Africa Offshore Wind: Zero Commissioned Capacity Despite 100GW Announced Projects

BETAR.africa | 7 April 2026

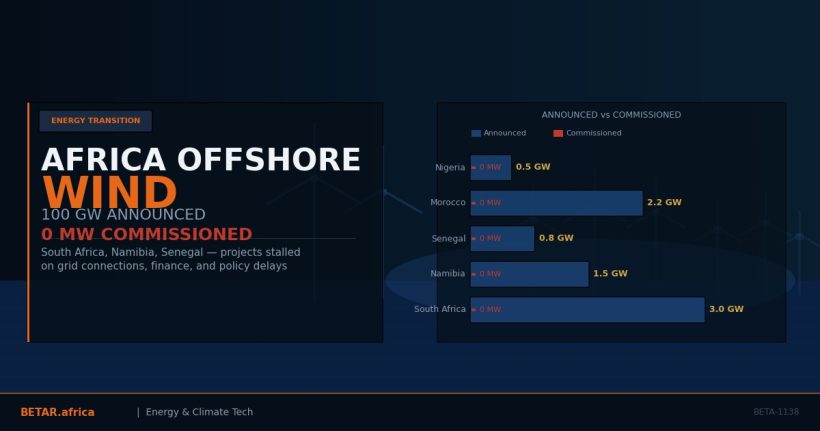

The numbers are arresting. Africa’s Atlantic and Indian Ocean coastlines carry enough offshore wind potential to power the entire continent multiple times over. Government-backed programmes in South Africa, Morocco, Egypt and Senegal have collectively announced more than 100 gigawatts of offshore wind projects. International developers — Mainstream Renewable Power, TotalEnergies, Equinor, Lekela — have run surveys, issued press releases and submitted project proposals.

Commissioned capacity: zero megawatts.

Not a single offshore wind turbine spins commercially on the African continent. While Europe installs roughly 3–4 GW of offshore capacity per year and China commissioned more than 15 GW in 2023 alone, Africa has not generated a single kilowatt-hour from offshore wind. The gap between announcement and reality is not a pipeline delay — it is a structural failure that reveals how energy ambition without regulatory, financial, and infrastructure scaffolding produces nothing but paper projects.

The Pipeline Illusion

Energy consultancies tracking Africa’s renewable pipeline routinely flag offshore wind as the continent’s highest-potential untapped resource. The South African Wind Energy Association estimates South Africa alone has over 2,000 km of viable coastline. Morocco’s Atlantic coast is classified among the best offshore wind resources globally. Egypt’s Mediterranean and Red Sea zones have attracted early-stage developer interest from major European utilities.

Yet of the 100GW+ of announced capacity across the continent, credible industry estimates suggest no more than 5–8% of projects are genuinely development-ready — meaning environmental impact assessments are underway, grid connection studies commissioned, and off-take frameworks at least partially defined. The rest exist as feasibility studies, MoU announcements, or regulatory filings that have not advanced in three or more years.

Africa receives less than 0.5% of global offshore wind investment, against roughly 3% of global onshore wind investment and 4% of solar PV investment. The offshore undershoot is not explained by resource quality. It is explained by risk.

South Africa: The Most Advanced Case Is Still Stuck

South Africa’s Renewable Energy Offshore Wind Development Programme (ROWDP) is widely considered the continent’s most structurally advanced offshore framework. The Department of Mineral Resources and Energy launched ROWDP in 2021, with NERSA (the National Energy Regulator) subsequently developing technical specifications. Two offshore wind zones — the West Coast Zone off Saldanha Bay and the East Coast Zone off Richards Bay — were identified, and a spatial planning process completed in 2023.

A Request for Proposals for the first round of ROWDP bidding was expected in 2024. It has not materialised. The core problem: Eskom’s grid connection capacity in both zones is severely constrained. The Saldanha zone would require an estimated R8–12 billion ($420–630 million) in transmission infrastructure upgrades before a single offshore wind project could connect. NERSA has not approved cost-of-connection terms, developers cannot bankfin projects without knowing their transmission cost, and the ROWDP tender remains in indefinite pre-launch status.

South Africa’s experience illustrates the structural sequence problem: offshore wind requires enormous upfront capital for subsea cable landing infrastructure, onshore substations, and grid reinforcement — costs that precede revenue generation by five to seven years. Without a functioning grid connection framework and credit-worthy off-take agreements, no developer can assemble project finance at acceptable returns.

The Xlinks Lesson

No African offshore wind story generated more international attention than Xlinks, the UK-Morocco Power Project — a proposal to build 10.5 GW of combined offshore wind and solar capacity in Morocco’s Guelmim-Oued Noun region and export power via a 3,800 km HVDC undersea cable directly to the UK grid.

At its peak, Xlinks attracted investment commitments from Octopus Energy, National Grid Ventures, and Intercontinental Energy. The project promised to demonstrate that Africa’s renewable surplus could become a genuinely tradeable commodity — the foundation for a continent-wide clean energy export model.

In 2024, Xlinks quietly shelved its timeline. The economics had shifted: UK electricity import policy became less certain post-Brexit energy negotiations, the $16–20 billion cable cost was increasingly difficult to structure without sovereign guarantees from both the UK and Moroccan governments, and Moroccan domestic power demand growth raised questions about how much exportable surplus Morocco would actually have by the mid-2030s. Xlinks remains alive as a concept. It is no longer a near-term project.

The Xlinks trajectory is instructive not because the project failed, but because it demonstrated the conditions required for African offshore wind to work at scale: sovereign-level off-take certainty, DFI first-loss capital tranches, cross-border regulatory harmonisation, and a willing anchor buyer with political commitment over multi-decade horizons. These conditions are rare.

The LCOE Problem

Africa’s energy economics present offshore wind with a structural disadvantage that does not exist in Europe or East Asia. On the continent’s most attractive development zones, utility-scale onshore solar now prices at $25–35 per megawatt-hour — among the lowest generation costs globally. Battery energy storage systems (BESS), while still expensive, are falling rapidly, addressing the intermittency gap that once made offshore wind’s near-constant generation a genuine differentiator.

Offshore wind in African conditions — deeper waters, less mature supply chains, higher political risk premia — prices at $80–120/MWh for first-of-kind projects. The premium over solar is 2.5–4x, not marginal. For energy ministers trying to hit affordability targets and reduce electricity tariff pressure, solar-plus-storage is an obvious first choice. Offshore wind becomes attractive only at national scale, when grid diversity value — preventing solar generation cliffs at sunset — justifies the cost premium.

No African market has yet reached the grid penetration levels at which offshore wind’s generation profile becomes economically valuable enough to justify the LCOE differential. South Africa, at roughly 6–8% solar penetration on its national grid, is the closest. It is not there yet.

Infrastructure That Does Not Exist

Europe built offshore wind on three decades of accumulated port infrastructure: jack-up vessels capable of operating in 40–60 metre water depths, blade assembly facilities, subsea cable installation fleets, and offshore maintenance capabilities. Africa has none of this.

The absence is not an argument against African offshore wind — it is an investment sequencing problem. Saldanha Bay in South Africa and Tanger Med in Morocco have the deep-water port infrastructure that could theoretically host offshore wind construction logistics. But no African port has yet configured for offshore wind heavy-lift operations, and no vessel owner has committed a jack-up fleet to the continent without signed, financed project contracts to justify the mobilisation cost.

The supply chain chicken-and-egg problem is one reason DFI financing matters disproportionately for first-mover projects. The AfDB, IFC, and European Development Finance Institutions have the balance sheet to absorb first-of-kind infrastructure risk that commercial lenders cannot. To date, none has committed to an African offshore wind project — in part because no project has cleared the regulatory and grid-connection preconditions required for bankability assessment to begin.

What Would Change the Picture

Three shifts could materialise African offshore wind capacity in the 2027–2032 window. First, South Africa completing ROWDP Round 1 with signed transmission agreements and a viable cost-of-connection framework — even a single 300–500MW project would establish pricing reference points for the continent. Second, a DFI-anchored risk facility specifically targeting African offshore wind development costs — covering early-stage environmental impact assessment, grid studies, and project development finance before commercial debt markets can engage. Third, Morocco’s ongoing offshore tender programme, which the Moroccan Agency for Sustainable Energy (MASEN) has been advancing with French and Spanish developer interest, producing a signed power purchase agreement with a financed project.

Without at least one of these, the 100GW announced pipeline remains exactly what it is today: a measure of ambition, not a measure of progress.

The Gap Is Not Inevitable

Africa’s offshore wind impasse is real, but it should not be misread as evidence that the resource is inaccessible. The barriers are regulatory, financial, and logistical — all of them solvable with sufficient policy commitment and capital alignment. The challenge is sequencing: offshore wind requires grid investment before project investment, and project investment before supply chain investment. In a continent where capital is scarce and energy ministers are managing short-term tariff crises, the long-horizon logic of offshore wind competes poorly.

The 100GW announcement figure will likely continue to grow. The commissioned megawatt count will remain at zero until at least one government resolves the sequence — builds the grid connection, secures the DFI anchor, and accepts the above-solar cost premium as a long-run grid stability investment. The first country to do that will establish the African offshore wind market. Everyone else is waiting for someone else to go first.

BETAR.africa covers clean energy investment, climate tech, and the economics of Africa’s energy transition. For more analysis, see our coverage of Africa’s BESS deployment landscape, Kenya’s clean grid paradox, and the AfDB Mission 300 two-year review.