A new composite index scores Africa’s ten largest economies on five pillars of digital readiness. The results confirm a continent split in two — with one group preparing to compete globally and another still fighting for basic connectivity.

Digital infrastructure is no longer just an enabler of economic activity in Africa — it is the economy. Cloud computing, mobile payments, e-government, and AI applications all depend on a foundation that most of the continent is still assembling. Yet talking about “Africa’s” infrastructure as a single story obscures the real picture: a group of front-runners pulling away from a much larger cohort of laggards.

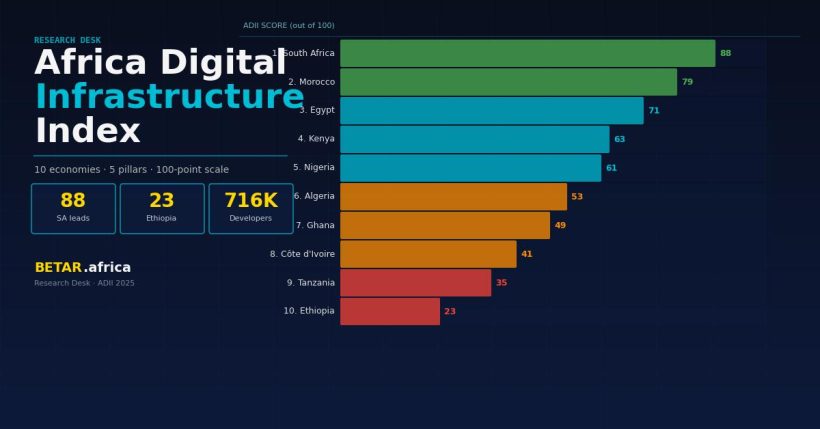

To quantify that divide, BETAR.africa has developed the Africa Digital Infrastructure Index (ADII) — a composite score for the continent’s ten largest economies, ranked across five equally weighted pillars: broadband penetration, mobile internet speed, data center capacity, regulatory readiness, and tech workforce depth. Each country receives a score out of 20 per pillar, for a maximum of 100.

The ten economies — Nigeria, Egypt, South Africa, Algeria, Ethiopia, Morocco, Kenya, Tanzania, Ghana, and Côte d’Ivoire — together account for roughly 70 percent of sub-Saharan and North African GDP.

The Five Pillars: How the Index Was Built

Pillar 1 — Broadband Penetration uses internet penetration rates from ITU’s State of Broadband in Africa 2025 and DataReportal country profiles. Rates range from Morocco’s 92 percent to Ethiopia’s estimated 20 percent.

Pillar 2 — Mobile Internet Speed draws on Ookla’s Speedtest Global Index (December 2025). Morocco’s 5G launch propelled it to 124.32 Mbps median download — 39th globally. Ethiopia’s network, still dominated by Ethio Telecom’s monopoly, sits below 15 Mbps.

Pillar 3 — Data Center Capacity scores based on total installed IT-load megawatts, number of carrier-neutral colocation facilities, and active hyperscale presence (AWS, Azure, Google Cloud). Source: ResearchAndMarkets/GlobeNewswire Africa Colocation Data Center Portfolio 2025–2028 (125 existing facilities, 46 upcoming, across 14 countries).

Pillar 4 — Regulatory Readiness scores based on the presence of a dedicated national broadband plan, data protection legislation, active spectrum reform, and interoperability mandates. Source: World Bank Digital Economy for Africa (DE4A) diagnostic data and ITU-EU Digital Regulatory Mapping 2025.

Pillar 5 — Tech Workforce Depth uses estimates of professional software developer population from OfferZen, Stack Overflow, and IFC’s Africa’s IT Talent Pool analysis. Africa has approximately 716,000 professional developers; more than half are concentrated in South Africa, Nigeria, and Egypt.

The ADII Rankings: Top 10 African Economies

| Rank | Country | Broadband (20) | Speed (20) | Data Centers (20) | Regulatory (20) | Workforce (20) | Total |

|---|---|---|---|---|---|---|---|

| 1 | South Africa | 15 | 16 | 20 | 17 | 20 | 88 |

| 2 | Morocco | 19 | 20 | 13 | 15 | 12 | 79 |

| 3 | Egypt | 17 | 12 | 14 | 14 | 14 | 71 |

| 4 | Kenya | 11 | 12 | 12 | 16 | 12 | 63 |

| 5 | Nigeria | 10 | 11 | 14 | 13 | 13 | 61 |

| 6 | Algeria | 14 | 13 | 8 | 10 | 8 | 53 |

| 7 | Ghana | 12 | 9 | 8 | 12 | 8 | 49 |

| 8 | Côte d’Ivoire | 10 | 8 | 7 | 10 | 6 | 41 |

| 9 | Tanzania | 8 | 7 | 6 | 9 | 5 | 35 |

| 10 | Ethiopia | 5 | 4 | 4 | 6 | 4 | 23 |

The Front-Runners: South Africa, Morocco, Egypt

South Africa leads convincingly, scoring near-maximum on both data center infrastructure and workforce. Johannesburg hosts the continent’s largest cluster of carrier-neutral data centers — Teraco, Equinix’s JB1–JB3, and NTT DATA among them — with over 300 MW of installed IT load. The country’s 2024 National Data and Cloud Policy and established Protection of Personal Information Act (POPIA) provide one of Africa’s strongest regulatory foundations for private investment.

Morocco scores highest on connectivity, propelled by the November 2025 launch of 5G — the only North African country to have deployed it at scale. At 124.32 Mbps median mobile download, Morocco’s network outperforms Turkey, Brazil, and much of Eastern Europe. The country’s Maroc Digital 2030 strategy has attracted Microsoft, AWS, and Huawei to commit data center investments in Casablanca and Rabat.

Egypt is the continent’s dark horse. With 96.3 million internet users — the second-largest user base on the continent — Egypt’s scale offers leverage that smaller digital economies cannot match. Its data center market is expanding rapidly, with Cairo becoming a transit hub for submarine cable traffic between Africa and Europe via the Suez corridor. Fixed broadband, however, remains a weak point: speeds lag behind Morocco and South Africa, and last-mile fiber deployment is concentrated in Greater Cairo.

The Middle Tier: Kenya, Nigeria, Algeria

Kenya punches above its weight on regulation, having enacted a Data Protection Act in 2019 and a new National Digital Master Plan in 2022 that commits to open-access fiber policy. Nairobi’s Konza Technopolis is home to a growing data center cluster. But internet penetration at 47 percent, and a developer talent pool of roughly 60,000, cap its overall score.

Nigeria is Africa’s largest economy but ranks fifth on digital infrastructure — a recurring paradox for a country where fintech volumes routinely exceed the rest of sub-Saharan Africa combined. Lagos hosts Equinix’s LG2 facility (expanded in April 2025) and several domestic operators, but data center capacity per capita remains low. Regulatory fragmentation between the NCC, NITDA, and National Information Technology Development Agency creates friction for private investors.

Algeria has a solid broadband penetration rate (~70 percent) driven by historically subsidised mobile plans, but scores poorly on data center capacity and private sector tech workforce. State dominance in the telecom sector has constrained competition and innovation.

The Laggards: Ghana, Côte d’Ivoire, Tanzania, Ethiopia

Ghana and Côte d’Ivoire occupy a liminal zone: both have active startup ecosystems (Accra and Abidjan are regional hubs for venture activity), but their physical infrastructure scores reflect underinvestment in backbone fiber and power stability.

Tanzania and Ethiopia sit at the bottom of the index — a structural gap, not just a connectivity gap. Ethiopia only opened its telecom market to competition in 2021 with Safaricom’s entry; state-owned Ethio Telecom still holds over 90 percent of mobile subscriptions. Installed data center IT load in Ethiopia is estimated below 10 MW. The country’s 130 million people are served by infrastructure built for a fraction of that number.

The Submarine Cable Wildcard

One variable the index cannot fully capture is the submarine cable build-out now underway across the continent. TeleGeography’s 2025 Africa Telecommunications Map documents 77 active or under-construction cable systems serving Africa, up from 53 in 2020. The Meta-led 2Africa cable — 45,000 km, connecting 46 landing stations across 33 countries — went live in most markets in late 2025, the largest single infrastructure investment in African connectivity history.

For Tanzania, Mozambique, and Côte d’Ivoire, new cable landings represent a genuine opportunity to improve latency and capacity over the next two to three years. The question is whether domestic fiber and last-mile networks can absorb the additional capacity. In most cases, that investment is still outstanding.

What the Index Reveals

The ADII is not a ranking of potential — it is a measurement of current readiness. On that measure, two findings stand out.

First, the gap between South Africa and Ethiopia is wider than any comparable pair of economies on any other continent. A score of 88 versus 23 out of 100 represents a structural divide that will not be resolved by a single subsea cable or a new national broadband plan.

Second, regulatory readiness is the most improvable pillar — and the one where African governments have the most direct control. Countries that enact clear data protection laws, mandate open-access fiber, and create independent spectrum regulators see private investment follow. Those that don’t, wait.

For infrastructure investors, hyperscalers, and development finance institutions, the ADII points to a short list of market-ready destinations: South Africa, Morocco, Egypt, and Kenya. The rest of the continent represents long-horizon bets — significant in potential, but requiring foundational investment that the market alone will not make.

Sources: ITU State of Broadband in Africa 2025; GSMA Mobile Economy Sub-Saharan Africa 2025; Ookla Speedtest Global Index (Dec 2025); ResearchAndMarkets/GlobeNewswire Africa Colocation Data Center Portfolio 2025–2028; World Bank Digital Economy for Africa (DE4A) initiative; TeleGeography Africa Telecommunications Map 2025; IFC Africa’s IT Talent Pool; OfferZen State of South Africa’s Developer Nation 2025; DataReportal internet penetration country profiles; Carnegie Endowment for International Peace, “Beneath the Waves” (March 2025).