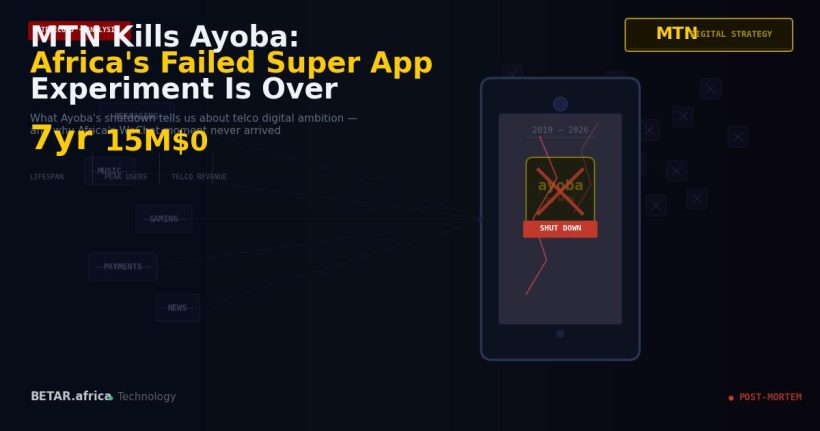

On March 20, MTN removed Ayoba from app stores and began a 30-day wind-down of the messaging and entertainment platform it launched in 2019 with ambitions to become Africa’s WeChat. Monthly active users on a zero-rated messaging app had reached a widely cited 2022 figure of approximately 35 million — “a figure widely cited in reporting on Ayoba’s 2022 growth milestone,” as MTN’s own communications framed its traction. By 2026, Ayoba was gone.

The shutdown is not primarily a product story. It is a capital allocation argument — and it says something specific about the strategic error that African telcos have been repeating for a decade.

What Ayoba tried to do

MTN launched Ayoba as a super app — a single platform combining messaging, music streaming, mobile games, news, and payment features, distributed with a critical advantage: zero-rated data on MTN networks. Users could access Ayoba without consuming their data bundles. This was the distribution strategy: make the product free to access in markets where data costs are a genuine barrier to digital engagement.

The model had a structural problem that zero-rating could not solve. Zero-rated data creates engagement, but engagement on a zero-rated service is not the same as willingness to pay. Ayoba’s user base was concentrated in MTN’s most price-sensitive markets — users who adopted Ayoba because it was free, not because it was better than WhatsApp, TikTok, or YouTube. Converting that user base to a monetised product required competing on product quality against platforms backed by Meta’s engineering budget and Google’s content library. MTN was not equipped for that competition.

WhatsApp’s network effects in Africa are structural, not contingent. In Nigeria, Ghana, South Africa, and Kenya, WhatsApp is the communications infrastructure for informal commerce, family communication, and professional coordination. An alternative messenger requires not just adoption by individual users but simultaneous migration by entire social and business networks. That transition cost is prohibitive regardless of how much data the alternative saves.

MTN’s revised digital strategy

MTN’s own explanation for the shutdown frames it as a consolidation, not a retreat. In an official statement, MTN said it is “building a unified digital platform” that integrates its digital services — MoMo, its fintech layer, FWA broadband, and content partnerships — rather than maintaining separate consumer apps.

That framing is consistent with where MTN’s digital investment has actually been generating returns. MoMo, MTN’s mobile money platform, processed $280 billion in transaction value in FY2025 — a scale that makes it one of the continent’s most significant financial infrastructure players. MoMo’s value is network effects in payments, not entertainment or messaging. It is a fundamentally different product economics model from a super app.

MTN’s FWA (fixed wireless access) push — targeting 30 million connected homes by 2028 — is similarly infrastructure-oriented. It monetises MTN’s spectrum and network assets by extending connectivity into residential broadband, with predictable subscription economics and a market largely free from the app-level competition that killed Ayoba.

The implicit capital allocation logic is becoming clear: MTN’s shareholder value comes from being infrastructure, not from competing with consumer internet companies at their own game.

The telco digital strategy question

Ayoba’s failure joins a long list of telco super-app experiments that have not survived contact with network-effect reality. Orange launched Djingo in francophone Africa; Vodacom has periodically pursued content bundling strategies; MTN’s own previous digital investments — the MCN acquisition, various content platforms — followed a similar pattern of investment followed by rationalisation.

The pattern reveals a structural tension in African telco digital strategy. Telcos have three genuine competitive advantages: network infrastructure, subscriber relationships at scale, and existing billing relationships with hundreds of millions of customers. They have one genuine digital product success: mobile money, which exploits all three advantages simultaneously and operates in a domain — payments — where WhatsApp and TikTok are not natural competitors.

The comparison is instructive. Safaricom’s M-PESA super app ambitions are better grounded than MTN’s Ayoba was, because M-PESA is building on top of an existing financial infrastructure layer that processes a third of Kenya’s GDP. The app is the interface; the infrastructure is the moat. Airtel Money and Orange Money are following the same logic.

Ayoba was attempting to build the infrastructure layer — the user base and engagement — from the app down. The direction was wrong. Infrastructure is not built with a messaging app; it is built with spectrum, towers, and billing rails.

The read for the ecosystem

MTN’s decision to kill Ayoba and concentrate its digital investment in MoMo and FWA is the right strategic call, made several years later than the evidence justified. The company’s FY2025 results — with Nigeria becoming its largest revenue market and MoMo approaching break-even in multiple markets — validate the infrastructure thesis.

For the broader ecosystem, the Ayoba lesson is about capital efficiency in a market where distribution advantages (zero-rating, subscriber relationships) are real but not sufficient to overcome product-market-fit deficits at scale. African telcos are genuinely positioned to win in payments, connectivity, and the infrastructure layer. The consumer entertainment market belongs to the consumer internet platforms.

MTN, to its credit, appears to have arrived at this conclusion. That the conclusion took seven years and a fully built super app to reach is the cost of learning it the expensive way.

MTN said in an official statement that it is “building a unified digital platform” consolidating its digital services, describing the Ayoba wind-down as part of this strategic reorganisation.