The Ownership Divide: Africa’s Animation Studios and the Economics of IP

When Kugali Media announced its collaboration with Disney Animation in 2020 to produce Iwájú — a futuristic Lagos-set series that premiered on Disney+ in February 2024 — the deal was celebrated as a cultural milestone. The more significant story was the commercial structure behind it. Kugali did not receive a work-for-hire commission from a larger studio. The Lagos-founded company originated the intellectual property from its existing comic universe and brought it to Disney as a creative partner. That distinction, between studios that own their IP and those that manufacture animation on behalf of someone else, is now the defining economic fault line in African animation.

Work-for-Hire: The Structural Trap

For most of the industry’s history, African animation studios operated as production service providers — essentially skilled labour deployed on terms set entirely by international buyers. The work-for-hire model generates revenue once: a flat fee tied to delivery of finished frames, with no royalties, no residual rights, and no stake in the downstream commercial life of the content. A studio that animates a series for a European broadcaster receives its production fee and exits the economics entirely. If that series generates decades of licensing revenue through merchandise, syndication, and streaming, none of that flows back to the African studio.

The economics of this model are unfavourable even on pure production terms. African animators work at a significant wage discount relative to their peers in the United States and Western Europe. Junior animator roles at Triggerfish Animation Studios, South Africa’s largest animation house, pay approximately ZAR 167,930 per year — roughly $9,200 at current exchange rates — compared to $60,000 to $120,000 per year for equivalent roles in the US market. That six-to-ten times labour cost differential is the core argument international co-producers make for involving African studios. It has also depressed the capital accumulation necessary to finance independent IP development.

Triggerfish: Scale Without Full Ownership

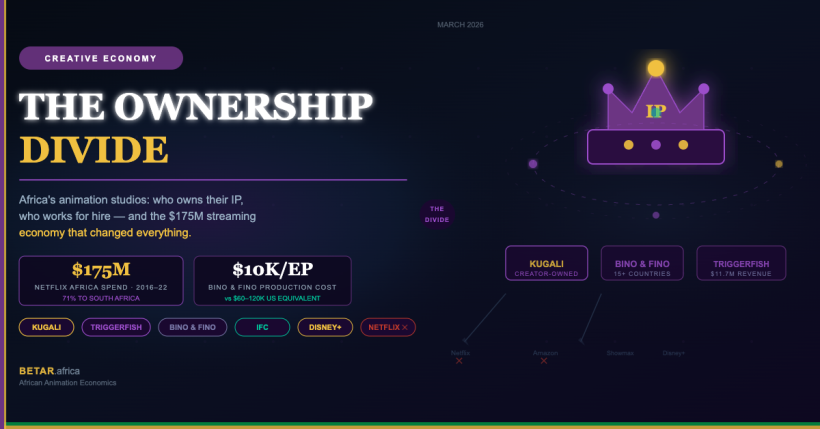

Triggerfish represents the most commercially advanced studio on the continent and the clearest example of how far a service-oriented model can scale — and where its limits lie. Based in Cape Town with a second studio that opened in Galway, Ireland in 2025, the company employs between 100 and 250 people and generates an estimated $11.7 million in annual revenue, according to third-party estimates. Those figures represent substantial scale by African animation standards. They also illustrate the ceiling: $11.7 million for a studio that has secured Netflix and Disney+ deals, co-produced multiple series with global distribution, and operated continuously for over two decades.

Triggerfish’s Netflix engagements include Mama K’s Team 4 — announced in 2019 as Netflix’s first commissioned African animated series, co-produced with London-based CAKE Entertainment — and Supa Team 4, which released two seasons in 2023 and was co-produced with CAKE and France’s Superprod Studio. In both cases, the animation itself was produced by studios outside Africa: Superprod handled the animation on Supa Team 4, while Triggerfish functioned primarily as the creative development and showrunner entity. The production fee income — substantial but undisclosed — does not come with residual rights. Neither Netflix nor any other major streaming platform has publicly committed to ongoing royalty payments to African creative partners.

In February 2024, the International Finance Corporation formalised a collaboration agreement with Triggerfish aimed at expanding market access and advisory support for the African animation sector. No monetary value was disclosed in connection with that partnership, which was structured as institutional backing rather than a direct investment. The IFC’s involvement signals multilateral recognition of the sector’s development potential while also highlighting the degree to which African animation remains reliant on external institutional validation to access co-production pipelines.

What Platforms Pay — And Refuse To

Netflix’s financial exposure in Africa gives some context for the scale of the streaming economy without disaggregating animation specifically. Between 2016 and 2022, Netflix spent approximately $175 million across Nigeria, Kenya, and South Africa on content — licensing and commissions combined. South Africa captured 71% of that total, approximately $125 million, reflecting Triggerfish’s gravitational pull and the broader Cape Town production infrastructure. Nigeria received $23.6 million. Kenya received the smallest allocation of the three.

Netflix’s 2025 global content budget stands at $18 billion, with 51% now directed toward internationally sourced content — a structural indicator of where streaming economics are moving. Whether African animation can secure a larger share of that expanded international envelope is partly a question of production infrastructure and partly a question of rights arrangements. Netflix’s position on royalties, stated explicitly to South African regulators reviewing copyright legislation, is that its subscription-based revenue model is incompatible with ongoing royalty payments to creators. IP ownership by African studios, in other words, does not translate into streaming royalty income under current platform terms.

Amazon Prime Video’s 2024 withdrawal from African original content commissioning further reduced the buyer pool. The exit was framed as part of a broader restructuring of international operations, but the practical effect was to remove a competing bidder from a market with few enough buyers that any exit shifts negotiating dynamics. The contraction of Showmax — the MultiChoice-backed streaming platform — provides a counterweight of sorts: Showmax spent approximately ZAR 3.95 billion ($235 million) on content across 2024 and 2025 while absorbing operating losses of ZAR 8.79 billion ($524 million) across that same period, a structural loss rate of roughly $2.50 spent for every $1 earned. The platform is buying market position, which generates commissioning opportunities for African studios, at a cost that is not commercially sustainable indefinitely.

The Production Cost Equation

The economics of African animation production are most transparent at the smaller studio scale. Bino and Fino, created by Adamu Waziri and produced by EVCL from Abuja, Nigeria, represents Africa’s most distributed independent animation property: the series broadcasts in more than 15 countries and has been dubbed into 14 languages including Hausa, Igbo, Yoruba, Swahili, and Persian. Industry estimates place production cost at approximately $10,000 per eight-minute episode — roughly $1,250 per finished minute — produced by a core team of four over approximately six weeks per episode.

That production cost structure is competitive with outsourced animation work from Southeast Asia and materially below Western European and US production rates. Global broadcast-quality 2D animation runs from $1,500 to $20,000 per finished minute depending on complexity; 3D production costs run higher still. African studios operating in the $1,000 to $3,000 per minute range carry a legitimate cost advantage when serving international buyers. The commercial challenge is that the buyers who can deploy that cost advantage most effectively — large streaming platforms, international broadcasters — are the same buyers whose rights structures strip African studios of long-term IP value.

Market Sizing: What the Numbers Actually Measure

The African animation market is frequently cited at values in the range of $14.52 billion for 2024, rising toward $29.51 billion by 2033 at a projected CAGR of 8.2%. Those figures, sourced from market research firms including IMARC Group, represent the total value of animation services consumed across the continent — including advertising animation, educational content, broadcast production, and all derivative animation work — rather than specifically the studio industry’s revenue or IP value. The headline figure is best understood as an addressable market for animation services broadly, not a direct measure of African studio revenues.

A more grounded measure: Africa’s share of the global creative economy stands at approximately 1.5%, per UNCTAD data from 2022. The continent’s film and audiovisual sector — spanning all production formats, not animation specifically — employs roughly five million people and contributes approximately $5 billion to continental GDP. UNESCO has estimated potential output of $20 billion per year and 20 million jobs if the creative sector received commensurate investment. Afrexim Bank’s Creative Africa Nexus fund has committed $2 billion to the creative sector as a step toward bridging that capitalisation gap, though deployment timelines remain aligned with multi-year programme structures rather than immediate studio financing.

The Pan-African Studio Question

The structural bet that Kugali represents — IP origination as the entry point for global platform relationships — has an economic logic that is becoming harder to ignore as the evidence base grows. Kugali brought a pre-existing universe to Disney rather than accepting a commission to animate someone else’s concept. The financial terms of that arrangement remain undisclosed; whether Kugali retained any ongoing IP rights or received solely a co-development and production fee is not a matter of public record. What is documented is the structural position: originating IP creates leverage that work-for-hire production does not.

The challenge for studios seeking to replicate that model is capitalisation. Developing original IP requires upfront investment in writing, visual development, and pilot production before a platform deal is in place. Triggerfish has absorbed those development costs through decades of service work revenue; smaller studios do not have that cushion. The IFC-Triggerfish partnership and Afrexim’s CANEX commitment both signal institutional recognition that the sector needs development financing to escape the work-for-hire trap rather than simply more commissions on existing terms.

What the Pan-African studio model looks like economically is still being written. Its distinguishing characteristics — compared to the current state — would include African IP ownership retained through global distribution, revenue-sharing structures beyond flat production fees, and studio capitalisation sufficient to finance original development without a commissioned buyer in place. The Kugali-Disney deal is a proof-of-concept for one path. Triggerfish’s scale and the IFC’s involvement sketch another. The economics of African animation are at a commercial inflection point. The question is whether the institutional capital now moving into the sector arrives in time to fund the transition before another generation of studios optimises for the fee model instead.