Africa’s performing rights organisations collected a combined record in 2024. But the numbers inside each country’s accounts tell a more fractured story — of one organisation setting benchmarks, another paying out less than $300,000 in US dollar terms despite record local-currency figures, and a third barred from collecting at all.

Music publishing is the business of what happens to a song after it is written. Every time a composition is broadcast on radio, performed live, streamed on a platform, or placed in an advertisement, the writer and publisher are entitled to a royalty payment. In Africa, three collecting societies dominate that pipeline: SAMRO in South Africa, COSON in Nigeria, and MCSK in Kenya. Together, they are the primary filter between commercial music use and the creators who wrote the works.

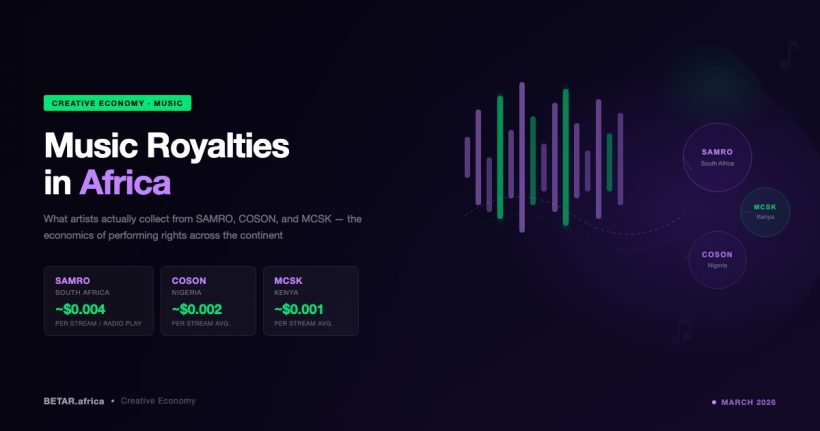

SAMRO: The Benchmark

South Africa’s Southern African Music Rights Organisation distributed R429.2 million in royalties in the financial year ended June 2024 — the highest figure in the organisation’s history, up 48.3 percent on the prior year. Total licensing revenue collected reached R684 million.

The scale of that increase reflects structural change rather than organic market growth alone. SAMRO began collecting from digital service providers only in 2021. In FY2024 it made what it described as a “groundbreaking” R33 million distribution covering Spotify, Apple Music, Netflix, TikTok, and Facebook — the first major digital royalty payout to its members.

The gap between collection and distribution remains significant. SAMRO collected R684 million in licensing revenue but distributed R429.2 million — a difference accounted for by administrative costs, the processing cycle for foreign royalties, and unclaimed distributions. A 2025 update noted that R22 million in previously unclaimed royalties was unlocked after the organisation updated member banking details.

“We acknowledged the challenges posed by unregistered music creators and unnotified musical works, which have hindered the accurate distribution of royalties in the past,” said SAMRO CEO Annabell Lebethe in the organisation’s statement accompanying the R33 million digital distribution. “In response to these challenges, we implemented operational tactics that leverage data from DSPs, VoD’s and tools such as auto-copyright tools and CISNET.”

SAMRO’s declared target is R1.2 billion in annual revenue and R1 billion in distributions by 2028. On current trajectory, those figures are achievable — but they also illustrate that even Africa’s most professionally administered PRO still processes the majority of its revenue from traditional broadcast, not digital.

COSON: Record Numbers, Devalued Currency

Nigeria’s Copyright Society of Nigeria distributed N465.5 million in royalties in 2024 — its highest annual figure on record, representing a 123 percent increase over the N208.5 million distributed in 2023.

At official exchange rates of approximately N1,600 to the US dollar, that N465.5 million equals roughly $291,000.

That is less than SAMRO distributes in a single month.

The comparison is not simply a function of market size. It reflects a structural crisis in Nigerian music rights administration compounded by currency collapse. The naira lost over 50 percent of its dollar value in 2023 alone following the removal of the official peg. Royalty distributions denominated in naira and set by collection rates agreed with domestic broadcasters and venues have not kept pace with the currency’s depreciation.

The governance dimension adds further complexity. COSON’s operating licence expired in May 2019. The Nigerian Copyright Commission demanded a forensic audit as a condition of renewal; COSON refused, and continued operations regardless. A Federal High Court ruled that the licence had lapsed. Nigeria’s Collective Management Regulations 2025 now allow rights holders to choose their CMO freely, formally ending COSON’s de facto monopoly.

MCSK: The Audit Breakdown

Kenya’s Music Copyright Society collected Ksh 139.3 million in FY2023 from public performance and mechanical income combined. But the Kenya Copyright Board found in early 2024 that Ksh 56 million of that was unaccounted for. Audited accounts had not been filed for five consecutive years.

MCSK’s operating licence was not renewed when it expired in mid-2024. The High Court dismissed the society’s subsequent petition. As of February 2026, MCSK is barred from collecting royalties in Kenya.

The January 2024 distribution paid out Ksh 20 million to more than 16,000 registered artists. The top earner received Ksh 757,092 — approximately $5,850. The average per registered member was approximately Ksh 1,250 — about $8.

What the Global Context Reveals

The International Confederation of Societies of Authors and Composers (CISAC) reported that total African royalty collections reached €90 million in 2024, up 14.2 percent year-on-year. Africa was the fastest-growing region by percentage. It also remained the smallest — representing 0.64 percent of the €13.97 billion collected globally.

That 0.64 percent share sits against a continent with over 1.4 billion people, a rapidly expanding music streaming market, and genres — Afrobeats, Amapiano, Afropop — with documented global commercial reach. Sub-Saharan Africa’s recorded music market surpassed $110 million in 2024 (IFPI), with Spotify alone paying out $59 million in royalties to Nigerian and South African artists last year. But platform streaming payouts to master rights holders are structurally different from publishing royalties distributed through PROs to composers and songwriters. The two revenue streams follow separate pipelines.

The Black Box Problem

A significant portion of African compositions are simply not registered in ways that allow global collection systems to identify them. When a composition’s metadata — writer name, ISRC code, publisher, rights splits — is incomplete or inconsistently recorded across systems, streaming platforms and broadcasters cannot match usage to rights holders. The unmatched revenue is pooled and redistributed to already-registered rights holders by market share.

This is the “black box” mechanism: money earned by African compositions that flows to rights holders elsewhere. CISAC and Downtown Music Publishing Africa have both identified the root causes: unregistered works, unsigned royalty split agreements, missing screen and live performance documentation, and DSP metadata that carries variant name spellings or omits diacritical marks.

Sync: Where the Money Is Largest and Least Documented

Synchronisation rights — the fees paid when a composition is placed in film, television, or advertising — represent the highest-unit-value category in music publishing. A placement in a major streaming series can command $20,000 to $100,000 per song. A local TV advertising placement typically runs $1,000 to $5,000.

The challenge for African composers outside South Africa is that sync deals typically require a publisher with infrastructure capable of issuing licences, clearing rights, and collecting across territories. Most African composers outside major markets do not have publisher representation. The sync income from the global market for African music flows primarily to publishers holding international sub-publishing agreements, not to the composers directly.

The Arithmetic

Africa’s PRO system is growing but operating well below its potential. SAMRO’s record distribution year amounts to approximately $23 million in US terms — roughly what a mid-sized US independent publisher might collect for a single catalogue in a year. COSON distributed under $300,000. MCSK is not currently authorised to collect at all.

The structural requirements for closing the gap are consistent across all three: transparent governance, audited accounts, digital registration infrastructure, and investment in member rights education. Nigeria’s new CMO competition framework may accelerate reform if alternative organisations build credibility.

The CISAC global collections benchmark provides the clearest long-range target: Africa at 0.64 percent of global collections, on a continent generating a disproportionate share of the world’s most streamed music genres. The revenue is there. The question is whether the infrastructure can be built to collect it.