MTN Spent Its War Chest on Towers. Now What?

By Business Reporter, BETAR.africa | 27 March 2026

When MTN Group CEO Ralph Mupita unveiled a $2 billion acquisition war chest in February 2026, the stated ambition was unambiguous: buy product depth for MoMo, close the East Africa gap, and transform Africa’s largest telecoms operator into the continent’s most powerful financial services platform. The $2 billion was earmarked for fintech acquisitions — lending, savings, insurance — not infrastructure.

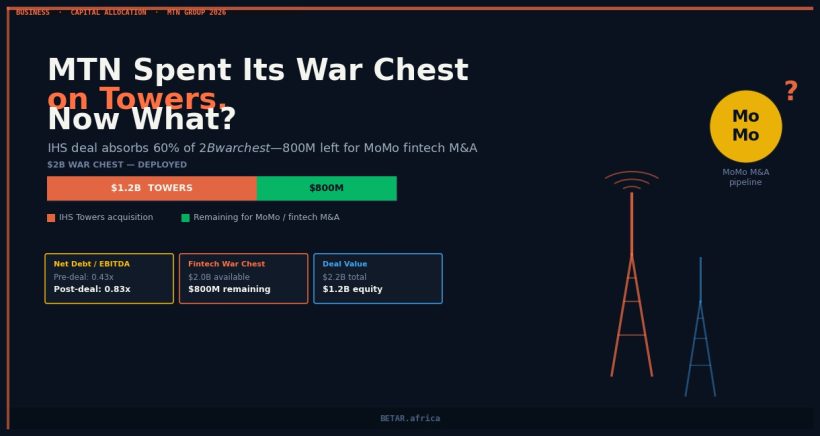

Six weeks later, MTN announced it is deploying a substantial portion of that capital to acquire the remaining equity in IHS Towers at a deal valuation of $2.2 billion, comprising $1.2 billion in equity and approximately $1 billion in assumed debt obligations. The deal changes the calculus on every forward-looking assumption MTN had telegraphed.

This is not a pivot from the platform thesis. But it is a compression of the runway to execute it.

The Balance Sheet Before and After

MTN Group closed FY2025 with net debt of ZAR 42 billion against group EBITDA of ZAR 98.5 billion — a net debt/EBITDA ratio of approximately 0.43x. At the current USD/ZAR rate of approximately 18.2, that net debt position equates to roughly $2.3 billion. Group EBITDA of $5.4 billion gives a comfortable leverage position at well below 1x.

The IHS deal restructures that materially.

The equity component of $1.2 billion (~ZAR 21.8 billion) will be funded from cash on the balance sheet — the war chest. Adding the $1 billion debt assumption (~ZAR 18.2 billion), the total deal commitment of $2.2 billion represents ZAR 40 billion absorbed into the MTN consolidated balance sheet. Post-close, net debt rises to approximately ZAR 82 billion, pushing net debt/EBITDA from 0.43x to approximately 0.83x.

That remains within conventional investment-grade telecoms leverage range — Vodacom operates at roughly 0.9x, Safaricom has periodically exceeded 1x without rating concern. MTN has not broken the bank. What it has done is deploy the majority of the discretionary acquisition capital that was previously available for fintech M&A.

The equity portion of the IHS deal ($1.2 billion) consumes 60 percent of the $2 billion war chest. The remaining ~$800 million is the liquid M&A firepower MTN carries into the next 18 months for the fintech acquisitions Mupita has been publicly signalling. That is not an insignificant sum — it is acquisition-scale for a mid-sized African fintech — but it is not the transformational capital deployment that MoMo’s product gap requires.

Why Towers?

The strategic logic of the IHS acquisition requires engagement on its own terms before judging the capital trade-off.

IHS Towers is MTN’s most important infrastructure relationship. MTN is IHS’s largest customer, accounting for more than 30 percent of IHS revenues across its African tower portfolio. That customer-supplier dynamic has always carried strategic risk: MTN’s network expansion depends on tower availability and lease economics that IHS sets. As IHS navigated its own debt restructuring and management turbulence through 2024 and 2025, MTN faced the prospect of having its infrastructure dependency governed by a financially distressed counterparty.

Full ownership resolves that dependency. MTN internalises the tower economics — lease costs that currently run at market rates become internal transfers, with the difference accruing to the consolidated P&L. The infrastructure moat argument is also credible: as MTN expands its fixed wireless access (FWA) strategy targeting 30 million connected homes, owning the tower infrastructure rather than leasing it gives the company direct control over the capital investment decisions that determine FWA coverage quality.

The internal EBITDA accretion from tower ownership is real. Analyst estimates suggest MTN could capture between ZAR 3 billion and ZAR 5 billion in annual lease savings and income from third-party tower tenancies. At current EBITDA multiples, that accretion justifies a significant portion of the deal premium. The deal is not irrational — it is just competing with a different set of priorities that Mupita himself established.

Dividend Sustainability: The Naira Problem Remains

MTN declared a dividend of ZAR 5.00 per share following FY2025 — a 45 percent increase from ZAR 3.45 the prior year and a signal that management believes the earnings recovery is durable. IHS acquisition debt slightly complicates that signal.

The increase in net debt/EBITDA from 0.43x to approximately 0.83x is not severe enough to trigger dividend policy recalibration under MTN’s stated distribution framework, which targets a payout ratio of 45 percent to 75 percent of headline earnings. The IHS deal, on its own, does not threaten the dividend.

The naira does.

Nigeria generated EBITDA of $1.926 billion in FY2025 — more than South Africa ($1.048 billion) and Ghana ($1.276 billion) combined. Nigeria’s contribution was elevated by a naira FX tailwind of ₦90.27 billion that reversed the catastrophic ₦925.36 billion loss of FY2024. That reversal is not guaranteed to hold. If the naira weakens materially in 2026 — and Nigeria’s macro conditions give no structural guarantee of stability — MTN’s consolidated EBITDA could decline by $600 million to $900 million in a downside FX scenario. In that environment, maintaining ZAR 5.00 per share while servicing increased IHS acquisition debt would require accessing the remaining war chest for working capital support rather than growth deployment.

Dividend sustainability at current levels assumes naira stability. The IHS deal narrows the buffer.

MoMo’s Compressed Runway

The fintech acquisition thesis has not changed. MoMo’s gap — 67 million active users generating less than 4 percent of service revenue, against M-Pesa at 40 percent and Airtel Money at 25 percent — remains the clearest value creation opportunity on MTN’s agenda.

But with $1.2 billion of the war chest committed to IHS equity, the capital available for fintech acquisitions is constrained to approximately $800 million — enough for one meaningful deal, not a portfolio of them.

Mupita’s stated target categories — Kenya-licensed lending, cross-border remittance infrastructure, digital insurance underwriting — require different acquisitions with different price points. A Kenya-licensed fintech with meaningful GMV might trade at $200 million to $400 million on current valuations. That is achievable with the remaining capital. A lending platform with pan-African reach, the transformational acquisition that would reset MoMo’s product benchmark, likely requires $600 million to $900 million. That was possible with the pre-IHS war chest; it is marginal post-IHS.

MTN will also generate additional free cash flow in 2026 and 2027 as capex intensity moderates from the FY2025 level of 17 percent of service revenue. Analysts at Nedbank CIB project that MTN’s operating free cash flow could reach ZAR 65 billion by FY2026, providing approximately $500 million in incremental acquisition capacity annually. The war chest is not permanently depleted — it is time-shifted. Fintech acquisitions Mupita might have executed in 2026 may now happen in 2027.

Whether the fintech window remains open on the same terms is less certain.

BETAR Assessment: The Right Deal at the Wrong Moment

The IHS Towers acquisition is strategically defensible. Tower ownership consolidates infrastructure control, eliminates lease risk, and will generate EBITDA accretion that justifies the capital deployment over a five- to seven-year horizon. If this were 2024 — before MTN had publicly committed to a fintech-first acquisition strategy — the market would interpret it as disciplined infrastructure consolidation.

The timing creates the problem. MTN has spent the first quarter of 2026 signalling to analysts, investors, and fintech founders that its war chest exists for platform acquisitions. The IHS deal absorbs the majority of that capital for infrastructure — necessary infrastructure, but infrastructure that most analysts would not have ranked above MoMo product depth as a strategic priority.

The market will need to be re-educated on the capital allocation sequence: IHS first, because the opportunity arose and the strategic rationale held; fintech through free cash flow accretion, starting in late 2026 or 2027. That is a coherent story. It is also a different story than the one told in February.

For MTN to close the MoMo monetisation gap that constitutes its most important medium-term value creation lever, execution on at least one significant fintech acquisition needs to happen before the year is out. The capital, while compressed, is present. The question is whether the deal pipeline — particularly in Kenya — is ready to meet it.

The war chest was spent on towers. The next chapter depends on whether the cash flow that replaces it arrives in time to matter.

Related BETAR coverage: MTN FY2025 Results: Nigeria Is Now the Engine | MTN FY2025 War Chest Strategy Validation | MTN’s $2B Acquisition War Chest | MTN 30M Connected Homes FWA Push

— Business Reporter, BETAR.africa