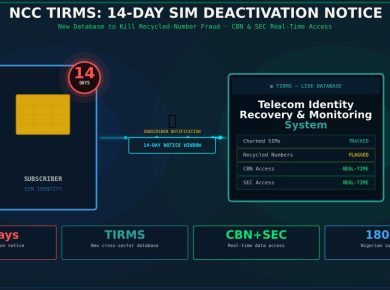

On March 10, the Central Bank of Nigeria issued formal baseline standards requiring banks and fintechs to deploy AI-powered anti-money laundering systems — with annual independent model validation, documented audit trails, and implementation roadmaps due in 90 days. Two days later, on March 12, the CBN issued a separate circular mandating real-time biometric liveness verification for every account opening in the country, with a July 1, 2026 go-live deadline.

Covered separately — as BETAR.africa reported on the liveness mandate and the AI AML standards — each circular is a significant compliance challenge. But the two mandates are not separate problems. They are two halves of the same architecture. And the CBN appears to know exactly what it is building.

The Architecture: Identity at Entry, Behaviour at Transaction

The liveness check mandate addresses who is entering the system. The AI AML standard addresses what that person does once inside. Together, they form a continuous assurance loop that runs from first account opening through every transaction: biometric identity confirmed at onboarding via real-time NIBSS cross-match; machine learning transaction monitoring flagging anomalies in behaviour afterward. The same person who opened the account — verified by biometric — is the person whose transactions are being monitored by a model that knows their risk profile.

This is not an accident of regulatory timing. The CBN’s AML standards explicitly require that KYC and transaction monitoring be integrated — not parallel functions. Customer risk profiles must update dynamically based on transaction behaviour, not locked at onboarding. When you add a mandatory biometric entry point, you establish a high-confidence identity anchor for that dynamic profiling. Liveness verification at onboarding reduces the synthetic identity problem at the front door; AI transaction monitoring detects behavioural anomalies once the account is active. The two mandates are architecturally linked.

The CBN has not stated this explicitly. But for Nigerian fintech product and engineering teams, the implication is clear: the regulator is not asking institutions to build two compliance features. It is asking them to build a compliance system — one in which identity assurance and behavioural monitoring are integrated components of the same infrastructure, not bolt-ons to existing stacks.

A Defined Market for Compliance Vendors

The mandates do not just create compliance obligations. They create a vendor market — and the July 1, 2026 deadline for liveness checks is already driving near-term demand.

The liveness check mandate explicitly permits institutions to use approved third-party identity verification providers, provided those providers have a live, approved connection to the NIBSS biometric database. That clause effectively creates a licensed-access regtech segment. Vendors with existing NIBSS integrations — Prembly, Seamfix, Smile ID, and VerifyMe among the most prominent — are positioned to onboard the tier of fintechs that cannot rebuild their identity infrastructure in-house before July 1. The closer the deadline, the more valuable a vendor with a production-ready NIBSS-connected liveness product becomes.

The AI AML standard creates a different, slower-burn market. Deposit Money Banks face an 18-month compliance window; other licensed institutions have 24 months. But the 90-day roadmap filing requirement — falling in the first week of June 2026 — means that vendor selection decisions must happen now. Institutions filing underdeveloped roadmaps risk attracting early CBN examination before the compliance deadline arrives.

International AML vendors — including players with established African operations like Temenos, Featurespace, and NICE Actimize — have a credible entry point here, particularly for larger DMBs that may already have existing relationships. But the more interesting dynamic is in the domestic market. Companies like Interswitch, which operates compliance infrastructure at the core of Nigerian banking, and emerging fintech compliance players are positioned to offer AML-as-a-service structured specifically around the CBN’s six-domain standard. The vendor that can document CBN audit readiness — with NIBSS integration, independent model validation reports, and audit trail architecture — will find a large, time-pressured captive market among mid-sized fintechs.

The Dual Crunch for Smaller Fintechs and Microfinance Banks

Nigeria’s largest commercial banks and well-capitalised neobanks — Kuda, Moniepoint, OPay, Palmpay — have the engineering teams to absorb both mandates. The more acute pressure falls on smaller digital lenders, payment service providers, and microfinance banks (MFBs) that operate compliance functions built for a lighter-touch regulatory environment.

For these institutions, the double mandate is not just a compliance project. It is a prioritisation crisis. The liveness check deadline is July 1, 2026 — 15 weeks away from the CBN’s March 12 circular. The AML roadmap filing is June 2026. The two timelines overlap, meaning engineering and compliance resources must run two significant infrastructure projects simultaneously with limited slack for delays in either.

Smaller MFBs face a structural challenge the neobanks do not: many operate loan and savings products through USSD or basic mobile apps that were not designed with real-time biometric verification in mind. Retrofitting a liveness check into a USSD-based onboarding flow is a product redesign, not a configuration change. The compliance cost per customer acquired will rise.

For digital lenders — who typically combine BVN validation and credit bureau checks at onboarding — the liveness requirement adds a live biometric step that many current stacks do not support. The AML standard then requires that same customer’s transaction behaviour to be monitored dynamically. A lender with a straightforward loan-disburse-repay product may not have previously needed a transaction monitoring system at all. Now they need two: one for identity at entry, one for behaviour in use.

The Regional Signal

Nigeria is not acting in isolation. Its successful exit from the FATF grey list in October 2025 created a specific political incentive to demonstrate that the improvement is durable — and the AI AML circular explicitly positions Nigeria as among the first African countries to formally mandate ML-based AML systems, not merely permit them. For other African central banks watching, the Nigerian experiment provides a template: biometric identity infrastructure at the national level (NIBSS) combined with an AI-enabled monitoring mandate creates a compliance architecture that satisfies FATF effectiveness requirements without requiring the soft infrastructure of mature financial markets.

Whether that template travels — to Ghana, Kenya, or Egypt — will depend in part on whether Nigeria’s institutions can implement it before the deadlines. A high-profile compliance failure would set back the argument as much as a successful rollout would advance it.

What Fintechs Should Do Now

The practical implication for Nigerian fintech and bank compliance teams is a sequencing decision. The liveness check deadline is nearer and more binary — either your account opening flow includes a real-time NIBSS-validated biometric check by July 1, or it does not. Start there. Engage a NIBSS-connected vendor or test your own integration in staging by April. The device activation cap (₦20,000 for the first 24 hours) requires customer communication planning before go-live.

The AML roadmap is due in June 2026 regardless of your compliance tier. File a credible one. Institutions that use the roadmap window to signal meaningful engagement — rather than aspirational timelines — are better positioned when CBN thematic reviews begin. The standard’s independent annual validation requirement means AML system quality will be externally visible.

The deeper institutional question is whether to treat these as two separate compliance projects or one. The CBN has not mandated integration. But the architecture it has mandated — high-confidence identity at entry, ML-based behavioural monitoring at transaction — will be more defensible, and more efficient, if the two systems are designed to work together from the start.