After seven years and a peak of 35 million monthly active users — a figure widely cited in reporting on Ayoba’s 2022 growth milestone — MTN has shut down Ayoba. The app was removed from major app stores on March 20, 2026. Existing users in Nigeria, Ghana, and South Africa have 30 days before the service goes dark. The post-mortem is short: African telcos cannot build messaging apps. The interesting question is what they can build instead.

Ayoba launched in 2019 with a playbook borrowed from Asia. MTN, Africa’s largest telco by subscribers at roughly 280 million, watched WeChat transform China Mobile from a connectivity pipe into a daily commerce and payments platform. The pitch was plausible: MTN had distribution across 19 markets, a billing relationship with hundreds of millions of subscribers, and the ability to offer zero-rated data on its own network. If any telco in Africa could pull off a super app, it was MTN.

It could not.

What killed Ayoba

The autopsy points to a single structural flaw: Ayoba was built on an incentive that was not a product. Zero-rated data attracted users to a platform they would not have chosen on merits. When those data incentives were scaled back — as they had to be for MTN to maintain margins on a service it was effectively subsidising — users left. The platform had failed to generate the behavioural stickiness that makes a super app defensible: daily utility, financial integration, network effects among contacts.

The 35 million monthly active user figure, cited at peak around 2022, masked this. Monthly active users on a zero-rated messaging platform measures incentive uptake, not product-market fit. WhatsApp was already used by most of Ayoba’s target audience for messaging. TikTok owned short-form content. Both had global network effects no single-market or regional telco app could replicate without a decade of investment and a fundamentally different product.

MTN’s own financials delivered the verdict before the shutdown announcement. Its digital services segment grew 15% in 2025 — respectable by most metrics but trailing the fintech business’s 24.9% growth and $500 billion in transaction value processed. When a company’s capital allocation decisions need to be made, those numbers tell the story.

The unified platform pivot

MTN’s official framing is that Ayoba is not a failure — it is a consolidation. MTN said in an official statement that it is “building a unified digital platform designed to bring connectivity, content, services, and everyday digital experiences together in one place,” reducing fragmentation across its digital product portfolio.

What that means in practice is less clear, but the direction is. MTN’s Ambition 2030 strategy has crystallised around three core platforms: connectivity (broadband, FWA, and mobile data), fintech (MoMo), and digital infrastructure (data centres, the AI compute play via Genova). Consumer entertainment and messaging are conspicuously absent from that taxonomy. The unified digital platform, to the extent it exists, looks more like a services layer on top of MoMo than a replacement for Ayoba.

The connectivity ambition is real and large: MTN is targeting 20 to 30 million homes connected via fixed wireless access and fibre-to-the-home across its markets. That is an infrastructure bet, not a content play. It builds from MTN’s structural advantage — network ownership — rather than trying to out-product companies whose entire business is software.

The playbook that works: payments first, services second

The contrast with how MTN’s peers have approached the super app question is instructive. Safaricom did not attempt to compete with WhatsApp. It built M-PESA into Africa’s most successful financial super app by starting with a utility — mobile money — that 35 million Kenyans now depend on for wages, rent, and school fees. Additional services (Ziidi Trader for stock investments, AI fraud detection, merchant tools) were added to a platform users already could not leave, not to a platform users were being paid to join.

The outcome is striking. M-PESA holds 89.7% of Kenya’s mobile money market. Safaricom processes up to 12,000 transactions per second. The AI and investment features being rolled out in 2026 land on a platform with genuine network lock-in.

Airtel Money is following a version of the same logic — operating as a licensed independent Payment Service Provider in Kenya since 2022, targeting an IPO in 2026, and building financial services on payment rails rather than trying to be an entertainment platform. Orange Money has leaned into cross-border remittances, where telco distribution genuinely creates value that pure-play fintechs struggle to match.

The pattern across Africa’s successful telco-digital plays is consistent: payments, lending, insurance — financial products with daily utility and a structural moat in regulatory relationships and distribution. Not messaging. Not content. Not gaming.

The lesson for Africa’s telco-to-tech story

MTN spent seven years and considerable engineering and marketing resources building a product it ultimately could not monetise at the scale its network warranted. The capital and management attention consumed by Ayoba is an opportunity cost against the MoMo and FWA buildout that is now MTN’s primary growth story.

The lesson is not that African telcos cannot build digital businesses — MoMo’s $500 billion in annual transaction volume is one of the most significant digital financial infrastructure achievements on the continent. The lesson is that the things telcos are uniquely positioned to build are fundamentally different from the things consumer internet companies build.

Telcos own spectrum, towers, and billing relationships. Those assets create moats in connectivity, payments, and increasingly in enterprise digital infrastructure. They do not create moats in messaging or short-form video, where global incumbents have network effects that no regional player can overcome by offering free data.

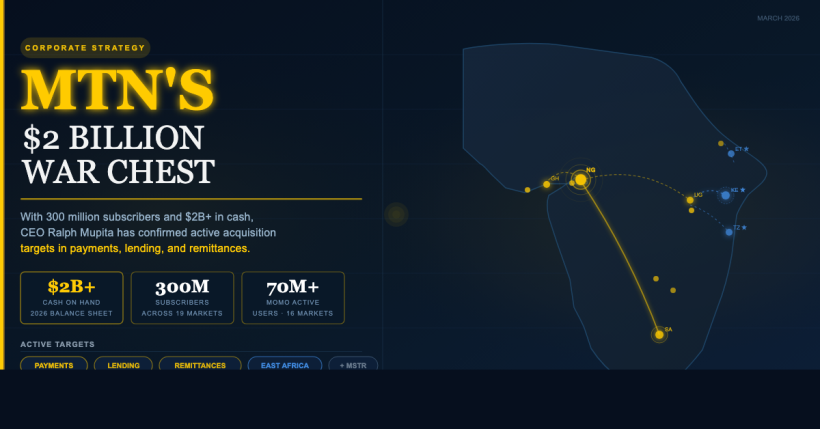

MTN’s $2 billion-plus acquisition war chest — confirmed at its FY2025 results — is now being watched for signals about where the company thinks the next moat is. The Ayoba shutdown is a data point in that investment thesis. The app graveyard has one more occupant. The question is what gets built with the capital that was subsidising it.