Kenya Sets Africa’s Highest Stablecoin Bar — and 50 Crypto Firms Still Want In

Draft VASP regulations propose a KES 500 million capital requirement for stablecoin issuers. The Kenya Virtual Assets and Artificial Intelligence Association calls it a domestic kill shot. The Nairobi NIFC crypto hub is the other half of the same strategy.

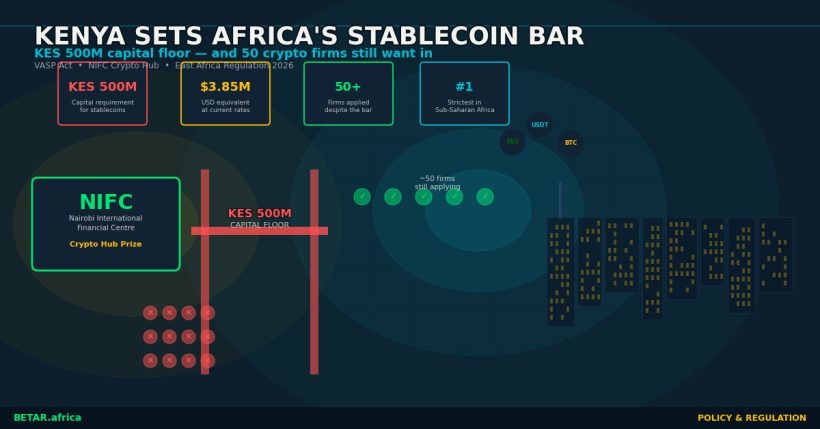

Kenya’s National Treasury has proposed the strictest stablecoin capital requirement in Sub-Saharan Africa. Under draft regulations circulated for public comment, stablecoin issuers seeking a licence under the country’s Virtual Asset Service Providers Act would need to hold a minimum of KES 500 million — approximately $3.85 million at current exchange rates — in qualifying capital before they can legally operate.

The number lands hard. Nigeria’s Virtual Assets Regulation, finalised in early 2026, sets capital floors for crypto exchanges and custodians but contains no comparable threshold for stablecoin issuers specifically. South Africa’s Financial Sector Conduct Authority, which brought crypto service providers into its regulatory perimeter in 2023, operates on a risk-based capital adequacy model rather than a fixed floor. Ghana’s VASP Act sandbox, now running with eleven admitted firms, has not disclosed stablecoin-specific capital thresholds.

Kenya’s figure is a deliberate design choice — and the industry knows it.

What the Rules Say

The draft regulations, released for stakeholder comment in late March 2026, set out capital requirements for each category of licensed virtual asset service provider. For stablecoin issuers — defined as entities that issue tokenised instruments pegged to fiat currency, commodities, or baskets of assets — the proposed floor is KES 500 million (~$3.85M).

The requirements extend beyond the capital floor. Stablecoin issuers would be required to hold full-reserve backing for all issued tokens — 100% liquid assets matching the outstanding supply — and to publish audited reserve attestations quarterly. Interest or yield cannot be paid on stablecoin balances held by retail customers, a provision designed to prevent stablecoin issuers from operating as shadow deposit-takers outside CBK oversight.

Custody rules require that reserve assets be held in segregated accounts at CBK-licensed institutions, with no commingling with proprietary or operational funds. A licensed stablecoin issuer must obtain advance CBK approval before any material change to its reserve composition, pricing mechanism, or smart contract architecture.

For exchange and brokerage operations — the second regulated category — the capital floor is set at KES 50 million (~$385,000). Custody-only providers face a KES 20 million (~$154,000) threshold. Stablecoin issuance is priced an order of magnitude higher than anything else on the table.

The Industry Pushback

The Kenya Virtual Assets and Artificial Intelligence Association — VAAK — filed formal objections within days of the draft’s circulation. The association represents a coalition of domestic operators across the VASP stack: exchanges, custodians, payment gateways, and digital asset infrastructure providers.

VAAK’s core argument: the KES 500 million floor effectively eliminates domestic stablecoin issuance as a business category. At current capitalisation levels, the association estimates that more than 90% of Kenya-domiciled crypto firms cannot meet the threshold. Only well-capitalised foreign entrants — and a small number of established local fintechs already operating at scale — would qualify.

The association has proposed three alternatives to Treasury. The first is a tiered capital structure: a KES 50 million entry threshold with a 24-month regulatory runway to scale to KES 200 million for firms that demonstrate reserves compliance and operational stability. The second is a reserve-ratio model, where capital adequacy is calculated as a percentage of outstanding stablecoin supply rather than an absolute floor — allowing early-stage issuers to grow their capital base in proportion to their market. The third is a regulatory sandbox carve-out: an admission pathway for domestic stablecoin issuers to operate at reduced capital levels under direct CBK supervision for an initial 18-month period, with full licensing available upon successful completion.

None of VAAK’s proposals have yet been accepted. The consultation window closes in April 2026.

Why Kenya Set the Bar This High

The KES 500 million figure is not an accident. Treasury officials, in briefings to the financial services industry, have framed it explicitly as a systemic risk management instrument — a mechanism to ensure that any entity issuing a currency-equivalent instrument in Kenya’s financial system holds sufficient capital to withstand a run scenario without requiring a CBK intervention or consumer protection backstop.

The regulatory logic tracks the global conversation. The collapse of TerraUSD in 2022, which wiped roughly $40 billion in market value over three days, produced regulatory aftershocks that are still reverberating through emerging market crypto frameworks. Kenya’s draft rules are explicit about the risks that motivated the threshold: stablecoin de-peg events, insufficient reserve management, and the potential for retail financial harm at scale.

The high bar is also, frankly, a filter. Kenya does not want dozens of thinly capitalised stablecoin issuers competing in a market that is still building investor confidence and regulatory credibility. It wants a small number of well-capitalised, auditable institutions — and it is willing to price out the local market to get there.

VAAK’s objection is that this approach sacrifices domestic ownership of the stablecoin infrastructure to the benefit of foreign entrants with deep pockets. If Kenya’s stablecoin issuance layer is captured entirely by international players — Circle, Tether, or regional fintech conglomerates — the domestic innovation and employment benefits of building a live crypto economy accrue elsewhere.

The Other Half of the Strategy: Nairobi as Africa’s Crypto Hub

The capital rules are only half of Kenya’s crypto regulatory architecture. The other half is playing out at the Nairobi International Financial Centre, where approximately 50 global crypto firms are in active discussions about establishing regional headquarters under NIFC’s preferential framework.

The NIFC offers incorporated entities a suite of incentives: a reduced 15% corporate tax rate on qualifying income (against Kenya’s standard 30%), VAT relief on certain financial services transactions, streamlined work permit processing for international staff, and access to double taxation agreements. For crypto firms looking to anchor their African operations in a well-regulated, well-connected jurisdiction, the package is competitive.

Among the firms in discussions, Binance has been most prominently reported. The exchange, which withdrew from Nigeria in early 2024 after a regulatory confrontation with the CBK’s peer institution and paid a substantial fine to the Nigerian financial crimes authority, has since been publicly rebuilding its Africa-focused regulatory posture. Nairobi — with its VASP Act, NIFC framework, and a government that is actively marketing itself as Africa’s financial services capital — is a logical landing point.

The NIFC track and the capital threshold track tell a coherent story when read together. Kenya is pricing out domestic micro-operators while rolling out a hospitality framework for institutional entrants. The domestic market gets a rigorous, internationally credible regulatory architecture. Global players get a stable, incentivised operating base in East Africa’s largest economy. The question VAAK is asking is whether domestic entrepreneurs get anything at all.

Where This Leaves Kenya’s Regulatory Race

Kenya’s VASP Act came into force in November 2025, giving the country East Africa’s most comprehensive crypto statute. But as BETAR reported in March 2026, implementing regulations — the rules that actually define licensing conditions — remained unpublished for the first four months of the Act’s operation. The draft stablecoin capital rules represent the first concrete implementation signal from Treasury since the Act commenced.

They land in a continent that is building its crypto regulatory architecture at speed. Nigeria’s VARA framework is operational. Ghana’s VASP sandbox is running. South Africa’s CASP licensing regime has been processing applications since late 2023. Rwanda is simultaneously building out virtual asset rules alongside its retail CBDC pilot.

Kenya has the most sophisticated statutory foundation on the continent. Its implementing regulations will determine whether that foundation produces a domestic crypto industry or primarily serves as a landing pad for international capital. The KES 500 million stablecoin floor is the clearest signal yet of which outcome Kenya’s Treasury has decided to optimise for — and the consultation window is the last formal opportunity for industry to argue otherwise.

BETAR.africa covers African technology, business, and innovation. Follow our Policy & Regulation and Crypto beats for ongoing coverage of Kenya’s VASP implementation.