Nigeria Fintech M&A Pipeline Q2 2026: Who Is Buying the Compliance Laggards?

By BETAR.africa Business Desk | 22 April 2026

The Central Bank of Nigeria’s compliance window has closed. An estimated 40 to 60 tier-two and tier-three fintechs — digital lenders, USSD-native microfinance banks, undercapitalised payment service providers — cannot meet the four-mandate stack and cannot sustain operations without resolving that gap. The question for Q2 2026 is not whether consolidation happens. It is who has the capital, the CBN goodwill, and the strategic logic to be the acquirer — and who will be acquired.

BETAR.africa analysis of the post-compliance operator landscape, combined with published CBN licensing data, Q1 2026 deal disclosures, and conversations with Lagos-based M&A advisers, identifies a credible acquirer short list, a structured target pool, and three deal pairs worth watching before the end of June.

The Acquirer Short List

The compliance wave did not leave all survivors in an equally acquisitive posture. Capital position, CBN standing, and strategic product logic define who can realistically move.

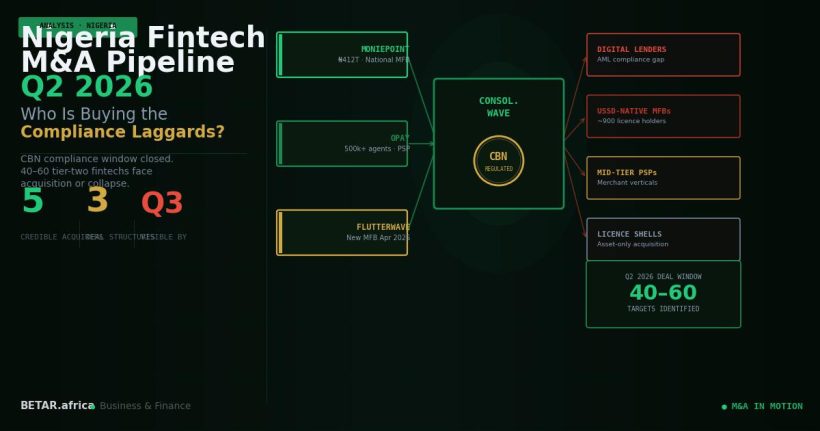

Moniepoint is the most acquisition-ready actor in the market. The company processed ₦412 trillion in transaction value in 2025, holds a national MFB licence — requiring N5 billion minimum paid-up capital — and has already demonstrated cross-border M&A execution via its 78% acquisition of Sumac Microfinance Bank in Kenya. Domestically, Moniepoint’s merchant focus creates a direct strategic rationale for acquiring compliance-capable lenders or identity infrastructure providers that extend its merchant credit and KYC stack. It has the balance sheet, the CBN relationship, and the precedent.

The Stack Group — the holding structure encompassing Paystack and Paystack Microfinance Bank — enters Q2 with a newly issued MFB licence and a stated product roadmap built around merchant working capital and BaaS. Paystack’s January 2026 acquisition of Ladder MFB established the group’s willingness to use acquisition as a licensing mechanism. A second acquisition — this time to extend geographic reach or product capability rather than just to resolve a licence gap — is structurally consistent with Stripe’s global playbook for its Nigerian unit.

OPay operates Nigeria’s largest agent banking network, with over 500,000 points concentrated in informal retail and transportation. Its acquisition thesis is volume-driven: adding customer accounts or merchant accounts at marginal cost through an acquisition is more capital-efficient than building out the equivalent organically. OPay’s exposure remains on the virtual asset side — it has been executing a structural clean-up of its crypto-adjacent product history since late 2025 — but its compliance position for core payments is strong.

PalmPay carries a nuance that the others do not: its Transsion Holdings and Chinese institutional funding base generates enhanced CBN scrutiny on beneficial ownership and cross-border capital flows. The company completed its AI/AML deployment ahead of the June deadline and has resolved the majority of its VARA-adjacent questions. PalmPay is acquisitive in principle — its access to non-equity capital from its parent group is a genuine structural advantage — but CBN approval timelines on a PalmPay-led deal are likely to be longer than for domestic-capital acquirers.

Flutterwave is the newest entrant to the MFB tier, having received CBN approval for a microfinance banking licence in early April 2026. As BETAR reported, the primary driver was settlement independence following the 2022 Access Bank freeze episode. Flutterwave enters Q2 with a freshly activated MFB and a product team now authorised to design lending and deposit products for the first time. An acquisition at this stage would likely be additive to its identity and KYC infrastructure rather than balance-sheet-driven.

The Target Pool

Against those five acquirers, three categories of consolidation candidates have become structurally defined by the compliance architecture.

The first category is digital lenders. Nigeria’s licensed digital lending sector includes dozens of operators whose core product — short-term consumer credit, often at high APRs — was built before the AI-based AML and liveness check mandates came into force. The compliance math is unfavourable: annual model validation requirements, transaction monitoring infrastructure, and a customer identification flow rebuilt from scratch to support biometric verification. For a lender operating at thin margins on small-ticket loans, these are structural costs, not administrative overhead. The most credible exit is a portfolio sale: a licensed acquirer purchases the loan book and customer data, leaving the shell entity to wind down.

The second category is USSD-native operators. These are primarily community and state-level microfinance banks whose onboarding flow is built on USSD — a protocol that does not support liveness checks as currently specified by CBN. The compliance gap is not a matter of capital or engineering capacity. It is architectural: the customer acquisition channel is incompatible with the mandate’s biometric verification requirement. Approximately 900 CBN-licensed MFBs fall into this cohort, concentrated in states outside Lagos and Abuja. Their value to an acquirer is the MFB licence itself, not the operating business. The Moniepoint-Sumac and Paystack-Ladder transactions established the precedent: a licence is worth acquiring even from a marginal operating institution.

The third category is mid-tier PSPs with user bases but weak compliance infrastructure. These are the most contested acquisition candidates — companies with meaningful customer scale, particularly in specific merchant verticals, that lack the engineering teams to implement the full CBN mandate stack but retain commercial value. These operators are likely to seek compliance partnership structures before accepting acquisition terms: a white-label arrangement with a tier-one fintech that provides the compliance infrastructure while the mid-tier operator retains its brand and merchant relationships.

Deal Structures and the CBN Approval Variable

Three transaction structures are operationally viable in the current regulatory environment. Direct acquisition — a top-tier fintech purchases an MFB or PSP, migrates the assets, and winds down the legacy entity — is the cleanest structure but also the most CBN-intensive. Licence transfer and entity merger both require CBN prior approval, and the regulator’s bandwidth for processing M&A applications during an active enforcement period is a genuine constraint. BETAR analysis suggests that formal transactions in the consolidation candidate tier will become publicly visible by Q3 2026, as CBN processes the backlog of applications generated by the March 31 enforcement cycle.

Portfolio purchase — acquiring the loan book or customer base without the regulated entity — avoids the CBN merger approval requirement but is limited to specific asset types. A compliance partnership or BaaS arrangement requires no CBN approval but produces less certainty for the acquirer. For operators that want a clean resolution rather than an ongoing dependency, this structure is transitional at best.

The CBN approval variable is the least legible element of the timeline. The regulator has demonstrated willingness to move at pace on enforcement — but M&A approval is a different workflow from enforcement, and the 2027 electoral calendar will progressively constrain the CBN’s appetite for headline-generating actions as the year progresses.

Q2 2026 Watchlist

Three specific deal dynamics merit monitoring before the end of June.

Seamfix and the KYC infrastructure play. Seamfix is a Lagos-based identity verification company whose core product — biometric KYC, liveness check infrastructure, and NIBSS integration — is precisely what USSD-native operators lack and what acquirers need to onboard at scale. An acquisition of Seamfix would give either Moniepoint or Flutterwave a proprietary compliance-infrastructure capability to extend to third-party operators, converting a direct-to-customer product into a B2B compliance platform. Both companies have the strategic logic and the acquisition capability. A deal in this category would be transformative rather than merely consolidating.

The digital lending book acquisition. OPay and PalmPay have both signalled commercial interest in expanding their credit products to serve their existing merchant and consumer bases. A portfolio acquisition of an unlicensed digital lender’s loan book — removing the compliance-incapable operator from the market while adding a seasoned credit asset — is a capital-efficient way to do so. Watch for CBN FCCPC joint clearance filings, which are required for consumer credit portfolio transfers above a certain threshold.

The MFB licence extension for The Stack Group. Paystack MFB is currently licensed as a microfinance bank, not a national MFB. The distinction matters: a national MFB licence requires N5 billion minimum paid-up capital and permits full operations across all 36 states; a standard MFB licence has lower capital requirements but geographic restrictions. As Paystack MFB activates its BaaS and merchant lending products, a national MFB upgrade application becomes operationally necessary. Whether that upgrade comes via organic capitalisation or a second acquisition — picking up a licensed entity in a state where Paystack MFB currently has no operating presence — is the Q2 question to watch.

The compliance window closed in March. The M&A window opened at the same moment. Whether the consolidation wave runs at CBN speed or at market speed will define which operators are still standing when the 2027 electoral cycle puts a ceiling on regulatory intensity. The acquirers know who they are. The targets know what they need to resolve. The Q2 calendar is when the two populations begin to close the gap.

BETAR.africa | Business Desk analysis. Related: BETA-1139 — Nigeria Fintech Post-Compliance Sector Map · BETA-1073 — Paystack Ladder MFB · BETA-1256 — Flutterwave CBN MFB Licence · BETA-1027 — Nigeria Fintech Compliance Cost Stack · BETA-1002 — Nigeria Fintech Compliance Moat.