Tanzania’s Contactless Lead: The East Africa Payments Story BETAR Is Missing

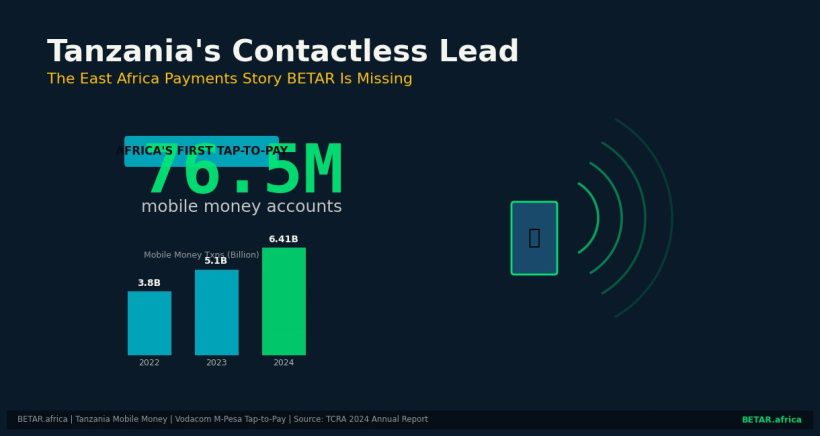

With 76.5 million mobile money accounts and Africa’s first mobile money tap-to-pay service, Tanzania is running a payments experiment that Kenya’s Safaricom monopoly cannot replicate. The continent’s coverage hasn’t noticed.

Africa’s fintech conversation has a geography problem. Nigeria and Kenya dominate the reporting. Their central banks, their unicorns, their payment rails, and their regulatory battles generate coverage in rough proportion to the lobbying power of their startup ecosystems — which is disproportionate, and the record shows it.

Tanzania, which processed 6.41 billion mobile money transactions in 2024 — a 26.7 percent increase year-on-year — is not in that conversation. Seventy-six-point-five million mobile money accounts serve a population of roughly 66 million people. Account-to-population penetration that would generate a dozen breathless analyses if it happened in Lagos or Nairobi passes without a headline.

On March 17, 2026, Tanzania quietly became the first market in Africa where a customer can tap their phone to pay via mobile money. Vodacom Tanzania, in partnership with M-Pesa Africa, payments processor Paymentology, and Visa, launched the continent’s first mobile money tap-to-pay service — embedding NFC contactless capability directly into the M-Pesa wallet. The launch received scattered regional coverage. It deserved more than that.

Why Tanzania — and Not Kenya

The tap-to-pay question is actually a competitive structure question. M-Pesa’s Tanzania launch was not accidental or a strategic afterthought. It reflects a structural reality about the two markets that is often glossed over in Kenya-first coverage: Safaricom’s dominance in Kenya, which is presented as a fintech success story, has a shadow side that constrains exactly this kind of infrastructure innovation.

In Kenya, M-Pesa holds between 94 and 96 percent of the mobile money market. That level of concentration means Safaricom has limited competitive incentive to accelerate infrastructure investments that a rival could free-ride on. Contactless NFC merchant infrastructure requires terminal rollout at scale — a capital-intensive exercise that makes more commercial sense in a multi-operator environment where the infrastructure cost is shared across the ecosystem rather than borne by a single dominant player.

Tanzania is a multi-operator market. M-Pesa (Vodacom Tanzania) competes with Airtel Money, which recorded 119.4 million transactions in Q4 2025, and Tigo Pesa. The Bank of Tanzania has positioned the country for interoperable contactless deployment since it published its contactless payment transaction circular in 2023, establishing regulatory limits and technical standards that created the enabling environment the tap-to-pay launch is now running inside.

“M-Pesa on Visa is a game-changer for Tanzania’s digital economy,” said Epimack Mbeteni, M-PESA Director at Vodacom Tanzania at the launch. “It means that any business that accepts Visa payments anywhere in the world can now also accept payments from M-Pesa customers without any additional setup.”

That last clause is the key infrastructure unlock. By routing the contactless transaction through Visa’s network rather than requiring merchant-side M-Pesa integration, the launch eliminates the merchant onboarding friction that has historically slowed mobile money adoption at the point of sale. Any business with an existing Visa-enabled POS terminal now has access to Tanzania’s 76.5 million mobile money accounts.

The Infrastructure Underneath

Tanzania’s payments infrastructure is deeper than its coverage suggests. The Bank of Tanzania’s Payment Systems Annual Report 2024 documents a market that has built its digital rails with less fanfare than Kenya but with comparable technical ambition.

TAN-QR — Tanzania’s unified merchant QR code standard — enables any mobile money wallet to pay any QR-enabled merchant without bilateral integration agreements. The standard was adopted in 2022 and has since been integrated across all major operators. It is the QR equivalent of the interoperability frameworks that Kenya’s Central Bank is still negotiating its way toward in 2026.

The banking sector’s role in contactless infrastructure is significant. CRDB Bank, with TZS 16.04 trillion in total assets, and NMB Bank, with TZS 13.39 trillion, have driven POS terminal rollout across merchant categories including supermarkets, fuel stations, and hospitality. Their infrastructure investment is the physical substrate on which the Vodacom-Visa tap-to-pay service now runs.

“What we’re seeing in Tanzania is a market that built interoperability from the infrastructure up, rather than trying to retrofit it onto an existing dominant player,” said Anna Porra, Chief Revenue Officer at Paymentology, the processing partner for the tap-to-pay launch. “That sequencing matters enormously for how contactless scales.”

Meagan Rabe, Head of Digital Partnerships at Visa Sub-Saharan Africa, placed Tanzania’s trajectory in a regional context at the launch: “84 percent of Tanzanian SMEs say digital payment tools have improved their business outcomes, according to our latest Visa Acceptance survey. The infrastructure milestone today connects those businesses to a global network they can participate in through the wallets they already use.”

Tanzania vs Kenya vs Uganda: The Regional Picture

A direct comparison clarifies what Tanzania’s contactless lead means for East Africa’s digital economy architecture.

Kenya’s mobile money market is larger in absolute transaction value — M-Pesa Kenya processes an estimated $300 billion in value annually — but its contactless capability remains limited to card-linked products served by the commercial banking system. The Safaricom-dominated structure has not produced a multi-operator contactless standard, and Kenya’s merchant POS infrastructure outside Nairobi is thin. The Ziidi Trader launch (BETA-423) shows Safaricom’s willingness to build new vertical services within M-Pesa, but horizontal infrastructure like universal tap-to-pay requires a market structure that Kenya’s concentration actively works against.

Uganda has a more competitive mobile money market — MTN Mobile Money and Airtel Uganda both operate at scale — and an active National Payment System regulator in the Bank of Uganda. Mobile money interoperability was mandated by the BOU in 2021. But Uganda has not yet produced a contactless NFC standard for mobile money, and POS terminal density outside Kampala remains significantly lower than Tanzania’s.

Tanzania’s combination of multi-operator competition, a proactive Bank of Tanzania, a unified QR standard, and substantial commercial bank POS investment has created the specific conditions for a contactless launch that its neighbours haven’t assembled.

The EAC Integration Question

Tanzania’s payments trajectory matters for East Africa’s digital economy integration ambitions — and not just as a success story. It matters structurally.

The Kenya-Rwanda PSP licence passporting MOU signed on March 11, 2026 (BETA-515) is the EAC’s most concrete step toward regional payments harmonisation. But it is a bilateral agreement between the region’s two most fintech-forward regulators. Tanzania, the region’s second-largest mobile money market, is not a signatory.

A Rwanda-Tanzania RSwitch–TIPS cross-border settlement pilot is underway, funded through the World Bank’s Eastern Africa Regional Digital Integration Project (EARDIP). If that pilot proves out in 2026, it creates a Tanzania-Rwanda corridor that runs parallel to the Kenya-Rwanda passporting framework — two pieces of a regional integration puzzle that the EAC Monetary Affairs Committee is trying to assemble into a coherent architecture.

Tanzania’s regulatory posture — the Bank of Tanzania contactless circular, TAN-QR, and now the enabling conditions for Africa’s first mobile money tap-to-pay — positions it as a market that is building the infrastructure for regional integration from the ground up. Whether the EAC can harmonise Tanzania’s payment stack with the Kenya-Rwanda bilateral framework before the region fragments into incompatible standards is one of the more consequential questions in East African digital policy.

The Hardware Ceiling

NFC contactless tap-to-pay has a hardware constraint that Tanzania’s launch does not eliminate. NFC requires a mid-to-high-tier Android device or an iPhone; it is not available on feature phones or low-cost entry-level smartphones. In Tanzania, as across most of sub-Saharan Africa, feature phones still represent a significant share of active mobile money accounts.

TAN-QR’s persistence is the pragmatic response. QR code payments work on any smartphone camera, and mobile USSD payments work on any phone. Tanzania is not going contactless-only; it is adding NFC as a payment layer for the smartphone-owning segment of its user base while maintaining USSD and QR pathways for everyone else. The Bank of Tanzania’s contactless transaction limits — established in the 2023 circular — provide the regulatory framework for managing the NFC tier without it becoming a vector for fraud at the expense of consumers on older devices.

As smartphone penetration rises — Tanzania’s smartphone adoption grew by approximately 18 percent in 2025 — the NFC layer will serve a growing share of the user base. The infrastructure investment Vodacom, CRDB, NMB, and Visa have made today is a long-duration asset.

The Coverage Problem

The underlying editorial reality here is one BETAR has an obligation to name. Tanzania’s payments story is not obscure because the market is small or the developments are minor. It is obscure because Africa’s fintech coverage industry — including this publication, until now — has defaulted to a Kenya-Nigeria axis that reflects where the VC ecosystem is concentrated rather than where the infrastructure development is happening.

76.5 million mobile money accounts. 6.41 billion transactions in 2024. Africa’s first mobile money tap-to-pay. These are not peripheral data points. They are evidence of a market that has been systematically underreported, and an East African digital economy that is not a two-country story.