Africa has a tech talent problem. Over the past decade, a cluster of private coding schools have stepped in to fix it — or at least to sell that promise. ALX Africa, Moringa School, Decagon Institute, and a growing roster of competitors collectively enrol hundreds of thousands of learners annually. Governments have pumped billions into parallel programmes. Investors have followed. The pitch is simple: train enough Africans in software engineering and the continent’s digital economy will take off.

The economics behind that pitch are more complicated.

The Market These Schools Are Competing For

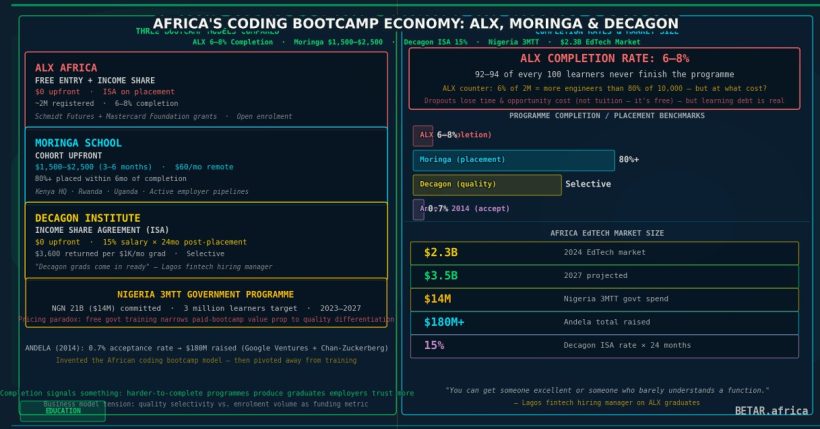

Africa’s EdTech market was valued at roughly USD 2.3 billion in 2024 and is projected to reach USD 3.5 billion by 2027, according to industry estimates. The coding bootcamp segment — focused on software development, data science, and related technical skills — represents a meaningful slice of that, driven primarily by employer demand for job-ready developers who are cheaper to train privately than to source from stretched public universities.

The competitive landscape has stratified quickly. Three models have emerged as dominant:

ALX Africa (formerly part of the Sand Technologies / Holberton School ecosystem) is the market-share leader by enrolled learners. It claims a registered user base approaching two million across its network — a number that requires immediate qualification, because “registered” in ALX’s reporting includes everyone who has started an online module, not everyone who has completed a programme. Its flagship software engineering track is tuition-free at entry, funded through a combination of foundation grants (notably from Schmidt Futures and the Mastercard Foundation), government partnerships, and, increasingly, an income-share structure where placed graduates contribute a portion of their first-year earnings back to the programme.

Moringa School, headquartered in Nairobi, runs a more traditional cohort model. Learners pay upfront — typically USD 1,500 to USD 2,500 for its software development programme, spread over three to six months, with a subscription-style remote option beginning around USD 60 per month. Moringa has expanded from Kenya into Rwanda and Uganda and has historically had a closer relationship with employer-side hiring pipelines than its free-to-enter competitors.

Decagon Institute in Nigeria has built its differentiation around the Income Share Agreement (ISA). Under Decagon’s published terms, accepted learners pay nothing upfront and instead commit to contributing 15 percent of their monthly gross salary for two years after landing a job — subject to a minimum salary threshold. At a monthly salary of USD 1,000 (roughly the NGN-equivalent mid-market rate for a junior developer in Lagos in early 2026), that works out to USD 3,600 returned to the school per successful placement, over two years. The model is explicitly bet-on-the-outcome — Decagon only earns if its graduates earn.

The Completion Rate Problem

The most widely cited figure in the African bootcamp debate is ALX’s completion rate. Investigative reports by Rest of World and TechCabal have placed the programme’s completion rate for its flagship software engineering track at between 6 and 8 percent — meaning that of every 100 learners who begin the course, somewhere between 92 and 94 never finish.

ALX has pushed back on this characterisation, arguing that its open-enrolment model deliberately accepts learners at all levels and that early attrition reflects self-selection rather than programme failure. The school also argues its absolute numbers still produce more graduates than any competing programme — that 6 percent of two million is more engineers than 80 percent of 10,000.

That arithmetic is technically correct. It does not answer the more important question: what does a 94 percent attrition rate cost the learners who drop out? For a genuinely free programme, the answer is primarily time — and opportunity cost. For programmes that charge upfront, the calculus is different. A learner who pays USD 2,000 for a Moringa cohort and drops out at month three has not merely lost time.

Moringa does not publicly report completion rates for its paid cohorts. When asked, a spokesperson pointed to a job placement figure — over 80 percent of graduates placed within six months of completion — rather than a completion-from-enrolment figure. The distinction matters enormously for any consumer making a purchasing decision.

What Employers Actually Get

The employer side of this equation is underreported. Three HR professionals at technology companies operating across Nigeria, Kenya, and South Africa — speaking on background due to ongoing hiring relationships with bootcamp programmes — offered a consistent picture: bootcamp graduates vary significantly in quality, and the variation correlates more with programme selectivity than with programme length.

“Decagon grads come in ready,” said one hiring manager at a Lagos-based fintech. “The selection process they run is tougher than most university entrance exams I’ve seen. We’ve had good outcomes.” The same manager was more cautious about ALX graduates, noting that the range of preparation was wide: “You can get someone who is genuinely excellent, or someone who barely understands what a function is.”

Moringa graduates received similar mixed notices in Nairobi, though the school’s tighter cohort structure — in-person instruction, weekly assessments, active career services — tends to produce a more consistent product than purely self-paced online programmes.

The common thread: completion signals something. Programmes that are harder to complete produce graduates employers trust more. The question is whether a school’s business model incentivises hard completion standards or easy enrolment numbers.

Government Programmes and Market Distortion

No analysis of Africa’s bootcamp economy is complete without accounting for the state.

Nigeria’s 3 Million Technical Talent (3MTT) initiative, announced in late 2023 and running through 2027, has committed NGN 21 billion — approximately USD 14 million at current exchange rates — to training three million Nigerians in digital skills including software development, data analysis, and UI/UX design. The government-funded programme partners with private training providers, including some bootcamps, to deliver curriculum at near-zero cost to learners.

The policy logic is sound: Nigeria has a structural skills deficit and private markets alone will not close it quickly enough. The execution risks are also familiar. Government-subsidised training programmes have historically struggled to maintain quality at scale, and the Nigerian technology sector has occasionally found itself flooded with “trained” graduates who lack marketable skills but do hold certificates. Whether 3MTT produces something different will depend on its quality assurance architecture, which remains opaque in public reporting.

For private bootcamps, 3MTT creates a pricing paradox. If the government offers comparable training for free, the value proposition for paid programmes narrows to quality differentiation — employer credibility, placement rates, post-graduation support. This favours premium, selective programmes like Decagon over volume-oriented free models. It may also push ALX and similar networks to compete more aggressively on graduate outcomes rather than registration counts.

The Andela Question

Any discussion of Africa’s coding bootcamp economy must reckon with Andela, the company that invented the model in 2014 and has since abandoned it.

Andela started as a highly selective bootcamp — accepting roughly 0.7 percent of applicants — that trained Nigerian, Kenyan, and Ghanaian developers and contracted them out to international technology companies. It raised over USD 180 million from investors including Google Ventures and the Chan-Zuckerberg Initiative on the premise that African software engineers were deeply undervalued.

By 2021, Andela had pivoted away from training entirely. It now operates as a pure remote-staffing marketplace — connecting pre-trained developers with global clients. The bootcamp operation became a talent pipeline for the staffing business, and eventually the staffing business was valuable enough on its own that the pipeline was cut.

The Andela arc tells an uncomfortable story about where the money actually is in the African EdTech bootcamp chain. Training is a thin-margin, difficult-to-scale operation. Placement and staffing — taking a commission on the salary of a developer you connected to a company — is a recurring, compounding revenue stream. The school is not where you make money. The recruiter is.

Several newer entrants appear to have absorbed this lesson. Zone, the UK-based programme that has expanded into Nigeria, is structured less as a school and more as a developer community with an integrated hiring engine. Decagon’s ISA model is, in economic terms, a 24-month recruiting commission dressed as tuition. The line between bootcamp and staffing agency has blurred in ways that are rarely made explicit to learners.

What Learners Should Know

For the hundreds of thousands of Africans who will encounter a coding bootcamp marketing message this year, a few questions are worth asking before signing up, paying, or committing an income share.

What is the completion rate, from enrolment to graduation certificate? Not the placement rate of graduates — the completion rate of all who started. Any school that cannot answer this question clearly is selling enrolment, not education.

What is the six-month and twelve-month employment rate, and what counts as employed? A support agent role at a call centre is technically “employed in tech.” A junior software engineering role is not the same thing.

For ISA programmes: what is the cap? Most responsible ISA structures include a total payment cap — typically 1.5x to 2x the cost of tuition. Programmes without a cap expose learners to open-ended financial liability.

Africa’s tech talent gap is real. The bootcamp industry that has grown up to address it contains genuinely excellent programmes, extractive ones, and many that fall between those poles. The continent will produce its next generation of developers. The question is which programmes will get credit, and at what cost.

BETAR.africa reached out to ALX Africa, Moringa School, and Decagon Institute for comment on completion rates, pricing structures, and graduate outcomes. ALX Africa and Moringa School did not respond by deadline. Decagon Institute confirmed its ISA terms but declined to provide aggregate placement data.