Afrobeats is one of the most commercially successful music genres of the 2020s. Its streaming numbers are global; its royalty economics are not. One million Spotify streams from Nigerian listeners generates approximately $300 for rights holders. The same volume of streams from listeners in the United States generates approximately $3,500. From Sweden, approximately $10,000.

That is a 30x differential between the country that produced the music and one of Europe’s premium streaming markets — and it is not an anomaly. It is the structural reality of geography-based per-stream pricing, and it sits at the centre of African music’s most persistent economic problem.

“Africa is a clear growth story in global collections, and the trajectory is real,” said Gadi Oron, Director General of CISAC, commenting on the continent’s 2024 royalty collection results. “But the gap between what the continent generates culturally and what it captures economically in royalties remains one of the biggest structural inequities in the global music industry.”

Why Geography Determines What You Earn

The per-stream rate an artist receives from Spotify or Apple Music is not a fixed global number. It is calculated as a function of the advertising revenue and subscription fees generated in the listener’s country, multiplied by the artist’s market share of total streams in that territory.

In markets with high premium subscriber penetration and strong digital advertising CPMs — Sweden, the United States, the United Kingdom, Germany — per-stream rates are among the highest in the world. In African markets where premium subscription uptake remains low and digital advertising CPMs are a fraction of Western benchmarks, the per-stream economics compress accordingly.

The arithmetic is unforgiving. An Afrobeats artist generating 10 million streams in Nigeria — a substantial number representing a genuinely popular song — would receive approximately $3,000 in streaming income before label and distributor cuts. The same 10 million streams from a diaspora-heavy UK audience would generate closer to $35,000.

This is not a failing of streaming platforms alone. The underlying mechanism — market-specific licensing agreements tied to local ad and subscription revenue — reflects the commercial reality of digital media economics. But for an African artist whose core fanbase lives in Africa, the system structurally discounts the economic value of their most loyal listeners.

The Diaspora Arbitrage

The African music industry’s response to geography-based pricing has been pragmatic rather than ideological: shift the listener base.

The release strategy increasingly favoured by major African labels and management teams is to prioritise international market activation at the point of release — pushing tracks to diaspora communities in the UK, US, and continental Europe before, or simultaneously with, domestic rollout. The economics are explicit: a stream in London pays four to five times more than a stream in Lagos.

This diaspora-first arbitrage is visible in how major Afrobeats releases are now structured. Promotional cycles begin with UK and US playlist pitching. Tour announcements target European and North American venues before Lagos Arena is confirmed. Radio campaign spending tilts toward BBC 1Xtra and US urban radio.

The result is a feedback loop: African artists optimise their release strategies for international streaming markets because the income is structurally larger there, which in turn reinforces their commercial identity as international acts rather than domestic ones — and makes the case for domestic streaming market development harder to prioritise.

Sync: The High-Value Exit From Per-Stream Economics

For African composers seeking income that does not depend on geography-weighted streaming rates, sync licensing represents the most significant alternative revenue channel — and also the most inaccessible.

Sync licensing — placement of music in film, television, advertising, and digital video — bypasses per-stream rate structures entirely. Global sync licence fees for established tracks in major placements range from $20,000 to $100,000. In African advertising markets, a 30-second campaign carrying an original-commissioned composition can generate $5,000 to $15,000 in sync fees and subsequent performance royalties from campaign airplay — more than most African composers earn from collecting societies in three years.

The barrier is not demand. Music supervisors in London, Paris, and Los Angeles are actively sourcing African music for pan-African brand campaigns and international productions. The barrier is discoverability and rights infrastructure. Metadata is fragmented, rights clearance is slow, and payment pathways between international licensees and African rights holders are underdeveloped.

SyncAll, launched in October 2025, is the most concrete structural response to that gap: an end-to-end metadata enrichment and sync-licensing marketplace designed specifically for African music catalogues. The founders are targeting aggregation of 25% of African music metadata and 700 licensing deals within three years — a timeline that, if achieved, would make the sync channel a genuinely addressable revenue line for African publishers and catalogue-holding labels.

The Collection Gap Behind the Numbers

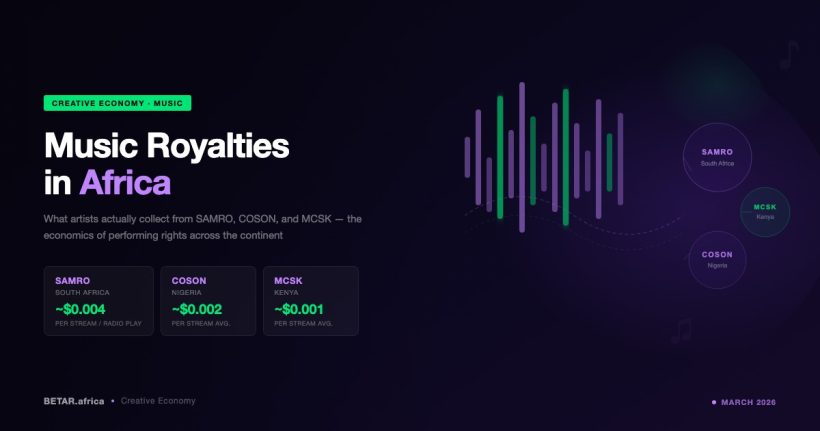

The streaming pay gap sits within a larger structural deficit in how African music generates royalty income. Africa’s performing rights organisations collected a record €90 million in 2024 — the continent’s first time breaching that threshold, according to CISAC’s 2025 Global Collections Report. But €90 million is 0.6% of the €13.97 billion collected globally. Africa accounts for approximately 17% of the world’s population and produces some of its most commercially successful music by genre.

The collection infrastructure story — how SAMRO, COSON, MCSK, and other African PROs perform against that gap — has been covered in detail in BETAR’s earlier analysis, which examined per-artist distribution figures, governance failures, and the 2025 KECOBO licence suspension in Kenya.

Tony Okoroji, Nigeria’s most prominent music copyright advocate, framed the collection problem in terms that apply equally to streaming and PRO distributions. “The licensing universe in Nigeria is enormous — hundreds of hotels, thousands of restaurants, over 600 radio stations — and we are still not capturing the full economic value of the music that makes all of those businesses profitable,” Okoroji said ahead of COSON’s 2024 AGM. “The numbers will grow when the enforcement infrastructure catches up with the economic reality.”

The same enforcement gap exists in streaming: millions of streams are being generated across Nigerian, Kenyan, and Ghanaian listeners daily. The infrastructure to translate that cultural output into economic income at anything approaching parity with Western markets does not yet exist. The 30x gap is not a talent problem. It is an infrastructure problem — and one that will require both platform-level reform and market-level development before African artists capture the full commercial value of the continent’s most commercially powerful cultural export.

Named sources: Gadi Oron, Director General, CISAC (public comments on 2024 Global Collections Report); Tony Okoroji, music copyright advocate and former COSON Chair (industry press, 2024 AGM period).

Additional sources: CISAC Global Collections Report 2025 (Music Business Worldwide); Afro Soundtrack — “Streaming Territories and Royalty Payouts in Nigeria”; The Creative Brief Africa — “The Streaming Pay Gap”; ThatPitch sync licence cost guide (2025); SyncAll launch (October 2025).