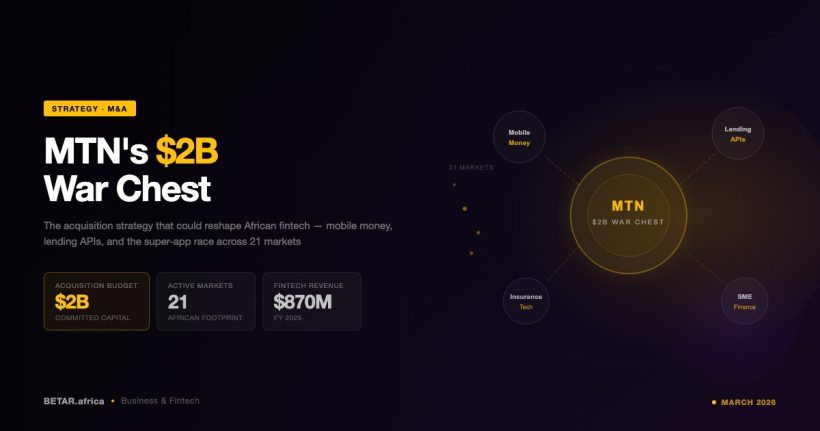

MTN Group enters 2026 with more than $2 billion in cash, 300 million subscribers across 19 African markets, and a chief executive who has publicly stated that the company is no longer a telecoms business. “We’re no longer just a telco. We’re building platforms,” Ralph Mupita told Semafor in February. The comment was brief, but it carried significant strategic weight — because MTN now has the capital, the distribution, and the stated intent to acquire its way into a position that would make it the most powerful financial services company on the continent.

The question is not whether MTN will make major fintech acquisitions. It is which ones, and when.

The Platform Thesis

MTN’s MoMo mobile money service already operates in 16 African markets with more than 70 million active users. By volume and reach, it is already one of the continent’s largest financial services platforms. But MoMo’s current proposition is primarily payments — airtime, merchant transactions, person-to-person transfers, and cross-border remittances. It does not yet have the depth in lending, insurance, savings, or investment products that would make it a full-service financial platform rather than a payments rail.

That gap is what Mupita is targeting with acquisitions. In an interview with Semafor, he confirmed that the company is actively scouting targets in payments, lending, and remittances — specifically capabilities that can be plugged directly into MoMo and activated across MTN’s subscriber base. The formula is simple in concept: MoMo has the customers; the acquisition targets have the product depth. Combine them, and the result is a financial services platform that no African fintech startup could match in distribution terms.

Mastercard validated the thesis in 2024, making a $200 million investment for a 3.8 percent stake in MTN Group Fintech. A $200 million strategic investment from Mastercard is not a passive bet; it is a signal that one of the world’s largest payments networks sees MTN Fintech as a credible long-term platform, not merely a mobile money operator.

The East Africa Opening

The most consequential part of MTN’s acquisition ambition is geographic. MTN operates at scale in Nigeria, Ghana, South Africa, Uganda, and Rwanda, among others — but the company remains absent from three of sub-Saharan Africa’s most important markets: Ethiopia, Kenya, and Tanzania. In aggregate, those three countries represent more than 200 million people, fast-growing mobile money penetration, and well-developed fintech ecosystems.

MTN tried to enter Ethiopia through a traditional network licence in 2021, bidding $600 million before walking away when the terms did not make sense. Mupita has since suggested that future East African entry may not follow traditional telecom models at all — that fintech or digital infrastructure could be the entry point instead of building a mobile network from scratch.

That framing opens a strategically significant possibility: MTN acquiring a Kenya-licensed financial services company, for example, would give it immediate regulatory access to MoMo’s largest missing market without the capital intensity of building a network. Kenya’s M-Pesa ecosystem has produced a generation of fintech companies operating within or adjacent to the Safaricom/M-Pesa rails — some of which would represent logical acquisition targets for a company with MTN’s capital position and distribution ambitions.

The Playbook Is Already Running

MTN is not approaching this as a future ambition. The playbook is already in execution. In late 2024, MTN Nigeria acquired MoMo PSB — the payment service bank entity that had been partially owned by Acxani Capital — for approximately ₦16.35 billion, with a further ₦9.4 billion invested to strengthen the balance sheet. That acquisition gave MTN Nigeria direct ownership of its mobile banking licence, rather than operating through a joint venture structure. Simultaneously, MTN Uganda is pursuing a spin-off of its MoMo unit as an independent fintech company, a structure that would allow the entity to raise external capital and pursue acquisitions in its own right across East Africa.

These are not peripheral moves. They are the structural preparation for a company that intends to be a multi-product financial institution operating at continental scale.

What This Means for African Fintech

African fintech companies raising Series A and Series B rounds in the next two years should be thinking seriously about MTN as both a competitor and a potential acquirer. A company that lands on MTN’s target list for an acquisition would be looking at a distribution unlock — 300 million subscribers — that no venture fund could replicate.

For the broader competitive landscape, MTN entering lending, insurance, or investment products directly via acquisition would represent a step-change in competitive dynamics for the segment it enters. The African lending market, for instance, has seen dozens of startups build customer acquisition infrastructure at significant cost. If MTN acquires one and routes its subscriber base through that product, the unit economics change overnight.

The precedents are clear. Flutterwave bought Mono to own the open banking layer. Moniepoint bought Sumac to acquire a Kenyan banking licence. Paystack absorbed a microfinance bank to expand its product footprint. All of these companies are large by African standards. MTN is in a different category: it has 3 to 4 times the subscriber base of any of them and $2 billion in cash on its balance sheet.

The consolidation wave in African tech is real. MTN is its largest potential actor — and it is just getting started.

— Business Reporter, BETAR.africa