By BETAR.africa Creative Economy Desk | 21 March 2026

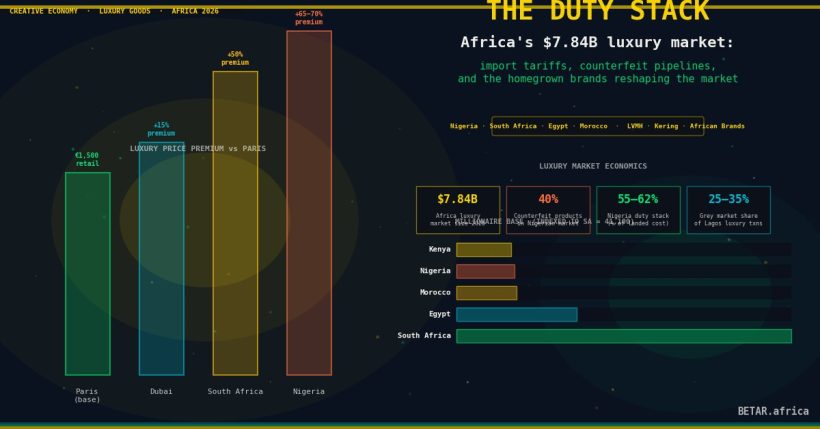

A Louis Vuitton Neverfull MM handbag retails for approximately €1,500 in Paris — the cheapest place in the world to buy the French house’s staple tote. Walk into Polo Luxury’s flagship store on Victoria Island, Lagos, and the same bag costs between ₦3.2 million and ₦3.8 million, equivalent to roughly $2,200–$2,600 at mid-2025 exchange rates. The price gap is not merely an exchange rate artefact. It is the arithmetic of Africa’s luxury duty stack — and it is reshaping every commercial decision in the continent’s $7.84 billion luxury goods market (Statista, Luxury Goods — Africa Market Forecast, 2025).

The Duty Stack: Quantifying the Nigerian Mark-Up

Nigeria’s customs regime applies a layered charge structure on imported luxury goods that makes fiscal transparency difficult. The Nigerian Customs Service collects import duty at rates of 35–50% on leather goods, apparel, and accessories classified under the relevant HS codes, on top of which retailers must absorb a 7.5% Value Added Tax, a 7% Import Adjustment Surcharge, a 4% Federal Customs Service levy, and a 0.5% Economic Transition Levy. On a €1,500 bag cleared at Lagos port with a CIF (cost, insurance, freight) landed value of approximately $1,750, the total duty and levy burden can reach 55–62% of the landed cost before retailer margin is applied.

Polo Luxury, which operates mono-brand boutiques for Louis Vuitton, Hermès, and Gucci at its Victoria Island and Abuja Airport Road locations, has positioned its pricing structure around the costs of authentic sourcing, import compliance, and operating standards — characterised in its official brand communications as the defining features of credible luxury retail in the Nigerian market. The retailer does not publish margin data, but industry participants estimate the typical Nigerian luxury retailer operates gross margins of 35–45% after duty costs — comparable to mature markets — while passing the full duty burden to consumers.

The result is a consistent 40–65% price premium over European retail for equivalent luxury goods in Nigeria, excluding currency depreciation effects. South Africa’s tariff regime is lighter — luxury apparel faces duties of 30–45% under the Southern African Customs Union schedule — but rand weakness has compressed the real gap with European retail. The broader regional pattern holds: African luxury consumers pay significantly more for the same goods than their counterparts in Paris, Milan, or Dubai.

The Grey Market and the Counterfeit Pipeline

High official retail prices have predictable consequences. Nigeria’s informal luxury economy — travellers purchasing in Dubai, London, and New York for personal use or resale — is substantial. BETAR.africa estimates, based on analysis of the pricing differential between Nigerian duty-inclusive retail and prices available through Dubai and direct overseas purchase — and accounting for the scale of informal freight volumes documented on the Lagos–Dubai corridor — that grey market channels account for 25–35% of premium goods transactions in Lagos, representing several hundred million dollars in annual volume that bypasses the official retail channel. No authoritative industry body has independently published an informal luxury import volume figure for Nigeria; this estimate is consistent with grey market share levels documented in other emerging markets where import duty differentials exceed 50 percent.

More disruptive is the counterfeit pipeline. According to market intelligence compiled in the Middle East & Africa Luxury Goods Market Analysis 2026–2031 (GlobeNewswire, March 2026), counterfeit luxury products present a “systemic challenge” to premium brands across the region. Counterfeit goods are estimated to account for 40% of products in the Nigerian market broadly, with annual economic losses attributed to counterfeit trade across all product categories — not luxury-specific — exceeding $20 billion (World Bank / Nigeria Consumer Protection Council data).

The luxury supply chain for counterfeits flows primarily from manufacturing clusters in Guangzhou and Yiwu, entering African ports at Lagos (Apapa and Tin Can Island), Mombasa, and Durban through container consignments documented as general merchandise. LVMH, Kering, and Richemont all maintain anti-counterfeiting operations for key African markets — but brand protection spending in sub-Saharan Africa remains a fraction of what these conglomerates deploy in Asia and the Middle East.

The counterfeit effect on authentic pricing is commercially significant. Brands facing high counterfeit penetration face a binary strategic choice: price higher to reinforce the authentic signal against fakes (the exclusivity premium response), or withdraw physical retail and accept that the market is served primarily through grey imports and multi-brand retailers. Most European heritage brands in Africa have defaulted to the second option, which creates the retail infrastructure gap that independent operators like Polo Luxury have monetised.

Who Buys Authentic Luxury in Africa

Africa’s verified luxury consumer base is smaller than headline market figures suggest. The Henley & Partners Africa Wealth Report 2025 identifies South Africa as the continent’s leading millionaire market with 41,100 residents holding investable assets above $1 million, followed by Egypt (14,800), Morocco (7,500), Nigeria (7,200), and Kenya (6,800). These five markets represent 63% of Africa’s millionaires and account for the vast majority of authentic luxury purchasing.

Nigeria’s millionaire population has contracted by 47% over the past decade — capital flight, currency devaluation, and emigration among the professional class are the primary drivers. Yet luxury retail volumes in Lagos have not declined proportionately. The consumer pool for authentic luxury at Nigerian price points extends beyond dollar-millionaire status to oil sector executives, government contractors, diaspora returnees spending foreign-currency earnings, and tech founders whose businesses hold dollar revenues.

The strategic geography of African luxury retail reflects this: Lagos, Nairobi, Johannesburg, and Accra are the four cities that luxury conglomerates monitor for mono-brand boutique viability. Dubai’s outsized position as Africa’s luxury proxy market — where a significant share of African luxury purchase intent is actually transacted — complicates continent-specific market sizing and attribution.

African-Born Luxury: The Economics of Cultural Premium

The most structurally interesting development in Africa’s luxury economy is the emergence of African-heritage brands commanding premium pricing on international platforms. Thebe Magugu, the Johannesburg-based designer who became the first African winner of the LVMH Prize in 2019, retails women’s ready-to-wear from R6,500 to R28,000 ($350–$1,500) and is stocked at Bergdorf Goodman, Net-a-Porter, and Dover Street Market internationally. His Magugu House flagship in Johannesburg — named by Time magazine as one of the world’s best places to visit in 2024 — functions as both retail and cultural programming venue, a model that commands a brand premium beyond pure-play boutique economics.

The economics of building an African luxury house at this level require deliberate trade-offs between revenue generation and brand narrative. Magugu told Business of Fashion in 2023: “I have had to make crucial decisions that may set us back financially, but advance the goals of the brand” — characterising the tension at the heart of African luxury brand-building: international wholesale provides the revenue, but domestic presence defines the brand’s identity capital.

Nigeria’s MAXIVIVE, founded by Papa Oyeyemi, has demonstrated that African luxury can compete at international production and editorial standards: the brand debuted at Milan Fashion Week in 2021, accessing a distribution tier that previously required European heritage backing. Oyeyemi has been direct about what would transform the sector’s economics: “Let’s have the right investment in millions or even parent company formations like LVMH or KERING of the world focus on Nigeria and that sophistication would appear immediately,” he told Office Magazine. Orange Culture, also Nigerian, has maintained international stockist relationships across Europe and North America for over a decade, showing that African luxury brand longevity is achievable outside the conglomerate acquisition model.

The LVMH and Kering acquisition question — whether either group has made acquisition overtures to African design houses — is one that brand founders consistently decline to address publicly. Thebe Magugu’s LVMH Prize relationship is the closest documented connection between the European luxury establishment and an African luxury brand. The structural incentive for acquisition exists: African luxury identity provides differentiated narrative capital in a global market competing on heritage and origin story. Whether commercial due diligence supports the valuation mathematics at current African luxury brand revenue scales remains the open question.

Luxury Retail Infrastructure: The Mall Premium

Physical luxury retail in Africa concentrates in a handful of super-regional malls. Sandton City in Johannesburg is the continent’s most mature luxury retail environment: vacancy fell to 0.1% by October 2025, and luxury goods — occupying just 3.6% of the mall’s gross leasable area — now generate 19.1% of total mall turnover, up from 12.5% in 2019 (Business Day, November 2025). The Diamond Walk precinct anchors the jewellery and watch offer; new openings including Marc Jacobs and Kate Spade in 2025 point to continued brand confidence. Dimitri Kokinos, Sandton City’s General and Asset Manager, attributed the performance to deliberate curation: “We have curated a tenant mix that meets Sandton consumers’ expectations, balancing global brands, local innovation and experiences. By staying close to our tenants and maintaining operational excellence, we continue to deliver a relevant retail environment,” he told Business Day in November 2025.

Comparable infrastructure exists at The Waterfront in Cape Town, Two Rivers Mall in Nairobi, and The Palms Lagos — but at meaningfully different unit economics. Lagos luxury retail faces structural headwinds from generator fuel costs, security infrastructure spend, and foreign currency procurement complexity that inflate operating costs relative to South African or Kenyan equivalents. Multi-brand luxury retailers continue to dominate the Nigerian model because the capital requirements for a credible mono-brand boutique — brand fit-out standards, duty-free sourcing, logistics — produce economics that are marginal at current consumer volumes.

Structural Outlook

Africa’s luxury goods market is projected to grow at 4.26% CAGR through 2030 (Statista). Growth is unevenly distributed. South Africa’s trajectory is strongest on formal infrastructure grounds; Nigeria’s remains largest by consumer aspiration and informal volume. The gap between where luxury goods are officially sold and where they are actually consumed — through grey market travel purchase, parallel imports, and platform re-commerce — is widening as duty pressures increase.

The economic case for a structural shift rests on one variable: whether any of the major conglomerates concludes that the African luxury consumer base, properly addressed, justifies the duty harmonisation advocacy, retail infrastructure investment, and brand-protection spending that would be required to serve it at scale. Until that commitment arrives, the arbitrage economics of Africa’s luxury market will continue to be extracted by grey market intermediaries, counterfeit supply chains, and the handful of independent retailers sophisticated enough to navigate the duty stack profitably.

Sources: Statista, Luxury Goods — Africa Market Forecast (2025): $7.84bn market size, 4.26% CAGR projection; Henley & Partners Africa Wealth Report 2025: African millionaire population data by country; GlobeNewswire, Middle East & Africa Luxury Goods Market Analysis 2026–2031: counterfeit market characterisation; Business Day, “Sandton City hits 99.9% occupancy” (November 2025): vacancy and luxury turnover data, including quote from Dimitri Kokinos, General and Asset Manager; World Bank / Nigeria Consumer Protection Council: counterfeit goods economic loss estimates (all product categories); Nigerian Customs Service tariff schedule (US trade.gov Nigeria Import Tariffs guide): duty rate data; Thebe Magugu — Business of Fashion interview (2023): brand economics and financial trade-off quote; Papa Oyeyemi, MAXIVIVE — Office Magazine interview: quote on LVMH/Kering investment and Nigerian luxury sector; Polo Luxury official brand communications: pricing and sourcing characterisation; BETAR.africa analysis: grey market volume estimate based on duty differential and Lagos–Dubai corridor freight data.