The For-Profit School Trap

Why private equity keeps betting on African education and losing

By the Education Reporter, BETAR.africa | April 2026

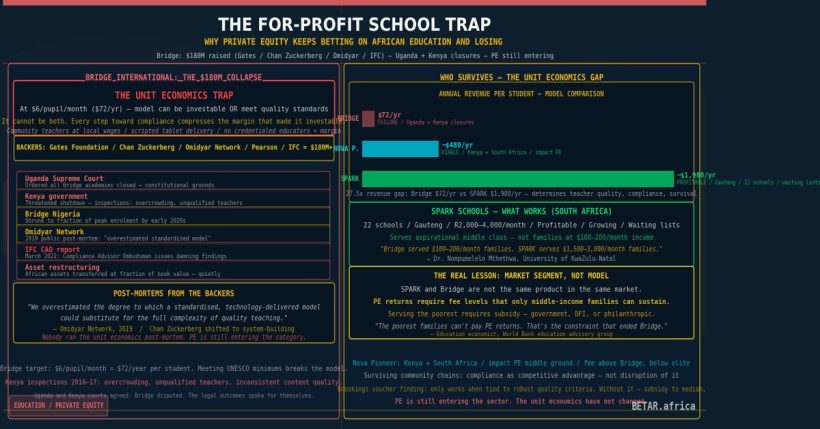

Bridge International Academies raised $180 million from the most credentialed roster of backers in the history of African education. The Gates Foundation invested. The Chan Zuckerberg Initiative invested. Omidyar Network, Pearson, and the IFC all put in capital. The company’s pitch was simple and compelling: deliver scripted, tablet-driven primary school instruction to low-income families across Africa and South Asia at $5–7 per pupil per month, turning one of the world’s most intractable development problems into a scalable, investable business.

By 2019, the Uganda Supreme Court had ordered Bridge’s academies closed on constitutional grounds. Kenya’s government had threatened shutdown over quality standards. Bridge Nigeria had shrunk to a fraction of its peak enrolment. By the early 2020s, the African assets were quietly transferred and restructured at a fraction of book value. Nobody ran the unit economics post-mortem.

Meanwhile, private equity is still entering the category.

The Business Model That Could Not Scale Quality

The Bridge International model was elegant in theory. Centralise curriculum into tablet-delivered scripts. Hire community teachers at local wage rates — not credentialed educators — and pay them to deliver those scripts precisely. Push costs below the threshold where government schools operated. Achieve margin on volume.

The unit economics were not a secret. At $6 per pupil per month, Bridge’s target revenue per student per year was roughly $72. Staff, facilities, and tablet amortisation had to fit underneath that. Every incremental investment in teacher quality, facility improvement, or curriculum depth that moved Bridge toward government quality standards directly compressed the margin that made the model investable.

That was the trap. Government quality standards in Uganda and Kenya were not arbitrary. The UNESCO minimum standards for teacher qualification, for classroom pupil-to-teacher ratios, for physical infrastructure — meeting them cost more than the model’s price point would sustain without outside subsidy. Bridge could be a viable investment or a school that met government quality requirements. It could not be both at $6 per month.

The Kenya government’s inspection reports from 2016 and 2017 documented precisely this tension: classrooms overcrowded, teachers without recognised qualifications, content quality inconsistent. Bridge disputed the findings. The legal outcomes in Uganda spoke for themselves.

Omidyar Network, one of Bridge’s earliest and most visible backers, published a public post-mortem in 2019 acknowledging that the investment thesis had not been borne out. “We overestimated the degree to which a standardised, technology-delivered model could substitute for the full complexity of quality teaching,” the Network noted in its learning documentation. Chan Zuckerberg took a similar posture, shifting its Africa education focus away from physical school chains toward broader system-building.

Why SPARK Works in Johannesburg

Three thousand kilometres south of Kampala, SPARK Schools operates 22 schools across Gauteng at monthly fees of R2,000–4,000 per learner — approximately $110–220 at current exchange rates, 20 to 30 times Bridge’s price point. SPARK is profitable. It is growing. It recently secured follow-on investment. Its waiting lists in Johannesburg’s northern suburbs are long.

The two models are in the same category — private, technology-enhanced, investor-backed — but they serve entirely different markets and operate under completely different unit economics.

SPARK targets South Africa’s aspirational middle class: families who can afford private school but not the R15,000–20,000 per month fees of the elite independent sector. At R2,000–4,000, SPARK is positioned to take share from underperforming government schools in middle-income suburbs while offering a technology-forward pedagogy — blended learning models, adaptive digital content — that appeals to parents who associate technology with quality.

“The misconception is that low-cost private schooling is a single market,” says Dr. Nompumelelo Mthethwa, an education economist at the University of KwaZulu-Natal who has tracked private school investment in sub-Saharan Africa since 2014. “Bridge was trying to serve families earning $100–200 per month. SPARK is serving families earning $1,500–3,000 per month. Those are not the same product, and they are not the same risk profile for investors.”

The revenue per pupil per year difference — $72 for Bridge versus $1,320–2,640 for SPARK — determines everything downstream: teacher qualifications, facility quality, admin capacity, and ultimately whether the model can survive government scrutiny.

Nova Pioneer and the Impact PE Middle Ground

Nova Pioneer occupies the intermediate position. Founded in 2013 with backing from Omidyar Network and other impact-oriented investors, Nova Pioneer operates K–12 schools in South Africa and Kenya at fee points significantly above Bridge but below South Africa’s elite independent sector.

The company does not publish audited financials publicly, but its impact reports document consistent enrolment growth across both markets, with the 2024 report indicating continued school network expansion. The model is less about scalable low-cost delivery and more about demonstrating that an African-origin, technology-integrated school chain can operate at quality levels competitive with established independent schools at a more accessible price point.

Nova Pioneer’s investor thesis — impact PE rather than pure commercial PE — accepts a longer path to return in exchange for the credibility of a genuine quality outcome. That distinction matters because it acknowledges implicitly what Bridge’s commercial PE backers could not: that quality African K–12 education, delivered at meaningful scale, requires a fee structure that most African families cannot afford.

The DFI Underwriting Question

The International Finance Corporation and the African Development Bank both maintain active private education lending portfolios. IFC has financed private schools across sub-Saharan Africa through its health and education practice. AfDB’s development finance for education increasingly flows toward private institutions, particularly in technical and vocational training.

The underwriting criteria tell a story. DFIs assess private education investments against social impact metrics — enrolment, learning outcomes, gender parity — alongside financial return criteria. Bridge International appeared to pass initial DFI screens because it was reaching low-income learners at scale. The quality and regulatory compliance dimensions were underweighted in the early investment models.

Post-Bridge, there is evidence that DFI education underwriting frameworks have become more sophisticated. IFC’s updated private education sector standards, issued in 2023, include explicit minimum requirements for teacher qualifications and government regulatory compliance as threshold conditions — not just impact additionalities. The Bridge post-mortem has shaped the DFI approach to private school investment even if it has not eliminated the category.

What the Pattern Says

The pattern across Bridge, SPARK, Nova Pioneer, and Omega Schools in Ghana is consistent: private equity investment in African K–12 education is viable, but only at price points that put it out of reach for the majority of African families. Omega Schools pioneered a daily-fee model in Ghana — $0.50 per day, targeting families who could not commit to monthly tuition — and expanded to over 40 schools at its peak before consolidating sharply. The trajectory mirrors Bridge’s structural problem: reaching the lowest-income families requires a price point that cannot sustain quality without subsidy.

Bridge tried to break that constraint by industrialising pedagogy below the quality threshold. SPARK accepted the constraint and targeted the market that could afford quality. Nova Pioneer is testing whether impact-oriented capital can sustain quality at a moderate fee premium without ever reaching the volume that makes the unit economics work for commercial PE.

The investment category is not going away. CESA 2026–2035 explicitly invites private sector partnership in education delivery, and domestic PE in markets like South Africa, Kenya, and Ghana is increasingly looking at education as an infrastructure play. But the evidence from two decades of for-profit school investment in Africa is clear: private equity returns in African K–12 education require fee structures that exclude the majority. The $180 million spent trying to prove otherwise has produced the most well-documented unit economics lesson in the sector’s history.

Private equity will keep entering African education. The next cycle — from domestic PE, DFIs, or impact funds — succeeds only if it prices in what Bridge proved: that quality schooling for most African families cannot be made commercially viable without subsidy or structural government partnership. The $180 million lesson is available for anyone willing to read it.