Two Telecoms, One Continent: What Airtel Africa and MTN’s FY2025 Results Reveal About Africa’s Biggest Strategic Bet

By Business Reporter, BETAR.africa | 22 March 2026

Africa’s two dominant pan-continental telecoms operators have now both reported their results for the year ended March 2025, and the numbers tell a surprisingly similar story: both recovered sharply from currency-driven losses, both posted strong constant-currency revenue growth, and both are betting that mobile money will define their next decade.

But the strategies for getting there could not be more different — and the FY2025 data is beginning to reveal which approach is working.

The Headline Numbers

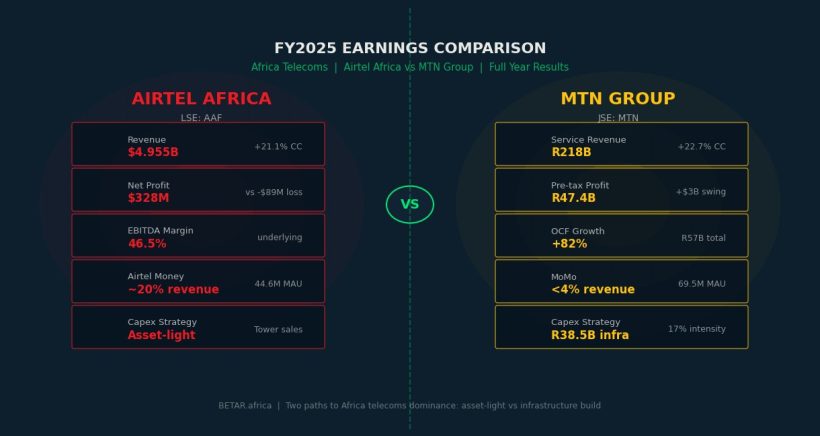

Airtel Africa reported revenue of $4.955 billion for its fiscal year ended 31 March 2025, representing a 21.1 percent increase in constant currency terms despite a marginal 0.5 percent decline in reported dollars — a result of the same naira and Malawian kwacha devaluation headwinds that hammered the entire sector. Net profit rebounded to $328 million from a loss of $89 million the previous year. Underlying EBITDA reached $2.304 billion, with margins of 46.5 percent.

MTN Group posted service revenue of R218 billion for the calendar year 2025, up 22.7 percent in constant currency, with pre-tax profit swinging to R47.4 billion ($2.81 billion) from a pre-tax loss of R4.1 billion in 2024. MTN’s customer base crossed 307 million against Airtel Africa’s 166.1 million — a gap that reflects MTN’s presence in West Africa markets that Airtel does not serve.

Both companies outran the macro environment. Both are generating meaningful cash. Both experienced roughly similar constant-currency revenue growth. And yet, from that shared starting point, the two operators are making almost exactly opposite capital allocation decisions.

The Fintech Gap — and Who Is Closing It

The most important strategic question in African telecoms right now is not voice or data. It is mobile money: which operator will convert a massive user base into a genuine financial services business?

Here, the FY2025 numbers expose a striking divergence.

Airtel Money — Airtel Africa’s mobile financial services arm — contributed approximately 20 percent of group revenues for the full year. Mobile money subscriber counts reached 44.6 million, growing 17.3 percent year-on-year, with mobile money revenue up 29.9 percent in constant currency. Airtel is on the verge of a structural milestone: in its most advanced markets, Airtel Money is no longer a feature of the telecom business. It is a standalone financial services business that happens to ride the telecom rails.

The evidence for this is the Airtel Money IPO trajectory. As of March 2026, Airtel Africa CEO Sunil Taldar confirmed the company is “very close to finalising the preferred listing venue,” with London and the UAE both under active consideration. An IPO of Airtel Money would make it the continent’s most significant fintech listing since Flutterwave shelved its own plans — and would force the market to value it separately from the voice and data business, almost certainly revealing a premium.

MTN MoMo presents a very different picture. MoMo reached 69.5 million monthly active users across 16 markets — significantly larger than Airtel Money’s user base. Yet MoMo fintech revenue represented less than 4 percent of MTN Nigeria’s total service revenue of ₦5.20 trillion, and the group-level contribution remains similarly modest. The distribution is enormous. The monetisation is not.

This gap — 69.5 million MoMo users generating less than 4 percent of revenue, against 44.6 million Airtel Money users generating roughly 20 percent — is the central challenge of MTN’s $2 billion M&A strategy. MTN has more users and less revenue per user. The acquisition thesis is that product depth (lending, savings, insurance) will close this gap. The FY2025 results suggest it has not closed yet.

Two Infrastructure Strategies, Two Capital Theories

The second major divergence is infrastructure.

Airtel Africa has been aggressively selling passive infrastructure — towers — for most of the past four years. The rationale was debt reduction and capital efficiency. By offloading towers to Helios Towers and others across Tanzania, Madagascar, and several Francophone markets, Airtel converted fixed assets into cash, reduced its debt burden, and committed to a sale-and-leaseback model that keeps operating costs variable. The result is an asset-light balance sheet that prioritises cash returns to shareholders: the board declared a full-year dividend of 6.5 cents per share, up 9.2 percent year-on-year.

MTN has moved in the opposite direction. The company is building FibreX — its fixed-line broadband push targeting 8 million connected homes in Nigeria as the first phase of a broader 30 million homes Africa group target — while maintaining FY2025 actual capex of R38.5 billion at 17% of service revenue, within MTN’s own 15–18% target range. The FibreX build is a long-duration infrastructure bet that will not generate meaningful revenue for several years. MTN’s $2 billion M&A war chest adds another layer of capital commitment, this time on the inorganic side.

The implicit investor proposition each company is making is therefore quite different. Airtel Africa is saying: the infrastructure stage is over, cash is being returned, and Airtel Money is the growth engine that will be unlocked at IPO. MTN is saying: the infrastructure stage is not over, there is more to build, and the returns will be larger when the platform is complete — but they will take longer.

Nigeria: Shared Pain, Different Scale

Nigeria is the market where both operators’ strategies face their hardest test. The naira devaluation of 2023–2024 compressed dollar-denominated earnings sharply for both, forcing them to negotiate tariff increases with the Nigerian Communications Commission.

MTN Nigeria’s FY2025 numbers, filed separately on the Nigerian Exchange, showed service revenue of ₦5.20 trillion ($3.37 billion at prevailing rates), up 55 percent year-on-year in naira terms. Nigeria became MTN’s single largest EBITDA contributor — overtaking South Africa for the first time in the group’s history, with EBITDA of $1.926 billion against South Africa’s $1.048 billion.

Airtel Nigeria delivered H1 2025 revenue of $699 million, up 46.5 percent. Nigeria’s EBITDA margin reached 56 percent — among the highest of any market in the Airtel group.

Both operators are growing fast in Nigeria. The difference is that MTN’s Nigeria business is more than twice the size of Airtel’s, and MTN’s FibreX investment in Nigeria is a direct attempt to open a fixed broadband market that Airtel is not pursuing at scale.

The Investor Question

For investors comparing the two stocks — MTN Group trades on the Johannesburg Stock Exchange, Airtel Africa on the London Stock Exchange — FY2025 presents a genuine trade-off.

Airtel Africa offers a cleaner earnings story: strong constant-currency growth, rebounding net profit, progressive dividends, and an Airtel Money IPO that could crystallise hidden value. The risk is execution: the tower sale-and-leaseback model locks in future lease costs, and the IPO timeline is market-dependent.

MTN offers scale and optionality: the largest mobile money user base in Africa, a growing fixed broadband position, and the M&A firepower to move into product verticals. The risk is timing: until MoMo converts its 69.5 million users into a material revenue contributor, the fintech thesis remains a promise rather than a data point.

FY2025 did not resolve the contest. But it sharpened the question. Both companies survived the devaluation cycle. Both emerged profitable. The next phase — fintech monetisation, infrastructure returns, and M&A execution — will determine which bet was right.

BETAR coverage: BETA-945 — MTN Group FY2025: Nigeria Overtakes South Africa | BETA-366 — MTN $2B Acquisition War Chest | BETA-965 — MTN FY2025 War Chest Strategy Validation

Sources: Airtel Africa plc FY2025 Annual Results (8 May 2025, NGX Group filing); Airtel Africa Annual Report 2025; MTN Group FY2025 Investor Relations; NGX Group official filings; Finance in Africa; Nairametrics; DirectorsTalk Interviews