Francophone Africa’s EdTech Gap: Why 26 Countries Are Being Left Behind

As investors declare Francophone Africa the continent’s next tech frontier, education technology remains the sector most conspicuously absent from the region’s investment map.

May 2026

When TechCabal opened its 2026 with a cover story declaring Francophone Africa “the smart money’s next frontier,” the piece catalogued the usual suspects: fintech interoperability, climate adaptation, logistics networks, and venture studios from Dakar to Abidjan. Education technology did not feature. That absence was not an editorial oversight. It was an accurate reflection of where the capital is — and where it is not.

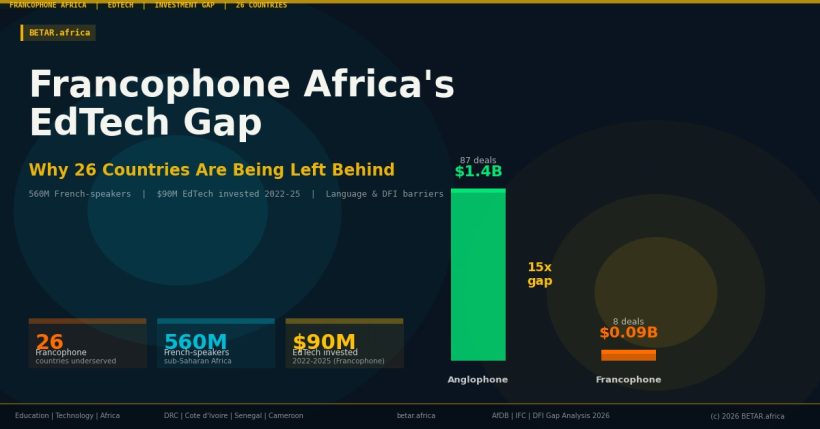

Francophone Sub-Saharan Africa comprises 26 countries with a combined population of more than 500 million people. French is the primary official language of instruction from Senegal to the Democratic Republic of Congo, from Cameroon to Madagascar. The region produces millions of secondary school graduates annually and faces the same structural skills gaps — in technology, healthcare, and technical vocations — that the rest of the continent confronts. What it does not have is a functioning EdTech investment market.

The Numbers

African startups collectively raised more than $3.4 billion in 2025. Francophone African startups — primarily in North and West Africa — raised approximately $450 million of that total, a growing share driven by Senegal, Côte d’Ivoire, and Morocco. The deals were concentrated in fintech, mobility, and climate-linked services.

EdTech does not appear in the Francophone Africa deal tables. The most significant education investment originating in the Francophone region in recent years is Enko Education — a Cameroon-founded, pan-African International Baccalaureate school network that raised $24 million in January 2025 from Africa Capitalworks and Adiwale Fund, and subsequently closed a $46 million total financing round in February 2026. The deal brought Enko’s school footprint to 16 institutions across 10 countries with 7,500 students, targeting 20,000 by 2029.

Enko is a brick-and-mortar private school operator with IB accreditation, targeting the continent’s top 5 percent of secondary school families by income. As its co-founder and CEO Eric Pignot has explained, the company’s strategy is to “consolidate Africa’s fragmented K-12 market” — finding schools with strong foundations to elevate into “African international schools of choice.” It is not, in any meaningful sense, a digital education platform for the mass market. It is also the most-funded Francophone EdTech company in Africa’s recent history — which illustrates the depth of the problem.

The broader EdTech sector, as tracked by BETAR in our Q1 2026 funding review, recorded zero major EdTech equity rounds on the continent this quarter. Within that already-thin market, Francophone Africa is the most consistently absent geography.

Why the Capital Doesn’t Flow

The structural barriers are known, documented, and persistent. They are also underappreciated in their compound effect.

Language. Most of Africa’s active EdTech investors — Partech Africa, Novastar Ventures, Founders Factory Africa, Owl Ventures — conduct their diligence in English. Most African EdTech pitch decks are written in English. Most EdTech founders networking at AfricArena, at Techpoint Inspired, at Lagos Angel Network events are communicating in English. The Francophone founder operating out of Abidjan or Yaoundé faces not just the standard startup fundraising challenge, but an additional translation layer — cultural as much as linguistic — that most English-speaking investors are not equipped to cross.

The gap is visible even to builders operating across both sides of the language divide. Cedric Mangaud, co-founder and CEO of Mstudio — the Ivorian venture studio explicitly designed to close the Francophone-Anglophone innovation gap — is direct about it: “We [francophone countries] are way behind the likes of Nigeria, Kenya and South Africa and we need to collectively build sustainable ventures that can reduce the gap and eventually close it.” That assessment applies to tech broadly. In EdTech, where deep market understanding depends on local knowledge of school systems, curricula, and household behaviour, the barrier is compounded further.

Content. Building an EdTech platform for Nigerian primary school students is expensive. Building one for Ivorian primary school students — producing content in French, aligned to the BEPC curriculum, appropriate for the infrastructure conditions of schools in Bouaké or Korhogo — costs a comparable amount of capital but produces a much smaller addressable market from any single country. The pan-Francophone pitch, spanning 26 countries with 10+ distinct national curricula, is intellectually attractive but operationally extremely complex. Most EdTech founders — including those from Francophone backgrounds — take the path of least resistance toward English-medium, larger-TAM Anglophone markets.

DFI configuration. Development finance institutions, which as BETAR reported are now the primary capital vehicle for African EdTech in the DFI-dominant 2026 environment, are also predominantly Anglophone in their programme architecture. The Mastercard Foundation’s EdTech Fellowship operates through CcHUB in Lagos and MEST Africa in Accra — both Anglophone. IFC’s education sector portfolio in Sub-Saharan Africa skews toward Nigeria, Kenya, and South Africa. The Agence Française de Développement (AFD) is the natural French-language DFI counterpart, but its education investment mandate has historically prioritised French bilateral academic partnerships and curriculum support over EdTech startup equity.

Where the Exceptions Are

Three companies are doing meaningful work at the intersection of digital education and Francophone markets, though none has achieved the scale of Anglophone Africa’s leading platforms.

Prepavenir, operating from Côte d’Ivoire, provides digital exam preparation for BEPC and BAC examinations and has built a subscriber base across West Africa’s Francophone corridor. It has not attracted significant external investment but demonstrates sustainable unit economics on a subscription model.

ARED (African Renewable Energy Distributor), originally focused on energy access, has pivoted to deliver offline digital learning content via solar-powered devices in low-connectivity Francophone communities across West Africa — a hardware-software hybrid approach that sidesteps the infrastructure problem rather than solving it.

UNESCO and the KIX Africa 21 Hub launched a joint initiative in 2025 to develop AI competency frameworks and translate digital learning resources into local African languages across Francophone markets — acknowledging that the language and content gap cannot wait for the private sector to fill it.

None of these represents a venture-scale EdTech business. They represent the floor of what exists.

The 2026 Opportunity Window

Jean-Marc Savi de Tové, Managing Partner at Adiwale Partners — which backed Enko Education’s January 2025 fundraise — frames the scale of the underlying demand: “The continent is experiencing rapid population growth, with 750 million young Africans expected to be of school age by 2030.” That capital is backing physical IB schools at premium price points, serving thousands of students. The digital, French-medium, mobile-first platform to serve the rest of the population remains unfunded.

There are signals that the Francophone Africa investment environment is shifting in ways that could eventually reach EdTech. Ventures Platform and Launch Africa have opened offices in Abidjan. Enza Capital is deploying into Francophone North Africa. Multiple local angel networks are deepening in Senegal and Côte d’Ivoire following improvements in the regulatory and startup law environment.

The educational infrastructure to support an EdTech market is also growing. Francophone African secondary enrolment rates have risen consistently since 2015. Mobile penetration in Côte d’Ivoire, Senegal, and Cameroon now exceeds 80 percent. Smartphone affordability, which GSMA’s 2026 pilot programme is targeting directly, will materially expand the addressable market for mobile EdTech in the region within the next three years.

What Francophone Africa’s EdTech market needs — and does not yet have — is a founder with the linguistic reach, curriculum knowledge, and investor access to build a cross-border platform at the scale that Anglophone Africa’s leading companies have achieved. That founder may already exist, building quietly in Abidjan or Dakar on a fraction of the capital their Anglophone peers attracted.

If so, they are raising in a market that is not yet watching.