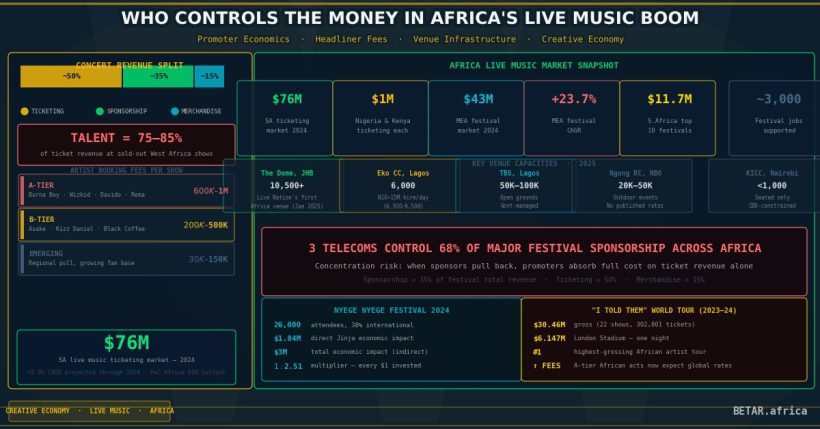

Africa’s live music sector is growing rapidly, but the money is not distributed equally. South Africa’s live music ticketing market generated an estimated $76 million in 2024 — about R1.4 billion — and is projected to grow at 5.9% annually through 2029, according to PwC’s Africa Entertainment & Media Outlook 2025–2029. Nigeria and Kenya each generated approximately $1 million in live music ticket sales the same year. Across the Middle East and Africa combined, the music festival market was valued at $43.16 million in 2024, with a projected compound annual growth rate of 23.7%.

The headline numbers are striking. The business model underneath them is tighter — and in some markets, more precarious — than the streaming era’s global Afrobeats narrative suggests.

The Headliner Fee Problem

The single biggest cost variable in African concert promotion is the artist. For A-tier Afrobeats acts — Burna Boy, Wizkid, Davido, Rema — booking fees have reached $600,000 to $1 million per show, based on industry-estimated figures consistent with fee structures reported in Vanguard, Pulse Nigeria, and The Papers Nigeria.

B-tier acts command between $200,000 and $500,000. That bracket includes names like Asake, Kizz Daniel, and South Africa’s Black Coffee, whose DJ sets carry a global price tag estimated at $300,000. An artist who booked for N3 million five years ago now asks N10 million, according to Cecil Hammond, founder and CEO of Lagos-based Flytime Group. “The greatest challenge really up until now is sponsorship,” Hammond told The Africa Report in 2024, “because every year the artist’s fees go up drastically.”

Hammond’s description of the Afrobeats fee inflation problem maps onto the touring data. Burna Boy’s “I Told Them” World Tour (2023–2024) grossed $30.46 million from 302,801 tickets across 22 shows, making it the highest-grossing tour ever recorded by an African artist, according to Pollstar tracking data. His London Stadium performance alone brought in $6.147 million from 58,973 tickets in a single night. When A-tier artists can command these figures in London or New York, their African market fee expectations rise accordingly — even when local venue capacities and ticket price ceilings cannot absorb the same economics.

Venue Infrastructure: The Three Markets

Across Lagos, Nairobi, and Johannesburg, the supply of purpose-built, large-format music venues remains constrained — which shapes both what promoters can charge and what they can spend.

Lagos relies on multipurpose spaces adapted for concerts rather than built for them. The Eko Convention Centre in Victoria Island holds approximately 6,000 in concert configuration. Hire costs are estimated at N10–15 million per day (roughly $6,300–$9,500 at current exchange rates). Tafawa Balewa Square, which can accommodate 50,000–100,000 on its open grounds, is managed by a Lagos State Government entity, with rates negotiated per event.

Nairobi’s concert ecosystem is similarly venue-constrained. The KICC auditorium holds under 1,000 for seated shows. Ngong Racecourse can accommodate 20,000–50,000 for major outdoor events; Carnivore Grounds historically hosts 10,000-plus for concerts. Neither venue publishes commercial hire rates.

Johannesburg received the continent’s most significant venue infrastructure investment in January 2025: Live Nation, in partnership with Stadium Management South Africa and Gearhouse South Africa, opened The Dome in Nasrec with a capacity of 10,500-plus. The venue — Live Nation’s first permanent facility on the African continent — was inaugurated with Tems headlining in March 2025. No equivalent Live Nation or AEG investment has materialised in Nigeria, Kenya, or any other African market.

Promoter Margins: How the Money Moves

A concert promoter in Lagos running a mid-scale headliner show faces a cost architecture that leaves thin margin at best. Artist fees consume the largest share — by some industry estimates, talent costs represent 75–85% of total ticket revenue at a sold-out show in West Africa. Production costs — sound, staging, lighting, security — sit on top. Hammond has noted that his security budget alone exceeds what many international festival operators allocate. Ticketing platform commissions add approximately 10% per ticket on Nigerian platforms including Tickets by Selar and Ticketbay; Arriya charges 5%.

On the revenue side, promoters draw from three primary sources. Ticketing is the largest, accounting for roughly 50% of a festival’s total revenue. Sponsorship contributes approximately 35% — and this is the variable that determines whether a show is profitable. Three telecoms companies reportedly control 68% of major festival sponsorship across African events, creating significant concentration risk. When those sponsors pull back, promoters are left absorbing cost on ticket revenue alone. Merchandise accounts for the remaining 15%.

Flytime’s ticket prices give a sense of the premium end: Flytime Fest 2025 general admission started at N120,000–N180,000 (approximately $75–$113). At an 8,000-capacity sold-out show with an average ticket price of N180,000, gross ticket revenue approaches N1.44 billion — approximately $900,000 at current exchange rates. Against a $600,000 headliner fee, that leaves $300,000 to cover production, security, venue, platform fees, and marketing before any promoter profit is realised.

Festivals vs. Standalone Shows: Different Risk Models

The festival economy runs on different logic. Southern Africa’s 10 major festivals generated a combined $11.7 million in 2024, supporting nearly 3,000 jobs with approximately 80% of production spending retained locally, according to a December 2025 report by Sound Diplomacy and UNESCO. That implies an average of roughly $1.17 million per major festival — smaller gross than a single Burna Boy arena show, but spread across multiple artists and revenue streams.

Uganda’s Nyege Nyege Festival generated $1.84 million directly for Jinja’s local economy in 2024 — from 26,000 attendees, 38 percent of them international visitors from 34 countries — with an estimated $3 million total economic impact when indirect spending is included. “We are proud to have brought about an innovative blueprint for how festivals can both create a life-transforming experience for attendees while at the same time generate a tremendous impact for the economy, from tourism to the creative industries,” said Derek Debru, co-founder of Nyege Nyege, following the publication of the 2025 Ugandan government economic impact report.

Busara Festival in Zanzibar pays approximately $80,000 per edition in government taxes, licences, and permits — a significant overhead that standalone shows do not carry. Every $1 invested in festival production generates an additional $2.51 in local economic activity, according to the Sound Diplomacy data.

The December Effect

Lagos’s “Detty December” is the clearest proof of what live events mean to a city economy at scale. During December 2024, Lagos’s tourism, hospitality, and entertainment sectors generated $71.6 million (N111.5 billion), driven in part by an estimated 1.2 million visitors and a concentration of concerts, shows, and cultural events. Hotels alone contributed $44 million; short-let accommodation $13 million.

This economic multiplier is the strongest argument for sustained investment in venue infrastructure, regulatory clarity, and promoter-side capital. The live music industry is not simply a cultural product — it is a mechanism for concentrating tourism spending, creating employment, and generating tax revenue.

What the Numbers Say

Africa’s live music economy is real, growing, and underwritten by a global Afrobeats moment that has produced the continent’s first billion-dollar touring acts. But the financial architecture that delivers shows to audiences in Lagos, Nairobi, and Johannesburg remains fragile: artist fee inflation is outpacing venue and ticketing revenue growth; venue infrastructure is years behind audience demand; and promoter margins depend heavily on sponsorship income concentrated in a small number of corporate accounts.

Live Nation’s Dome investment in Johannesburg signals that international capital is paying attention. But South Africa’s $76 million ticketing market is not Nigeria’s $1 million one. Until venue-grade infrastructure and reliable sponsorship ecosystems develop in West and East Africa, the concert economy’s wealth will continue to accumulate at the artist tier — not at the promoter, the venue, or the local economy.