Africa LNG Expansion vs. Energy Transition: $50B in Gas Infrastructure and a Continent Caught Between NDCs and Commercial Reality

In February 2025, the first cargo of liquefied natural gas loaded at Sangomar, off the coast of Senegal, and sailed for Europe. It was a moment of genuine national celebration — Senegal, a country that had never produced oil or gas at scale, had made it into the global LNG export league. Three weeks later, President Bassirou Diomaye Faye stood at the African Union summit and reaffirmed Senegal’s nationally determined contribution under the Paris Agreement: a renewable-led energy future.

Both things are true simultaneously, and that is exactly Africa’s problem.

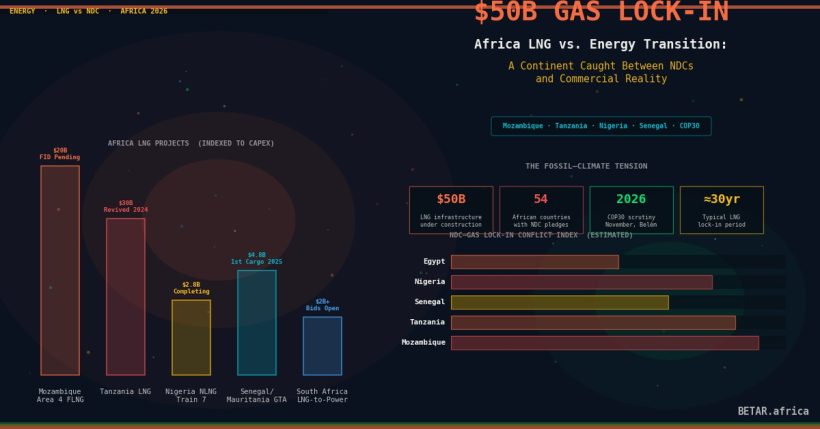

Across the continent, approximately $50 billion in LNG and gas infrastructure is either producing, under construction, or approaching a final investment decision. From Mozambique’s Coral FLNG platform — which has been exporting since 2022 — to Tanzania’s long-stalled $30 billion LNG project, revived in 2024 with ExxonMobil and Shell back at the table, to Nigeria’s NLNG Train 7 completing its $2.8 billion expansion, gas is having a moment in Africa. The Powering Africa Summit in Washington in March 2026 made the geopolitical logic explicit: US Energy Secretary Chris Wright pitched gas as a “transition fuel” for Africa, with the Export-Import Bank positioned to finance American LNG service exports.

The problem is that African governments are simultaneously committed — legally, diplomatically, and increasingly financially — to something different. All 54 AU member states have submitted NDCs to the UNFCCC. Most of those NDCs describe a renewable-dominated energy future. At COP30 in Belém in November 2026, those commitments will face their most rigorous scrutiny yet. And the gap between what African governments are building and what they have pledged is growing wider by the quarter.

The Gas Map

The $50 billion figure is not a projection — it is infrastructure that exists, is under construction, or has secured commercial financing. The breakdown matters.

Mozambique is the continent’s largest gas play. Coral FLNG (ENI, Eni’s 35.7% stake; co-investors include ExxonMobil, CNPC, and Galp) is producing and exporting. Mozambique LNG Area 4, TotalEnergies’ $20 billion project, was suspended after jihadist insurgency forced an emergency in 2021, but TotalEnergies has signalled conditional resumption pending security guarantees. Rovuma Area 1, the ExxonMobil/ENI joint venture, is separately in development planning. Together, Mozambique’s potential LNG capacity could reach 50 million tonnes per annum — larger than the current total output of the United States.

Tanzania LNG’s revival is the story of 2024–25. The project — involving ExxonMobil, Shell, Equinor, and Pavilion Energy — was effectively suspended for a decade over fiscal terms disputes. New host government agreements signed in 2024 have reopened the path to FID, though $30 billion in financing at a moment of rising capital costs remains a formidable hurdle.

Senegal and Mauritania’s GTA LNG (BP, Kosmos Energy, Petrosen, SMHPM) hit its first cargo in February 2025, delivering on a project that has been central to both countries’ development planning for a decade. Nigeria’s NLNG Train 7, a $2.8 billion Shell-led expansion of the existing Bonny Island facility, is completing construction and is expected to add 8 million tonnes per annum to Nigeria’s already substantial export capacity.

Egypt — via Eni and BP’s Mediterranean gas fields — is expanding both domestic supply and re-export capacity through its LNG terminals at Damietta and Idku.

The NDC Arithmetic

Every country on this list has submitted an NDC describing an energy transition. The question is not whether they have climate pledges — they do. The question is whether those pledges are consistent with the infrastructure they are committing to finance.

The International Energy Agency’s Africa Energy Outlook 2024 is unambiguous on this point. To keep African energy development aligned with the 1.5°C pathway, the continent needs to triple its renewable energy investment — from approximately $25 billion annually to $75 billion — while limiting new fossil fuel development to assets serving domestic energy access needs. LNG export infrastructure, by definition, is not domestic energy access. It is export revenue — which matters for fiscal stability, but which does not reduce energy poverty and does not advance the renewable transition.

The NDC contradiction is sharpest in Mozambique and Tanzania, where the scale of gas infrastructure dwarfs any plausible domestic energy consumption scenario. Mozambique’s entire electricity grid serves roughly 5 million connections. The Coral FLNG platform alone, when at full capacity, produces enough gas to power the country many times over — and exports all of it to Europe and Asia. This is not energy access. It is resource extraction on a large scale, which is a legitimate development strategy but is not the same as the renewable transition that Mozambique’s NDC describes.

Carbon Tracker and IEEFA have both modelled the stranded asset exposure. Their analysis suggests that African LNG projects premised on long-term export demand to Europe and Asia carry significant commercial risk: the EU’s carbon border adjustment mechanism, accelerating coal-to-renewables transitions in East Asia, and falling renewable costs all point toward lower long-run LNG demand than the project economics assume. The fiscal risk falls asymmetrically on African states — because international oil companies structure their LNG contracts with exit provisions that state-owned enterprises and host governments typically cannot match.

The Bridge Argument — and Its Limits

Proponents of African gas expansion — including, prominently, the African Union, the African Development Bank until recently, and the US government — make a “bridge fuel” argument. The logic is that gas can provide dispatchable, reliable baseload power while Africa builds out renewable capacity; that gas for electricity generation is preferable to coal; and that gas revenues provide the fiscal space for governments to invest in the renewable transition over time.

There is something to this argument in specific contexts. Gas-to-power projects aimed at domestic electricity generation — replacing diesel generators or preventing load-shedding — have a different climate calculus than LNG export terminals designed to serve European markets. South Africa’s LNG-to-power bids, which are seeking to replace coal with gas as an interim measure while the country scales renewables, are a more defensible case than a deepwater FLNG platform whose entire output is sold under long-term export contracts to European utilities.

The US government’s conflation of LPG for clean cooking with LNG export infrastructure is, however, a category error that has consequences. At the Powering Africa Summit, Secretary Wright used clean cooking access — which is a genuine humanitarian priority; 900 million Africans still cook on biomass, causing 600,000 deaths annually — to justify a broader gas-friendly posture that includes large-scale LNG export infrastructure. LPG for clean cooking uses small cylinders distributed through retail networks. LNG export infrastructure uses deepwater floating facilities and multi-decade export contracts. They are not the same thing, and treating them as interchangeable obscures the actual tradeoffs.

DFI Pressure: Who Is Financing What

The development finance landscape has shifted materially since COP29 in Baku. The African Development Bank, under its revised energy strategy, has committed to halt new financing for unabated fossil fuel projects. The European Investment Bank made the same commitment earlier. The World Bank’s energy lending has shifted sharply toward renewables.

This leaves African LNG projects increasingly dependent on bilateral DFI support — primarily US EXIM Bank, Japanese JBIC, and Chinese policy banks — plus commercial bank financing from institutions with weaker climate commitments. The result is a bifurcated DFI landscape: multilateral institutions aligning with COP30, bilateral lenders and commercial banks filling the gap for gas.

IM Bank Kenya’s $30 million green finance facility with SIDA, closed in March 2026, represents the multilateral direction of travel. The facility is structured to provide risk-sharing for renewable energy SME lending — the kind of instrument that actually moves money to energy access without the stranded asset risk of a deepwater LNG terminal. It is, in funding quantum, tiny compared to the LNG projects. But it points to where development finance is heading.

The COP30 Reckoning

The Belém COP will be different from previous climate negotiations in one important respect: the Global Stocktake, which assessed collective progress against NDCs in 2023, found a 20–23 gigaton gap between stated commitments and 1.5°C-consistent pathways. African NDCs, taken together, are some of the most ambitious per-capita commitments in the world — but only if the gas infrastructure currently being built does not lock in decades of fossil-fuel dependence.

The honest reckoning for African governments is that gas infrastructure and NDC commitments are only simultaneously viable if two conditions hold: gas genuinely displaces coal rather than adding to the energy mix; and revenues from gas exports are invested in the renewable transition rather than absorbed into general fiscal expenditure. Neither condition is guaranteed, and for export-oriented LNG infrastructure, neither condition is even the primary design intent.

Africa’s gas moment is real, commercially significant, and — for the producing countries — a legitimate response to decades of external pressure to leave fossil resources undeveloped while industrialised economies burned their own. That grievance is politically and historically valid. But the $50 billion being committed to LNG infrastructure will outlast any transition timeline that is consistent with limiting warming to 1.5°C. That is the contradiction that COP30 will not be able to paper over.

— Energy & Climate Tech Reporter, BETAR.africa

Related coverage: America’s Africa Energy Pivot: Clean Cooking and Critical Minerals Instead of Climate Finance | Africa Clean Energy Finance Q1 2026 | Africa Green Hydrogen 2026