The Private School Bargain: Africa’s Low-Cost Private Schooling Market After Bridge International

Bridge International Academies built the largest case for and against low-cost private schooling in Africa simultaneously. Its collapse left a $14.5 billion sector in need of a new model — and regulators with harder questions than the ones Bridge was willing to answer.

March 2026

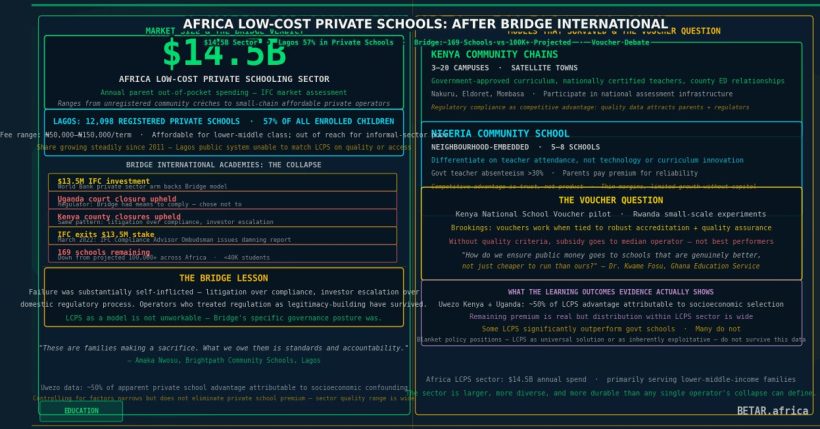

When the Kampala High Court upheld the Ugandan government’s closure of Bridge International Academies’ schools in 2018, the judgment was precise about why: Bridge had the means to comply with national educational standards, had been given multiple opportunities to do so, and had chosen not to. The same pattern played out in Kenya, where courts upheld county-level closures for failure to meet regulatory requirements. By the time IFC, the World Bank’s private sector arm, exited its $13.5 million investment in Bridge in March 2022, the company had contracted from a projected network of tens of thousands of schools across Africa to 169 facilities serving fewer than 40,000 students. The implosion was the continent’s most closely watched experiment in scaled, technology-driven low-cost private schooling — and it produced a verdict that the sector has spent the years since trying to interpret correctly.

The tempting reading is that Bridge’s failure exposed the low-cost private school model as fundamentally unworkable: extractive, standardisation-obsessed, hostile to teacher professionalism, and willing to put commercial expansion ahead of regulatory compliance and child safety. The harder and more useful reading is that Bridge’s failure was substantially self-inflicted — a product of a specific governance posture and investment thesis — and that the sector it attempted to dominate is larger, more diverse, and more durable than any single operator’s collapse can define.

The Size of the Market Bridge Tried to Capture

Sub-Saharan Africa’s low-cost private school sector is estimated at approximately $14.5 billion annually in parent out-of-pocket spending, based on IFC market assessments — making it one of the largest untapped education markets on the continent. The sector encompasses a range of providers: registered private schools serving lower-middle-income families in peri-urban areas; unregistered community schools operating with basic infrastructure in informal settlements; church and faith-based networks offering subsidised fees; and, increasingly, small-chain affordable private school operators attempting to build replicable models from a base of 5 to 20 schools.

Lagos is the most instructive case study in sheer scale. The state is home to approximately 12,098 registered private schools, which account for 57 per cent of all enrolled children — a figure that has grown steadily since 2011 and reflects a structural demand that the Lagos State public system has not been able to match for quality or, in peri-urban areas, for access. Most of those schools are not chains. They are owner-operated, community-embedded, and operating at fee points between ₦50,000 and ₦150,000 per term — affordable by the standards of the city’s lower-middle class, still out of reach for the informal-sector poor.

“We serve 1,400 children across four campuses in Surulere and Ajegunle,” said Amaka Nwosu, founder of Brightpath Community Schools, a Lagos-based affordable private operator. “These are families who have decided that the public school system is not working for their children and are paying what they can to give them something better. They are not wealthy families — they are families making a sacrifice. What we owe them is standards and accountability, not a script read off a tablet.”

What Bridge Got Wrong About Accountability

Bridge’s model was built around a thesis that teacher discretion was the primary variable in school quality and that standardisation — scripted lessons delivered via tablet, centrally monitored attendance, algorithmically tracked learning progression — could substitute for professional teacher development at lower cost. The thesis was not entirely wrong. There is evidence that structured pedagogical frameworks improve learning consistency in low-resource environments, and Bridge’s early-stage outcome claims were not fabricated. What the model could not survive was the accountability question.

Government regulators in both Uganda and Kenya identified specific non-compliances: teacher qualifications below national standards, facilities that failed minimum physical requirements, curriculum materials not approved by national boards. Bridge’s response — litigation rather than compliance, investor escalation rather than engagement, appeals to international arbitration rather than domestic regulatory process — confirmed the worst fears of governments that had been sceptical of private equity-backed education operators from the outset. The regulatory battles accelerated the closures rather than reversing them, and the IFC’s own Compliance Advisor Ombudsman produced a damning assessment of how the institution managed conflicts between its investment in Bridge and its development mandate.

The lesson is not that regulation kills LCPS — it is that LCPS operators who treat regulation as an obstacle to scale rather than a legitimacy-building process eventually lose the political licence to operate. The operators who have survived and grown in the same markets where Bridge collapsed have done so by meeting, and in some cases exceeding, government standards rather than contesting them.

Two Models That Are Scaling

Kenya’s affordable private school sector has evolved along lines that are instructive for the wider continent. Following Bridge’s contraction, a cohort of smaller, founder-led chains — operating between 3 and 20 campuses, typically in Nairobi’s satellite towns and secondary cities including Nakuru, Eldoret, and Mombasa — have grown by building relationships with county education offices rather than around them. These operators use government-approved curriculum, hire nationally certified teachers, and in several cases participate in Kenya’s national assessment infrastructure, giving them learning outcome data that strengthens their position with parents and regulators simultaneously.

Nigeria’s community school model takes a different form. The most durable operators in Lagos and Ogun State are embedded in specific neighbourhoods, draw their boards from the local community, and differentiate themselves from government schools on teacher attendance and accountability rather than technology or curriculum innovation. Their competitive advantage is not a product — it is trust. Parents in communities where teacher absenteeism in government schools runs above 30 per cent pay a premium for a school where the teacher shows up. The commercial model is modest, margins are thin, and growth beyond 5 to 8 schools is difficult without external capital. But these schools persist because they are solving a specific, real, local problem.

What the Learning Outcomes Evidence Actually Shows

The learning outcomes debate in the LCPS sector has been significantly distorted by motivated reasoning on both sides — pro-private advocates citing raw performance data, critics citing selection effects, and neither group fully engaging with what the ASER and Uwezo assessment data actually shows. The most credible synthesis, drawn from within-household comparison studies using Uwezo Kenya and Uwezo Uganda data, finds that approximately half of the apparent private school advantage is attributable to socioeconomic confounding — children in LCPS come from households with higher parental education, more books at home, and more nutritional stability. Controlling for these factors narrows but does not eliminate the private school premium.

What the Uwezo data does show clearly is that the distribution of performance within the LCPS sector is wide. Some low-cost private schools significantly outperform government schools on foundational literacy and numeracy at comparable income levels. Many do not. The sector average masks a quality range that runs from genuinely effective community schools to operators whose primary advantage over government provision is that the building has a roof and the teacher shows up. Blanket policy positions — LCPS as a universal solution, or LCPS as inherently exploitative — do not survive contact with that distribution.

The Voucher Question

The persistent policy proposal for the sector — government vouchers redeemable at accredited private schools — has accumulated more evidence in the years since Bridge than it had before. The Kenya National School Voucher pilot, the evidence from Rwanda’s small-scale voucher experiments, and the Brookings Institution’s comparative analysis of voucher programmes in developing countries collectively support a conditional conclusion: vouchers work when they are attached to a robust accreditation and quality assurance system, and they fail or become regressive when they are not. Handing government money to a sector with as wide a quality distribution as Africa’s LCPS market, without differentiated quality criteria, directs subsidy to the median operator rather than to the best ones.

“The voucher conversation always stalls at the same point,” said Dr. Kwame Fosu, Director of Private Education Policy at the Ghana Education Service. “Government officials want to know: how do we ensure public money goes to schools that are genuinely better, and not just to schools that are cheaper to run than ours? That is not an unreasonable question. It is the question that any serious voucher design has to answer first, not last.”

The Post-Bridge Market Map

The low-cost private school sector in Africa is not in retreat. It is restructuring. The investor-backed chain model that Bridge represented has not found a credible successor at comparable scale. The $14.5 billion market that IFC identified has not been consolidated — and may not be consolidatable in the way venture-style education investors imagined, given the local trust dynamics and regulatory complexity that govern school-by-school quality. What has grown are the models that Bridge could not replicate: founder-led, community-embedded, regulation-compliant, and modest in their ambitions for geographic expansion.

The sector’s policy challenge now is not whether to accommodate LCPS — governments across the continent have effectively accepted that the public system cannot serve all enrolled children without private sector participation. The challenge is to build the regulatory frameworks that distinguish effective operators from ineffective ones, so that public voucher money and international development capital flows toward schools that demonstrably improve learning outcomes rather than those that simply fill a gap in access that the state has failed to close.