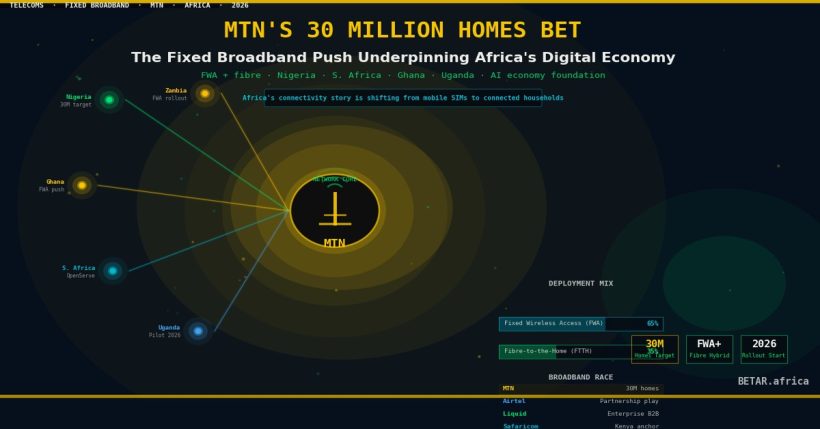

For most of the last decade, Africa’s connectivity story has been told in mobile terms — SIM penetration rates, 4G rollout percentages, the price of a 1GB data bundle. MTN is now rewriting the script. The continent’s largest operator has set a target of connecting 30 million homes across Africa with fixed broadband — a mix of fibre-to-the-home and fixed wireless access deployed at a scale that no African telco has attempted before. The announcement, confirmed to TechCabal in March 2026, positions MTN not merely as a mobile carrier upgrading its network, but as the company building the bandwidth layer on which Africa’s AI economy, fintech rails, and developer ecosystem will depend.

The strategic significance cannot be overstated. MTN’s connected home ambition is one of three core pillars in the company’s roadmap to 2030 — alongside fintech and digital infrastructure. It represents MTN’s answer to a question that has constrained every large-scale digital deployment on the continent: you cannot run inference models, process real-time payments, or stream high-definition content reliably on a congested mobile data connection. Fixed broadband changes the equation.

Why Fixed Wireless Access — And Why Now

The technology choice driving this expansion is worth examining closely, because it is the reason a 30-million-homes target is credible rather than aspirational. MTN is not proposing to trench fibre cables to 30 million front doors. The economics of last-mile fibre construction in African cities — where street layouts are informal, right-of-way permits are complex, and population density drops sharply outside city centres — would make that timeline and capex unworkable.

Fixed wireless access (FWA) solves this. Rather than physical cable, FWA delivers broadband-grade connectivity to a home or business using a dedicated receiver that connects to the operator’s existing 4G or 5G mobile tower infrastructure. Installation takes hours, not weeks. The capital cost per connected home is substantially lower than fibre-to-the-home. And critically, wherever MTN has 5G spectrum — South Africa, Nigeria, Ghana, Uganda — the coverage footprint that was built for mobile subscribers can be repurposed, at marginal additional cost, to serve fixed broadband customers.

MTN’s FWA deployments are already generating meaningful revenue. The operator is targeting high-income households with 5G FWA services and achieving average monthly revenue per user of between $24 and $32 — compared with typical mobile data ARPU well below $5 in most African markets. FWA now accounts for 24 percent of MTN’s 5G earnings, and router costs have fallen below $80, improving unit economics further with each passing quarter. In Nigeria alone, MTN added more than 281,000 home broadband users in the third quarter of 2025.

The Infrastructure Stack That 30 Million Homes Unlocks

The implications of fixed broadband at this scale extend well beyond the consumer experience of faster Netflix. Consider the infrastructure dependencies that BETAR has tracked in Q1 2026 alone.

Every AI application deployed by an African enterprise — the inference calls, the model outputs, the API integrations — depends on low-latency, high-throughput connectivity at the point of use. Mobile data connections, with their variable latency and throttling under congestion, are workable for basic queries but unsuitable for the always-on, real-time AI deployments that African enterprises are beginning to pilot. Fixed broadband at the home and SME level is the bandwidth layer that makes those deployments viable at scale.

The same logic applies to fintech. MTN’s MoMo platform serves more than 70 million active users across 16 markets. The next product tier — lending decisioning, insurance underwriting, micro-investment products — requires richer data signals from users operating connected devices, not just feature phones on intermittent data. Fixed home connectivity accelerates that transition.

For developers, the argument is simpler: a developer building and testing applications on a reliable fixed broadband connection at home is materially more productive than one working on throttled mobile data. Connectivity is a developer tool. MTN is, indirectly, investing in the African developer pipeline.

Capex Tension — Or Strategic Alignment?

MTN enters this infrastructure push simultaneously carrying a $2 billion acquisition war chest earmarked for fintech targets in payments, lending, and remittances — as reported by BETAR in BETA-366. The natural question is whether fixed broadband capex is competing with the M&A ambition for the same balance sheet headroom.

The evidence suggests they are parallel rather than competing budget lines. MTN maintains a capital expenditure discipline of 15 to 18 percent of revenue, a ratio the group has signalled it intends to hold. MTN Nigeria tripled its capex to ₦757.4 billion (approximately $527 million) in 2025 — its largest infrastructure investment in years — without the group announcing any deferral of its acquisition programme. The $10 billion total investment target for African expansion by 2030 is large enough to absorb both.

The MTN-Huawei strategic MoU signed at MWC Barcelona in March 2026 — which BETAR covered in BETA-334 — makes the alignment explicit. The agreement specifically covers coordinated development of FTTH and 5G FWA alongside AI-driven autonomous network infrastructure. Huawei is not being brought in as a network vendor executing a capex programme; the partnership is structured to reduce the unit cost of intelligent fixed broadband deployment over time, making the capex envelope go further. MTN’s Bayobab infrastructure unit meanwhile targets 135,000 kilometres of proprietary fibre backbone — the long-haul layer on which both mobile and fixed services run.

Two Visions of Africa’s Connectivity Future

MTN’s fixed broadband bet throws into sharp relief a strategic divergence with its closest continental rival. Airtel Africa is pursuing a fundamentally different vision: mobile-first, asset-light on infrastructure, and betting its connectivity future on a Starlink Direct-to-Cell partnership covering 14 markets. Airtel’s capital is flowing toward a mid-2026 mobile money IPO and data centre investment, not trenches and FWA radios.

The two models reflect genuinely different theses about where Africa’s next connectivity growth comes from. Airtel’s satellite partnership is compelling for rural and hard-to-reach areas — markets where MTN’s FWA deployment would be uneconomic without existing tower density. MTN’s fixed broadband push is a bet on urban and peri-urban density: that the homes and SMEs within range of its 5G towers represent an underpenetrated, high-ARPU market worth owning before a competitor does.

Both can be right simultaneously. Africa is large enough for multiple connectivity models. But the economics favour MTN’s approach in the markets that generate most digital economy revenue — Lagos, Johannesburg, Accra, Kampala. In those cities, the home broadband market is real, growing, and currently fragmented across dozens of small ISPs and cable operators. MTN is moving to consolidate it.

At 30 million connected homes, MTN would own the bandwidth layer of the African digital economy. That is the actual prize — not the FWA router rental fee.

— Technology Reporter, BETAR.africa