America’s Africa Energy Pivot: Clean Cooking and Critical Minerals Instead of Climate Finance

The 11th Powering Africa Summit made the Trump administration’s Africa energy posture explicit: commercial lending, critical minerals, and clean cooking as an investable sector. Climate finance is no longer in the vocabulary. For African governments that designed energy transition plans around US concessional commitments, this is not a rhetorical shift — it is a structural funding gap.

Chris Wright does not speak the language of his predecessor. Jennifer Granholm, Biden’s energy secretary, arrived at Powering Africa Summits with Just Energy Transition Partnership commitments and concessional finance packages for coal retirement. Wright — former CEO of Liberty Oilfield Services, a hydraulic fracturing services company — arrived in Washington for the 11th summit with EXIM Bank Chairman John Jovanovic and a “fireside chat” on energy access and clean cooking.

The contrast is not merely stylistic. The difference between those two postures represents several billion dollars in financing commitments that African governments no longer have, and a strategic shift in how the United States intends to engage with the continent’s energy sector for the remainder of this decade.

The Rebrand, Explained

Under Biden, US engagement with African energy was structured around three instruments: Power Africa grants and transaction advisory services, DFC concessional financing for clean energy projects, and the JETP — the Just Energy Transition Partnership — which committed bilateral finance packages to accelerate the retirement of coal and expansion of renewables in South Africa, Kenya, Senegal, and Indonesia.

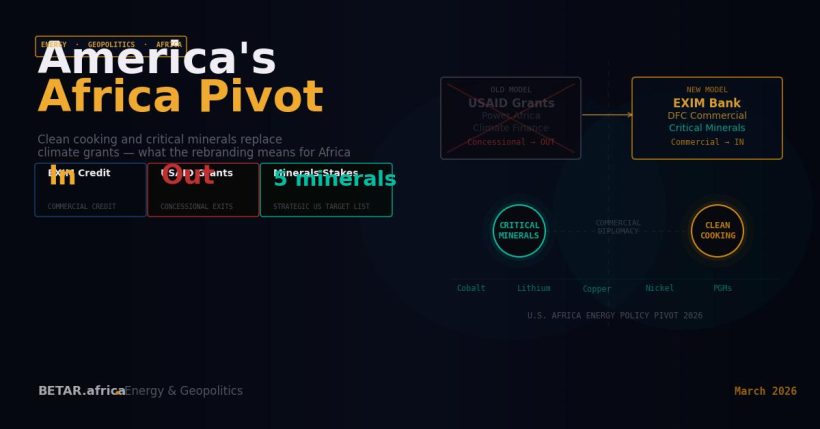

The Trump administration has not simply reduced these commitments. It has replaced the framing. The 2026 Powering Africa Summit theme — “Powering the US-Africa Partnership: Energy Infrastructure, Critical Minerals & Investment Strategies” — contains no mention of climate finance, energy transition, or development assistance. The word “investment” appears where “partnership” used to; “strategies” where “commitments” once stood.

What replaces the old model is a commercial diplomacy framework built on three pillars:

- EXIM Bank commercial credit for US-developed energy infrastructure projects in Africa — financing that requires commercial bankability and market-rate repayment, not concessional terms.

- Critical minerals bilateralism — US investment in African mining and processing infrastructure tied to supply chain security for batteries, semiconductors, and defence technologies. The DRC, Zambia, and South Africa are the priority corridors.

- Clean cooking as investment — reframing household energy access not as a development obligation but as a commercial opportunity for US private capital, with EXIM Bank as the enabling vehicle rather than USAID grants.

What Was Actually Withdrawn

The JETP withdrawal in early 2025 is the clearest measure of the gap. South Africa’s JETP, the most advanced and most monitored of the partnerships, had committed $8.5 billion in blended public and private finance — of which the US bilateral commitment represented approximately $1 billion in DFC financing and $150 million in USAID technical assistance and grant support.

Those commitments funded specific line items: technical assistance for the Integrated Resource Plan revision, capacity building for municipal utilities struggling with distributed solar integration, and concessional debt to Eskom’s Just Transition Financing (JTF) vehicle. Their withdrawal did not collapse the JETP — German, French and UK bilateral commitments remain in place — but it created a financing hole that the remaining partners have been unable to fully fill.

USAID’s broader energy portfolio was more dispersive in its impact. Across 23 sub-Saharan African countries, USAID Power Africa funded regulatory capacity building, transaction advisory for off-grid mini-grid developers, and direct grant support for clean cooking access programmes. The programmes that depended on USAID transaction advisers — particularly in francophone West Africa where regulatory capacity gaps are largest — have not found equivalent substitutes.

What African Governments Need to Recalculate

The governments most exposed to the US posture shift are those that integrated US concessional finance assumptions directly into their energy transition planning documents. Kenya is the clearest case. Kenya’s Nationally Determined Contribution revision, submitted in 2024, included financing assumptions for clean grid expansion that were partly premised on continued JETP-framework support. The clean grid paradox — Kenya has the cleanest electricity system in sub-Saharan Africa but some of the most expensive retail tariffs — is in part a financing cost problem. Concessional finance at below-market rates was supposed to reduce the debt-service cost embedded in generation tariffs. Commercial rates do not solve that.

Nigeria faces a different but related problem. DARES — the Distributed Access through Renewable Energy Scale-up programme — secured a $750 million World Bank financing package in 2025 to deploy mini-grids and solar home systems to 17.5 million Nigerians without grid access. DARES is not JETP; it is a World Bank instrument, not a US bilateral commitment. But the broader ecosystem of technical assistance, mini-grid regulatory support, and clean cooking access programming that USAID Power Africa provided in Nigeria is being wound down. DARES can deploy hardware; it cannot replace the policy environment support that created the conditions for mini-grid investment.

Is Commercial Finance Enough?

The honest answer is: for some projects, yes. For the energy transition at scale, no.

Commercial finance — EXIM Bank credit, DFC equity, private infrastructure funds — works well for projects that are commercially bankable: utility-scale solar with power purchase agreements from creditworthy offtakers, gas-to-power projects with long-term contracts, grid infrastructure serving industrial consumers. Sun Africa’s 500MW Liberia MOU, announced at the summit, is an example of the kind of project that might access commercial finance — assuming DFC is willing to provide the risk guarantee that makes Liberia’s sovereign credit acceptable to commercial lenders.

It does not work for last-mile electrification. Rural mini-grids serving communities where average monthly electricity consumption is 10–30 kWh are not commercially bankable at market interest rates. Clean cooking programmes reaching households spending $2–3 per day on charcoal cannot service commercial debt. Regulatory capacity building for under-resourced national energy regulators is not a revenue-generating activity. These are precisely the interventions where concessional grant finance is irreplaceable — and where the US withdrawal is felt most acutely.

The IEA’s Africa Energy Outlook estimates that reaching universal energy access by 2030 requires $25 billion per year in annual investment — roughly six times current levels. Of that, approximately $6 billion per year needs to flow to off-grid and last-mile solutions that will never be commercially bankable without subsidy. EXIM Bank’s total Africa energy lending across its history barely exceeds that single-year figure.

The Critical Minerals Trade-Off

The clearest window into the Trump administration’s actual strategic calculus is the critical minerals framing. EXIM Bank has announced a Critical Minerals Initiative specifically targeting African processing and extraction. DFC has indicated that strategic minerals investments — cobalt in the DRC, copper in Zambia, manganese in South Africa — will receive priority consideration.

This is not inherently bad for Africa. The continent holds 30–40% of global critical mineral reserves and has historically exported raw ore rather than processed materials, capturing a small fraction of the value chain. If US commercial finance helps build beneficiation capacity — processing cobalt into battery-grade materials in Kinshasa rather than in China — the development returns are real.

But the terms matter. EXIM Bank critical minerals financing is structured to secure US supply chain access — the finance serves US industrial policy first. Whether it also serves African industrial development depends on the bilateral agreements governing local content, processing requirements, and revenue sharing. African governments entering these negotiations without comparable technical advisory support to what USAID once provided are negotiating at a significant information disadvantage.

What to Watch at COP30

Belém in November 2026 will be the first COP where the new US posture is formally on display within multilateral climate finance negotiations. The New Collective Quantified Goal — the successor to the $100 billion climate finance commitment — was agreed at COP29 in Baku at $300 billion per year. The US was part of that agreement under Biden. Whether the Trump administration honours that commitment, restructures it around commercial finance, or withdraws entirely will define the COP30 narrative.

For African negotiators, the Powering Africa Summit’s commercial-first language is the clearest preview of what is coming. The argument that EXIM Bank and DFC represent a meaningful US climate finance contribution — just restructured around commercial terms — will be made in Belém. African delegations need to have the analytical framework to evaluate that argument clearly: what the commercial-concessional substitution actually costs at project level, which gaps it fills and which it does not, and what the implications are for NDC implementation timelines that were designed with different financing assumptions.

America is still engaged in Africa’s energy sector. The question is no longer whether the US is present — it is what the US presence actually delivers, and for whom.

— Energy & Climate Tech Reporter, BETAR.africa