’s Principal Secretary for Higher Education and Research, told Parliament that “the mismatch between demand and allocation could cripple operations,” warning that “without adequate funding, thousands of students would be locked out of essential support.” That assessment understates the risk: it is not thousands but hundreds of thousands — HELB’s own projections place 453,000 students at risk of losing loan access if the deficit is not resolved before the 2026/27 academic year begins.

Kenya’s predicament is directly linked to IMF fiscal targets. With national debt service consuming an increasing share of government revenue, the fiscal space for social sector spending has contracted under structural adjustment conditions that are, by now, familiar to the region. The universities cannot be restructured out of crisis the way a parastatal can be privatised; they can only be underfunded more slowly or funded adequately.

The IMF-Austerity Transmission Mechanism

The coincidence of university funding crises across Nigeria, Ghana, and Kenya is not coincidental. All three countries have active engagement with the IMF and World Bank — either under formal programme conditions or under the informal fiscal signalling that multilateral creditor relationships impose. Total African external debt stands at approximately $1.152 trillion, and debt service requirements are absorbing fiscal space that a previous generation of finance ministers was able to direct toward human capital.

The research evidence on IMF conditionality and education spending is contested. Some studies find positive associations between programme engagement and education expenditure; others document consistent cuts. The operational reality in all three countries in 2026 is that education budgets have been squeezed while debt service has risen — regardless of the direction of academic causality.

What is not contested is the consequence for the skills pipeline. A university system that cannot retain its faculty, cannot maintain its laboratories, and cannot expand its enrolment capacity is not producing the graduate cohort that a digitising economy requires. The EdTech sector is building around this gap — but patching a structural failure with bootcamps and fellowship programmes is not the same as repairing the underlying system.

The Rwanda Contrast

Not every African government has made the same trade-off. Rwanda’s government expenditure on education reached approximately 4.7 percent of GDP in 2024 — consistent with the UNESCO threshold and sustained across multiple budget cycles as part of the country’s Vision 2050 human capital strategy. The University of Rwanda and the Rwanda Polytechnic have both expanded research and industry partnership programmes under a national innovation mandate that treats the university system as an economic infrastructure investment rather than a discretionary social service.

Mauritius presents a similar profile at approximately 4.6 percent of GDP, with the additional advantage of a smaller, better-resourced system that can maintain quality at scale. Neither country is analogous to Nigeria or Kenya in population size or system complexity — but the comparison is instructive. The funding shortfall in Lagos or Nairobi is not inevitable. It is a policy choice being made under external pressure and internal prioritisation failures simultaneously.

The Downstream Consequence

The headline threat — that African public universities are underfunded — is not new. What is new in 2026 is the convergence: three major systems simultaneously under acute stress, at the same moment that the demand for university-educated technology, health, and professional services graduates is accelerating rather than contracting.

The skills gap that African employers and governments repeatedly identify as a constraint on growth does not originate in a shortage of learning platforms or bootcamp providers. It originates here — in the university budget lines that have been compressed for a decade, in the laboratories that have not been upgraded, in the faculty that emigrated, in the students who enrolled but did not complete because the funding support collapsed before they graduated.

The austerity is not paying down debt fast enough to justify the trade-off. And the compound interest on a generation of underqualified graduates will be paid for longer than any IMF programme runs.

Sources: Nigeria: Ministry of Finance 2025 Budget Summary; ASUU 2025 Agreement statement (NAN, Feb 2026); TETFund 2026 disbursement schedule (Authority News, Jan 2026). Ghana: EduWatch 2026 Budget Analysis (GBC Ghana Online, Nov 2025); Ghana Tertiary Education Commission fee directive; GETFund 2026 allocation breakdown; Citi Newsroom on GETFund/Free SHS (Nov 2025). Kenya: Daily Nation Sh260bn budget hole (2025); HELB KSh43.6bn deficit report (2026); Beatrice Inyangala, Principal Secretary for Higher Education and Research, parliamentary testimony (2026); Kenya Times university insolvency risk (2025). IMF/World Bank: Oxfam “Dispiriting, dangerous, anti-development” report; AfDB African Economic Outlook 2025. Rwanda/Mauritius: Trading Economics education spending data; AfDB Rwanda Development Effectiveness Review, Nov 2024.