Africa Clean Energy Finance Q1 2026: DFI Dominance, Commercial Bank Breakout, and the $8B Quarter That Rewrote the Investment Map

The first quarter of 2026 was the most active in the history of Africa’s clean energy finance market. But the volume is not the story. The story is the division of labour emerging between development finance institutions and commercial banks — a structural shift with consequences for every country on the continent that is serious about its energy transition.

On any given week in Q1 2026, a finance team somewhere in Africa was closing a clean energy deal. In South Africa, Standard Bank finalised a R6 billion solar project without any development finance institution co-lending for the first time in the country’s renewable energy programme history. In Nigeria, the World Bank unlocked its largest-ever single energy access commitment on the continent. In Namibia, the African Development Bank provided a catalytic loan designed to unlock the final investment decision on a $4.4 billion green hydrogen project. In Morocco, a Chinese battery manufacturer broke ground on what will become Africa’s first lithium-ion gigafactory.

Add the European Investment Bank’s €1 billion Mission 300 commitment, SolarAfrica’s $94 million wheeling deal in South Africa, a $52 million first close on a dedicated Africa climate venture fund, and the continuing disbursement tracking of South Africa’s $8.5 billion Just Energy Transition Partnership, and the contours of Q1 2026 become visible. By any measure — total capital committed, deal count, or geographic diversity — the quarter was the most active for Africa’s clean energy financing market on record.

The headline figure obscures the structural story. The question that matters for Africa’s energy transition is not how much capital was committed in Q1 2026, but by whom, on what terms, and in which markets. The answers reveal an emerging division of labour between development finance institutions and commercial banks that will determine how quickly Africa can scale its clean energy build-out over the rest of the decade.

The Commercial Bank Signal

The defining transaction of Q1 2026 was not the largest deal in dollar terms. It was Standard Bank’s solo debt arrangement for the 255-megawatt Lyra Energy Thakadu solar project in South Africa’s Northern Cape — approximately R6 billion in senior debt, no DFI co-lender, no bilateral guarantee, no first-loss provision from a multilateral.

This matters because it has not happened before in South Africa’s Renewable Energy Independent Power Producer Procurement Programme — a programme that has contracted more than 6,000 megawatts of private renewable energy since 2011 and attracted nearly every major DFI in the world. The standard REIPPPP financing structure involves a club of lenders in which DFIs provide concessional capital and political risk comfort that enables commercial banks to participate. Lyra Energy’s Thakadu project inverted this structure: a single commercial bank, carrying the full project on its balance sheet, with the DFIs absent.

Standard Bank’s ability to execute the deal reflects conditions that are specific to South Africa’s renewable energy market: a 20-year fixed-price power purchase agreement with sovereign-backed revenue certainty, an established developer track record, and a solar resource that has been well-characterised by nearly a decade of operational data from adjacent projects. The REIPPPP contractual framework, in effect, converts project risk into sovereign credit risk — and South Africa’s credit profile, while not investment-grade at its peak, is sufficient to support commercial project finance without DFI guarantee structures.

The limitation is explicit. Thakadu’s bankability without DFI participation is a function of South Africa’s specific conditions. It does not generalise to Nigeria’s mini-grid sector, Kenya’s geothermal development pipeline, or West Africa’s nascent solar market — contexts in which contractual frameworks, developer track records, and offtaker credit profiles require DFI participation to make projects financeable at all. But it establishes a reference point: in markets where programme credibility and contractual certainty are in place, commercial bank financing can replace DFI lending.

The DFI Pivot

If Thakadu marks the commercial bank frontier, the World Bank’s $750 million Nigeria DARES commitment marks the opposite: the continued necessity of concessional DFI capital in markets that commercial lenders will not enter.

DARES — the Nigeria Distributed Access through Renewable Energy Scale-up programme — targets 750,000 new electricity connections through solar home systems and mini-grids in 18 months. Nigeria has approximately 85 million people without electricity access, the largest deficit in the world. Its grid infrastructure prevents reliable power from reaching the majority of the population regardless of installed generation capacity. DARES is a bet that distributed solar can bypass the grid problem — but only with $750 million in International Development Association financing that prices the risk at terms no commercial lender would accept.

The Nigeria deal is not a failure of market development. It is a statement about sequencing. The DFI model — catalytic concessional capital enabling commercial capital to flow — requires a market to exist before it can be catalysed. In Nigeria’s rural electrification market, that market is still being created. DARES is creating it: establishing the operational track record, regulatory precedent, and consumer payment data that will eventually make mini-grid financing attractive to commercial capital.

The European Investment Bank’s €1 billion Mission 300 commitment, directed at Sub-Saharan Africa’s 600-million-person electricity access deficit, follows the same logic. So does the African Development Bank’s $10 million SEFA loan to unlock Hyphen Hydrogen Energy’s final investment decision on Namibia’s $4.4 billion green hydrogen project — a transaction where $10 million in concessional capital is designed to unlock 440 times its value in private and institutional financing.

The Financing Gap in Context

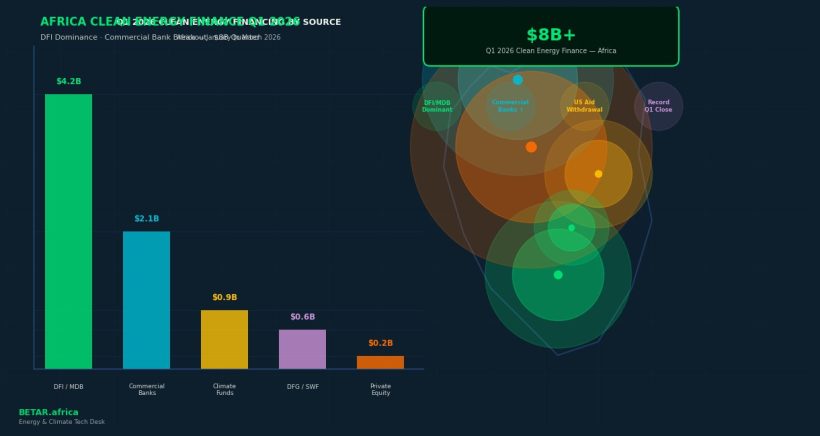

Africa requires approximately $50 billion per year in clean energy investment to stay on a trajectory consistent with the Paris Agreement. In Q1 2026, confirmed capital commitments across the continent totalled roughly $8 billion — Nigeria DARES ($750M), Lyra Energy Thakadu ($240M equivalent), SolarAfrica SunCentral 2 ($94M), EIB Mission 300 (€1B, approximately $1.1B), Persistent Africa Climate Ventures ($52M), AfDB BEEP carbon finance for clean cooking, South Africa JETP disbursements, and Morocco Gotion’s battery gigafactory groundbreaking ($5.6B in committed project investment).

At an annualised rate of roughly $32 billion, Q1 2026 represents the highest single-quarter run rate yet recorded — but still falls short of the $50 billion annual target. The gap is structural, not cyclical. It reflects the persistent concentration of bankable deals in a small number of markets — South Africa accounts for a disproportionate share of commercially-financed clean energy in Africa — and the inability of DFI capital alone to reach the 30-plus African markets that lack South Africa’s regulatory depth.

The Persistent Africa Climate Ventures first close at $52 million is a data point in a different part of the capital stack. Climate-focused venture capital is early-stage, high-risk capital that targets clean technology startups rather than infrastructure projects. Its relevance to the financing gap is indirect — better-capitalised startups produce better technology, better data, and better business models that eventually feed into bankable infrastructure. But the $52 million first close is evidence that dedicated climate VC is beginning to develop alongside project finance in Africa, addressing a gap in the capital stack that infrastructure-focused DFIs and commercial banks were never designed to fill.

Beyond Generation: Morocco’s Bet on the Value Chain

Morocco’s Gotion High-Tech gigafactory groundbreaking in Kenitra — a $5.6 billion investment in lithium-ion battery cell manufacturing — is a different kind of clean energy finance story. It is not a power generation project. It does not add a single megawatt to Africa’s grid. What it adds is the continent’s first industrial-scale battery manufacturing capacity, positioned to supply the electric vehicle and energy storage markets across North and Sub-Saharan Africa and, over time, to export to Europe.

The Gotion investment represents a structural thesis about where Africa’s clean energy role in the global economy should go: not just as a consumer of energy transition infrastructure financed by DFIs, but as a manufacturer of the components that the global transition requires. Morocco’s combination of a free trade agreement with the EU, proximity to European EV supply chains, and government incentives for industrial investment attracted the deal. Whether the model replicates elsewhere — Democratic Republic of Congo for battery minerals processing, South Africa for green hydrogen export, Kenya for geothermal technology development — is the question that will define the continent’s industrial policy agenda for the next decade.

What Q1 2026 Tells the Rest of the Year

Three things are clear from the Q1 2026 deal flow. First, the volume of clean energy capital available for Africa is growing — both DFI and commercial. Second, that capital is becoming increasingly differentiated by market maturity: commercial banks are consolidating in South Africa and, to a lesser extent, Kenya and Morocco, while DFIs are filling the vacuum in markets where commercial capital has not yet followed. Third, the continent’s clean energy story is beginning to extend beyond generation — battery manufacturing, green hydrogen, carbon markets, and climate venture capital are becoming real sectors with real capital flows, not just theoretical aspirations.

The $50 billion annual target remains out of reach. But Q1 2026 provides a clearer picture of the path: deepen the conditions that enabled Thakadu in more African markets, sustain DFI commitment in markets that cannot yet support commercial bank-only deals, and build the industrial and technology sectors that give Africa something more than consumption to offer the global energy transition.

Related BETAR.africa coverage: Nigeria DARES: The $750M World Bank Programme Targeting 750,000 Solar Connections in 18 Months (March 2026) | Lyra Energy Closes 255MW Thakadu Solar Project with Standard Bank (March 2026) | South Africa JETP: America Exited, Germany Doubled Down, and the Money Is Still Not Moving (March 2026) | Morocco Gotion: Africa’s First Battery Gigafactory Breaks Ground in Kenitra (March 2026) | Persistent Energy’s $52M Africa Climate Venture Fund First Close (March 2026)

Sources: World Bank DARES programme documents; Standard Bank / Lyra Energy financial close announcement; EIB Mission 300 press release; AfDB SEFA Hyphen Energy loan documentation; Persistent Africa Climate Ventures fund close announcement; Morocco Ministry of Industry / Gotion High-Tech groundbreaking statement; IRENA World Energy Transitions Outlook 2025; BloombergNEF Africa Energy Transition Factbook 2025; South Africa JETP Implementation Plans.

Word count: ~1,150