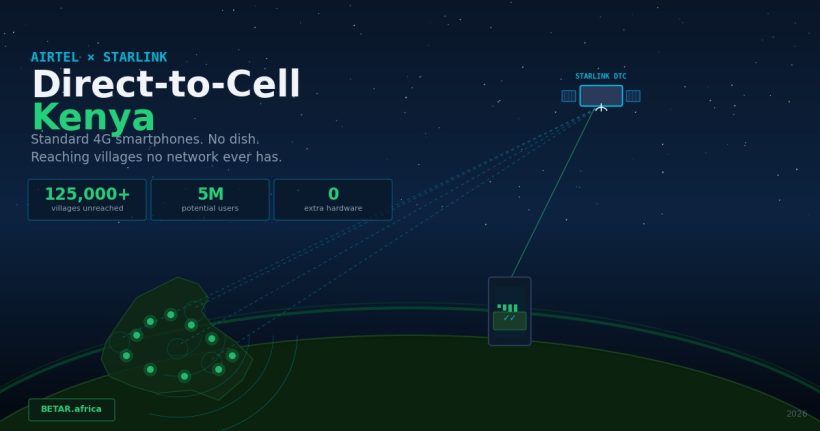

A standard 4G smartphone. No satellite dish. No additional hardware. WhatsApp messages delivered, mobile money transactions cleared — in a village that no Kenyan network has ever reached.

That is what Airtel Kenya and SpaceX’s Starlink demonstrated in a March 2026 pilot confirmation that carries consequences for every operator, regulator, and tower company on the continent. Direct-to-cell (DTC) connectivity — satellite signals beamed directly to ordinary handsets — has moved from engineering specification to operational reality in East Africa.

The question is no longer whether it works. The question is whether Africa’s regulatory and competitive infrastructure can absorb what it does to the economics of connectivity.

How it happened

The partnership was formalised in December 2025, when Airtel Africa and SpaceX signed a roaming agreement to trial Starlink’s Generation 2 satellites — the variant specifically engineered for direct device communication — on Airtel’s Kenyan subscriber base. The pilot phase, confirmed in late March 2026, targeted coverage-black zones: agricultural communities in the Rift Valley and coastal fishing settlements where Airtel, Safaricom, and Telkom have no physical infrastructure.

What was tested was deliberately constrained: Phase 1 covers text messaging and basic data. Full voice and SMS integration is planned for 2027–2028, pending regulatory approval. But the constraint understates the significance. In communities where mobile money is the banking system, and where WhatsApp is the supply chain communication layer for smallholder farmers and fishing cooperatives, text and data is not a limited service. It is infrastructure.

The test data cited in Airtel’s pilot documentation indicates throughput sufficient for standard messaging applications and low-bandwidth financial transactions. Latency figures remained within acceptable parameters for mobile money processing — the most commercially meaningful benchmark for East African rural users.

Why this is different from everything that came before

The history of satellite connectivity in Africa is a history of the cost problem. VSAT required hardware installations costing hundreds of dollars. Early LEO services like Starlink Standard required dish purchases at $350–$600 and monthly fees that positioned satellite internet as a business service, not a consumer one. The unconnected remained unconnected.

DTC dissolves the tower economics equation at its root. A tower serving a 60km² rural catchment requires $80,000–$150,000 in capital expenditure, annual maintenance, grid power or diesel logistics, and a subscriber density that makes unit economics viable. In Kenya, approximately 8 million people — roughly 15% of the population — live outside any network’s coverage footprint. For operators, building to reach them has never been financially rational.

With DTC, the device is already in the user’s pocket. Smartphone penetration in rural Kenya has reached 54% and continues to grow, driven by device financing schemes and sub-$100 entry-level 4G handsets. No new hardware is required. The marginal cost of connecting the unconnected, from an infrastructure perspective, is the satellite constellation — which Starlink has already built and continues to expand.

The arithmetic for 200 million unconnected Africans — the ITU’s 2025 estimate for the population living outside any broadband coverage — looks different under this model than it did twelve months ago.

The interference problem and the 14-regulator obstacle

The Kenya pilot has triggered exactly the regulatory response that operators anticipated. In March 2026, the Communications Authority of Kenya (CA-Kenya) initiated a review of the DTC spectrum configuration, setting a mid-2026 audit deadline. The central concern is interference: Starlink’s DTC signals operate in spectrum bands that overlap with existing cellular allocations, and at scale, the interference risk to existing network performance requires documentation and mitigation before commercial authorisation.

CA-Kenya’s review is not an attempt to block DTC. The CA’s public statement frames the review as a technical standards exercise, and Airtel’s position is that the interference risk is manageable with coordination protocols already established in the FCC’s DTC approval framework for the US market.

But Kenya is one market. A continent-wide DTC rollout — which is the commercial logic of the Airtel Africa partnership, not just a Kenya experiment — requires separate regulatory approvals in every jurisdiction: Nigeria’s NCC, South Africa’s ICASA, Ghana’s NCA, Tanzania’s TCRA, and at least ten others. Each has its own spectrum allocation, licensing framework, and political economy around foreign satellite operators.

The 14-regulator problem is not unique to DTC. It has limited every pan-African digital infrastructure play from mobile money interoperability to cross-border data flows. Airtel Africa’s 14-market footprint is an asset here — it provides the regulatory relationships and local licensing infrastructure that an operator without African presence could not deploy. But the timeline to continent-scale commercial DTC service is measured in years, not months.

The competitive map: who gains, who absorbs the pressure

The competitive implications are not uniform.

MTN’s fixed wireless access (FWA) play — 30 million connected homes by 2028, anchored in urban and peri-urban markets — targets a different geography and demographic than DTC’s rural coverage mandate. MTN FWA requires router hardware and addresses existing buildings in areas with network coverage. DTC targets the uncovered. These are complementary infrastructure layers, not direct competition.

Safaricom’s position is more complex. In urban and peri-urban Kenya, where M-PESA penetration creates profound switching costs — financial history, merchant relationships, business payment rails — Safaricom’s network advantage is durable. DTC does not change the M-PESA moat in Nairobi or Kisumu.

In rural Kenya, however, the dynamic is different. Safaricom has extended M-PESA into communities where it holds the only network connection, creating a first-mover advantage that DTC can, over time, contest. A rural farmer in Marsabit or West Pokot who currently uses M-PESA because it is the only service available may, within a DTC commercial rollout window, have an Airtel SIM that works without a tower. The subscriber acquisition math for Safaricom’s rural expansion changes.

The tower company sector faces the most structural question. IHS Towers and SBA Communications have built portfolios on the assumption that tower density is the non-negotiable infrastructure layer for African connectivity. DTC does not eliminate towers — voice traffic and high-bandwidth applications will require tower infrastructure for years — but it removes the coverage-floor argument for tower expansion in the lowest-density catchments. Capital allocation for tower buildout in rural Africa will face new scrutiny.

The 48-hour window that matters

Technology journalism has a coverage-window problem: connectivity announcements generate straight news coverage, and then the structural analysis arrives late or not at all. TechCabal and Techpoint both covered the March 26 pilot confirmation. Neither addressed the regulatory risk, the competitive implications for Safaricom and tower companies, or the device-penetration arithmetic that makes this moment different from previous satellite connectivity announcements.

What Airtel and Starlink have demonstrated is not merely a new product. It is a challenge to the tower-density model that has structured African connectivity investment for thirty years. The outcome will be determined by regulators, device economics, and competitive response — not by the pilot test results alone.

The CA-Kenya review will produce a decision by mid-2026. That decision will signal whether Kenya intends to be the first African market to authorise commercial DTC at scale. If it does, the precedent pressure on other regulators will be substantial.

BETAR.africa sought comment from Airtel Africa on the Kenya pilot results and commercial rollout timeline. A response was not received by publication time. The CA-Kenya review initiation is confirmed on public record.