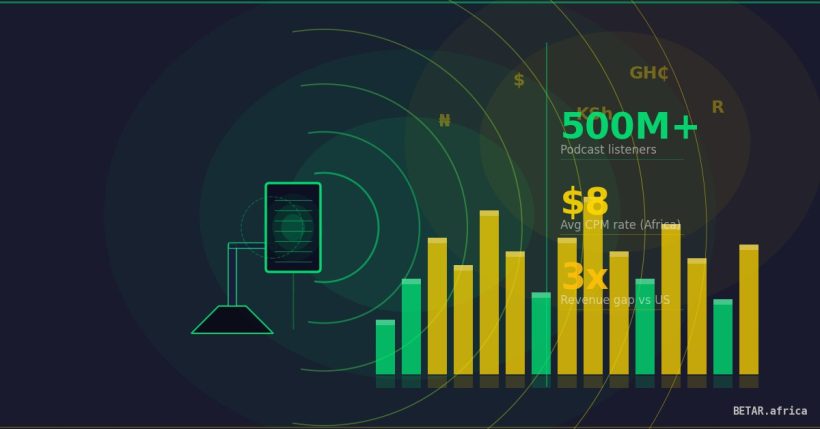

Africa’s podcast audience is growing faster than almost anywhere on earth. Ad revenue is not keeping up. The economics of the continent’s audio boom reveal a market rich in listeners and thin in dollars — and a creator class searching for models that actually pay.

The Reach-Revenue Gap

Podcast consumption in Nigeria jumped 97% in recent years. Local podcast creation rose 48% in the same period. Nigerians have streamed nearly 60 billion hours of podcast content on Spotify alone since the platform launched in the country. Across the continent, South Africa, Nigeria, Kenya, and Ghana have emerged as the four largest podcast markets by listenership — among the fastest-growing globally.

The money, however, has not followed the ears.

Africa accounts for less than 1% of global advertising spend. In absolute terms, that means African creators are fighting over roughly $5.1 billion in total ad market — against a global pool of $780 billion. The podcast sector captures only a fraction of that $5.1 billion. The structural result: African podcasters are building audiences in a market where the advertising infrastructure to monetise those audiences barely exists.

The Middle East and Africa podcasting market is projected to add more than $2.06 billion in value through 2030, with Africa’s slice of that expected to reach $18.78 million by 2027, growing at approximately 7.88% annually. Nigeria’s podcasting market alone is projected to hit $788 million by 2030, according to Grand View Research — a figure that reflects long-term growth potential more than present earnings. South Africa’s podcasting sector is forecast to grow at a compound annual rate of 34.8% between 2025 and 2030. The trajectory is clear. The current payout is not.

What Brands Pay — and What They Don’t

In the United States and United Kingdom, podcast advertising CPMs — cost per thousand listener impressions — typically range from $18 to $50 depending on audience size, show topic, and ad placement. Mid-roll host-read ads in premium shows can command even higher rates. These figures represent a mature market with standardised measurement, established ad networks, and advertiser confidence in podcast attribution.

African podcast CPM rates are not formally published or aggregated. There is no IAB Africa benchmark specific to audio. According to Afripods CEO Henrik Barck, the implicit rate is significantly lower — often by a factor of five to ten relative to Western markets — when deals are made at all. Many African podcasters cannot access standard programmatic advertising because no regional ad network serves their inventory at scale. The absence of standardised metrics — verified listener counts, completion rates, geographic breakdowns that satisfy African advertisers — further suppresses the market.

The brands that do invest in African podcast placements tend to be fintech companies navigating the continent’s startup economy. Nigerian podcasters have secured sponsorships from PiggyVest and Paystack — two of the country’s better-capitalised fintech firms — reflecting an alignment between podcast audiences (educated, urban, financially active) and the target customer for digital financial products. But these are individual deals negotiated show by show, not a market. They represent relationships, not infrastructure.

I Said What I Said, Nigeria’s top-charting podcast hosted by Jola ‘Jollz’ Ayeye and Feyikemi Abudu, illustrates what a viable creator business looks like at the frontier of this market. The show was among the 13 recipients of Spotify’s 2022 Africa Podcast Fund, sharing in a $100,000 grant pool distributed to creators across Nigeria, South Africa, Kenya, and Ghana. Beyond the grant, the show’s revenue model combines brand partnerships with Nigerian corporate advertisers and live events that convert audience loyalty into direct ticket and sponsorship income — a multi-stream stack assembled without the programmatic ad infrastructure that Western creators take for granted. It is a model that works at scale only because its creators built it before a market existed.

The Platform Landscape

Spotify is the dominant global platform for African podcast listeners, capturing 35.1% of surveyed listening in major markets, according to the Reuters Institute Digital News Report. The platform has made deliberate investments in African audio: in 2022, Spotify’s Africa Podcast Fund distributed $100,000 across 13 creators from South Africa, Nigeria, Kenya, and Ghana — providing both cash and distribution support. Spotify for Podcasters offers African creators analytics tools and global distribution, though its direct monetisation features are inconsistently available across African markets.

Apple Podcasts commands a slice of the listening market, particularly among South African and Kenyan audiences with higher smartphone penetration. But neither global platform has built localised monetisation infrastructure that connects African advertisers to African audiences at scale.

The gap is where Afripods operates. Founded in 2017 and headquartered to serve a pan-African creator base, Afripods was the first podcast platform to pay African creators directly — without requiring a US or European bank account, which had previously been a structural barrier to receiving any platform revenue at all. The platform hosts content in more than 50 languages, including Xhosa, Kikuyu, and Yoruba, and has partnered with over 110 broadcast radio stations to convert radio programming into podcast form, extending reach to non-streaming audiences. Afripods functions as both an advertising marketplace — connecting podcasters with regional brands — and a creator community, running events and collaborative initiatives through its #AfropodsMeets series.

Audiomack, primarily a music distribution platform with strong roots in African hip-hop and afrobeats, has extended its monetisation programme to African creators, opening another channel — however limited — for audio revenue on the continent.

What Creators Are Actually Doing

Given the thin advertising market, African podcasters have built revenue stacks that look different from their Western counterparts. Sponsorship and brand partnerships remain the primary revenue model, but most shows are self-funded, with creators operating for years before attracting any commercial interest. Crowdfunding and listener support — via Patreon or direct appeals — are common supplementary income sources, particularly for shows with loyal niche communities.

Live events have emerged as a significant revenue mechanism. Several Nigerian and South African podcasters now host live recordings of their shows, monetising through ticket sales or corporate sponsorship of the event itself. The live format converts a passive listener into a paying attendee, bypassing the platform-CPM problem entirely. It also creates the kind of visible, measurable event that brands — particularly in financial services and lifestyle categories — are willing to attach their names to.

Kenya’s video podcast market adds a further dimension. Kenyan video podcasters are outperforming traditional broadcasters on YouTube by a significant margin: the average podcast video accumulates over seven times the views of a mainstream media upload and fourteen times the engagement in likes, shares, and comments. Kenya is also the world’s fastest-growing internet advertising market, with a compound annual growth rate of 16% through 2029 — more than double the global average. PwC projects video advertising specifically will grow at 22.3% annually through 2029. Specialist podcast studios like SemaBOX in Nairobi are emerging to serve creators who want production quality without equipment investment — a sign that the economics are beginning to support a professional services layer around podcasting.

TikTok’s algorithm has become an unexpected distribution channel for African podcasters, with short clips driving show discovery among younger audiences. While TikTok’s Creator Fund excludes virtually all of sub-Saharan Africa, the platform’s organic reach has proven valuable for audience acquisition that converts to other revenue streams — particularly live events and brand outreach.

The Investment Gap

Venture capital has not arrived in African podcast-native media companies in any meaningful way. Unlike the wave of fintech, agritech, and healthtech funding that characterised African startup activity in the early 2020s, audio has not attracted institutional backers willing to build out the infrastructure — measurement tools, ad networks, creator payment rails — that would normalise podcast advertising economics on the continent.

Spotify’s $100,000 Africa Podcast Fund in 2022 was a notable exception, but it was a grant programme rather than an equity investment, and it has not been publicly renewed or scaled. The absence of VC interest partly reflects the global podcast advertising market’s own consolidation challenges — even in mature markets, podcast ad revenue growth slowed following 2022 — and partly reflects the difficulty of building advertising businesses at continental scale in markets with fragmented regulation, inconsistent internet penetration, and high data costs.

For the creator class, the data cost problem is not abstract. The internet is not evenly distributed across the continent, and mobile data prices remain among the highest relative to income globally. A listener streaming a one-hour episode on a metered data plan may spend a meaningful share of daily data budget on a single show. That cost suppresses listening frequency — and frequency is what advertisers pay for.

The Shape of What’s Coming

The economic case for Africa’s podcast industry rests on structural trends that have not yet translated into creator income: rising smartphone penetration, falling data costs in competitive markets, growing urban middle classes, and — critically — a demographic profile ideally matched to audio. The average African podcast listener is between 24 and 30 years old, part of a cohort that is digitally native, brand-aware, and increasingly financially active. These are valuable audiences. The infrastructure to monetise them at scale does not yet exist.

What does exist are individual operators building revenue models show by show, city by city, brand deal by brand deal. Platforms like Afripods are creating the payment rails that global incumbents have not prioritised. Video is accelerating commercial viability in markets like Kenya, where advertising dollars are growing faster than anywhere else on earth. And a creator class that has spent years producing content without significant payment has developed the diversified revenue instincts — live events, merchandise, community, direct support — that many Western podcasters only discovered when platform revenues collapsed.

Africa’s podcast economy has the audience. The advertising market is coming. The gap between those two facts is both the challenge and, for the operators who close it first, the opportunity.